“Damn, there is so much great knowledge out there. Did you know that “BOOKS” are full of smart?? No, I mean like life changing, I-wish-I-knew-that-years-ago type stuff.

I know that I was waaaayyy late to the game figuring it out. And I know that a lot of you are too busy to read as much as you ‘should’. And that is why you need me.

I still remember how it started for me. It started in June of 2008. After 11 years …..Click to continue

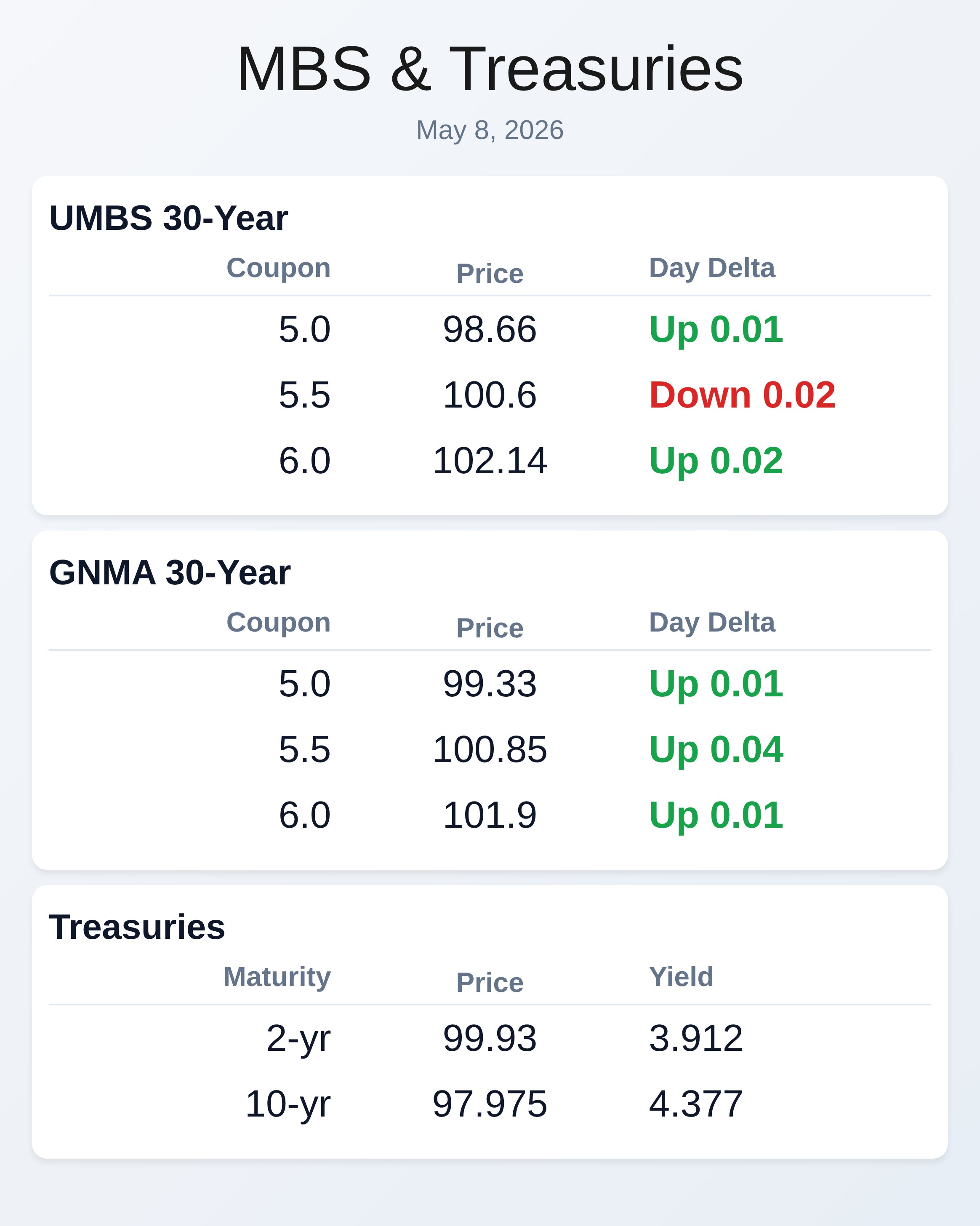

May 8, 2026

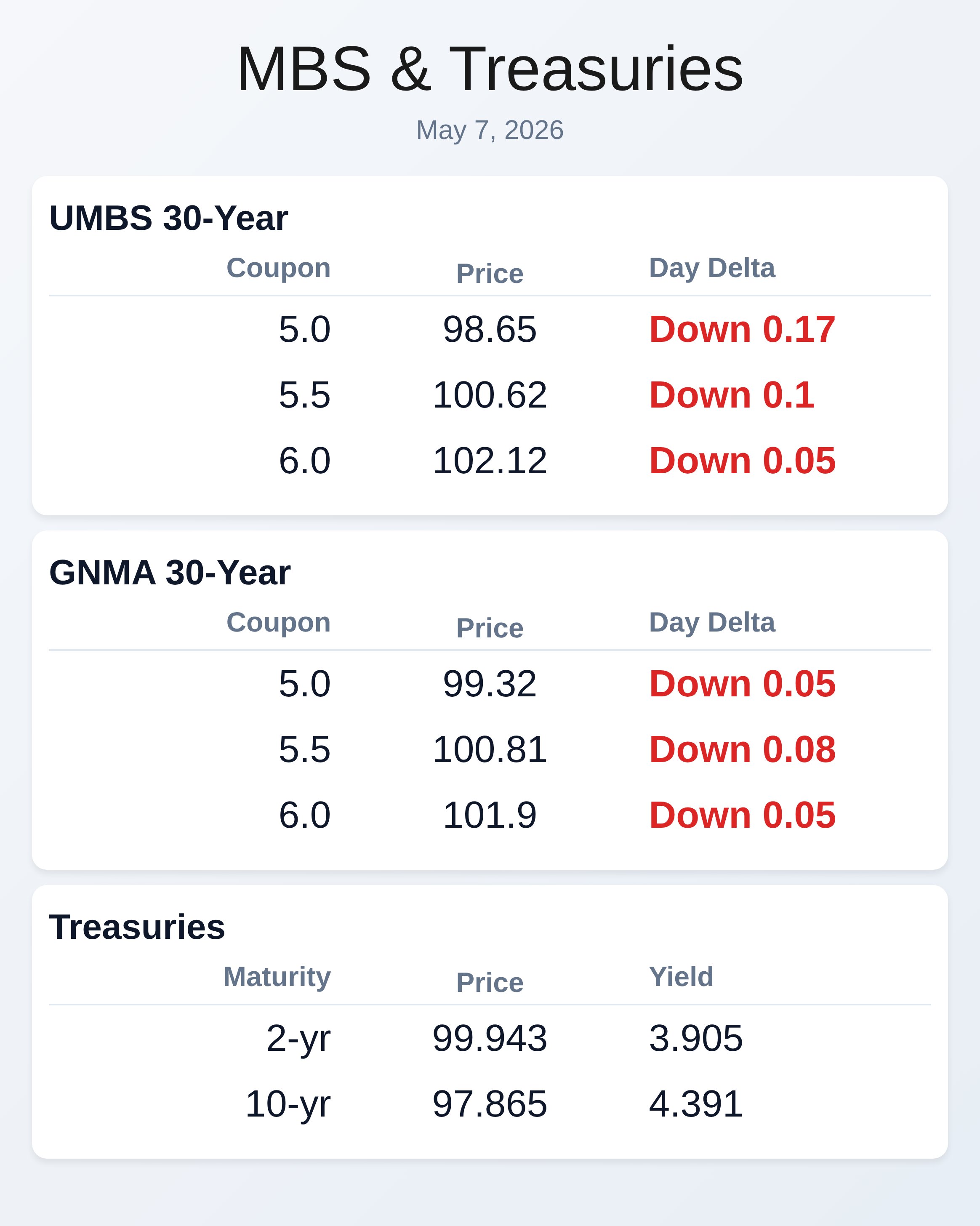

May 7, 2026

May 7, 2026

RECENT ARTICLES

What’s up in Mortgage Today (PM) – 10/16/2025

WTMS Blog Today = What's up in Mortgage Today (PM) - 10/16/2025 Block trading activity dominated the morning, sending UMBS prices lower despite a relatively light economic calendar. The 30-year UMBS 5.0 coupon dropped to [...]

What’s up in Mortgage Today (PM) – 10/15/2025

WTMS Blog Today = What's up in Mortgage Today (PM) - 10/15/2025 Bond markets are rallying this morning as earnings reports soothe trade war fears that dominated headlines last week. The UMBS 5.0 coupon gained [...]

What’s up in Mortgage Today (AM) – 10/15/2025

WTMS Blog Today = What's up in Mortgage Today (AM) - 10/15/2025 Markets are winning across the board today as positive earnings reports soothe lingering trade war fears. The UMBS 5.0 coupon sits at 99.75, [...]

Article Archive

Mortgage Today 12/21: Modest Gains Amid Economic Data and Fed’s Rate Outlook

In today's mortgage market update, we observed modest gains as MBS (Mortgage-Backed Securities) displayed some positive movements, with the 6.0 coupon rising by 8 basis points and the 5.5 coupon by 2 basis [...]

Part 2: The Reciprocity Rule.

Reading Notes For: Part 2: The Reciprocity Rule. This is a summary of my reading notes from Influence by Robert Cialdini. "Influence: The Psychology of Persuasion" by Robert Cialdini is [...]

Yeah But……. Volume 2= The Mortgage World DOESN’T Suck Right Now

Yeah But........... Volume #2

Mortgage Today 12/19: Stable Market, Housing Growth, and Student Loan Concerns – What to Expect

UMBS 6.0 was flat. The 5.5 coupon was up 6 bps in the first hour of trading. Bond pricing is slightly improved this morning as treasury yields continue to inch lower. The U.S. [...]

What is Influence? – How does it work? – Why is it important?

Reading Notes For: Part 1: The Introduction This is a summary of my reading notes from Influence by Robert Cialdini. "Influence: The Psychology of Persuasion" by Robert Cialdini is a [...]

Mortgage Today 12/18: Understanding the Impact of Fed Speak and Market Resilience

UMBS were down 11 bps on the morning. Bonds were almost perfectly flat overnight with 10s trading in a narrow range between 3.89 and 3.93. The first discernible move of the day arrived [...]

We need to stop taking ourselves personally

Today's lesson is from "The Fear Book" by Cheri Huber Some things we may not think of as fear - anger, sadness, irritation, urgency, depression, control issues - are pointing to an underlying fear. [...]