**WTMS Blog Today = What’s up in Mortgage Today (AM) – 05/22/2026**

Peace deal rumors triggered a mid-day market reversal that sent mortgage-backed securities and treasuries higher by late morning. The 10-year Treasury yield fell 0.022% intraday to 4.547%, while UMBS 30-year coupons posted gains across the board. Geopolitical headlines continue to dominate price action, making today’s direction unpredictable until we see if broader geopolitical developments settle before the long weekend.

Intraday volatility remains the default mode, meaning MBS pricing and 10-year yield movements are your primary risk management tools right now. Originators should stay alert to headline-driven swings and be ready to capitalize if rates improve further on Friday. Economic data came in mixed, with building permits and housing starts exceeding expectations while jobless claims held steady.

The Philly Fed Business Index fell sharply to -0.4 from 26.7 previously, signaling a significant pullback in regional manufacturing sentiment. Continued claims stayed flat at 1.782K, suggesting labor market resilience despite the manufacturing slowdown. These crosscurrents leave the Fed narrative unclear and keep yields range-bound.

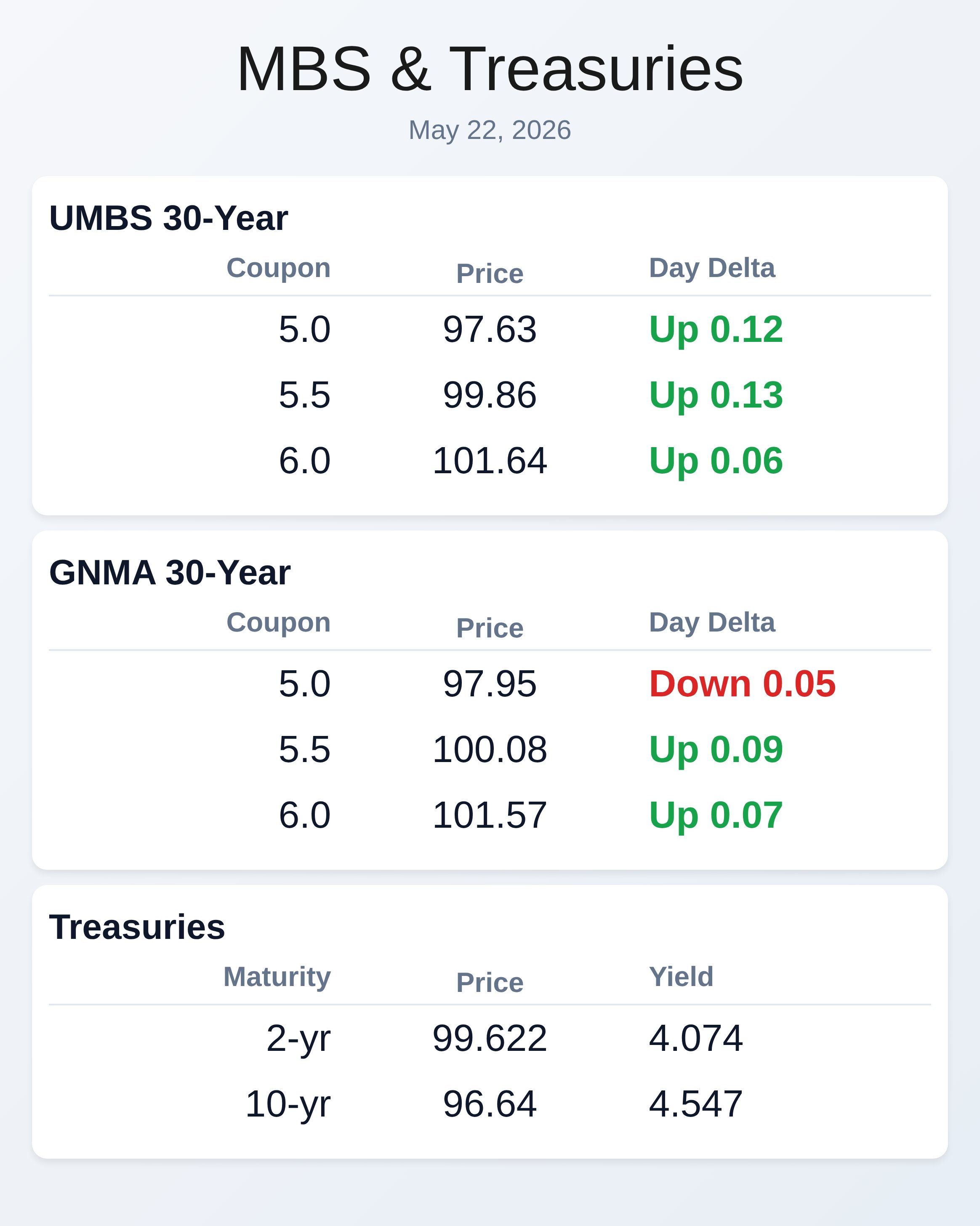

Mortgage sellers should monitor whether Friday’s data or weekend headlines push markets decisively in either direction. UMBS 30-year coupons rallied on intraday relief, with 5.0% coupons up 0.12 points to 97.63 and 5.5% coupons up 0.13 points to 99.86. GNMA 30-year securities showed more modest moves, with 5.5% and 6.0% coupons posting gains while 5.0% coupons retreated slightly.

The compression between UMBS and GNMA pricing reflects normal sector positioning ahead of a three-day weekend. Treasury prices extended gains across the curve, with 2-year yields dropping 0.008% and 10-year yields falling 0.022% intraday. These moves suggest risk-off sentiment is supporting the longer end despite mixed housing data.

**Locking vs Floating**

Building permits came in hotter than forecast, but the Philly Fed manufacturing index collapsed, creating conflicting signals about near-term economic momentum. War headlines are driving the dominant narrative, so headline-driven volatility is the dynamic to expect through Friday. Originators face uncertainty about whether geopolitical forces will push for a market move before the three-day weekend or pull back until Tuesday.

Lock your pipelines if you see another rate improvement on Friday—it may not last through the long weekend. Float aggressively only if you believe geopolitical tensions will sustain headline-driven weakness beyond the weekend break.

**Today’s Events**

Building Permits (Apr): 1.442M vs 1.39M forecast, 1.363M previous

Continued Claims (May/09): 1,782K vs 1,790K forecast, 1,782K previous

Housing Starts (Apr): 1.465M vs 1.41M forecast, 1.502M previous

Jobless Claims (May/16): 209K vs 210K forecast, 211K previous

Philly Fed Business Index (May): -0.4 vs 18 forecast, 26.7 previous

Philly Fed Prices Paid (May): 47.90 vs forecast unavailable, 59.30 previous

**Bond Pricing**

**UMBS 30 yr**

| Coupon | Price | Intra-Day Change |

| 5.0 | 97.63 | 0.12 |

| 5.5 | 99.86 | 0.13 |

| 6.0 | 101.64 | 0.06 |

**GNMA 30 yr**

| Coupon | Price | Intra-Day Change |

| 5.0 | 97.95 | -0.05 |

| 5.5 | 100.08 | 0.09 |

| 6.0 | 101.57 | 0.07 |

**Treasuries**

| Term | Yield | Price | Intra-Day Yield Change |

| 2 yr | 4.074 | 99.622 | -0.008 |

| 3 yr | 4.127 | 98.247 | -0.013 |

| 5 yr | 4.224 | 98.442 | -0.019 |

| 7 yr | 4.382 | 99.213 | -0.022 |

| 10 yr | 4.547 | 96.64 | -0.022 |

| 30 yr | 5.076 | 95.007 | -0.015 |