**WTMS Blog Today = What’s up in Mortgage Today (PM) – 05/21/2026**

Geopolitical headlines dominated mortgage markets today as peace deal rumors triggered a dramatic mid-day reversal, lifting mortgage-backed securities from early weakness. UMBS 5.0 climbed 26 basis points to 97.61, while GNMA 5.0 gained 22 basis points to 98.06 after Iran peace agreement speculation sparked a bond rally around 1:17 p.m. The 10-year Treasury yield compressed 32 basis points to 4.556%, though afternoon newswires pushed back on optimistic reports, leaving gains tempered by day’s end.

Oil prices tracked perfectly with bond moves, confirming the market’s sensitivity to geopolitical developments. Markets remain at the mercy of headline-driven volatility with the Memorial Day weekend approaching. Mixed economic data underscored competing inflation and growth pressures, complicating the rate outlook for originators.

Building permits beat expectations at 1.442 million versus 1.39 million forecast, while housing starts came in hotter at 1.465 million. However, the Philly Fed Business Index crashed to -0.4 from 26.7 previously, signaling a sharp slowdown in regional manufacturing and business activity. Prices paid declined to 47.90 from 59.30, offering some relief on the inflation front.

These crosscurrents suggest the economy is cooling, which could eventually support rates if recessionary fears deepen. Congress advanced the ROAD to Housing Act this week, signaling a major policy shift toward treating housing supply as a national economic priority rather than a local planning issue. The amended bill encompasses manufactured housing, zoning incentives, adaptive reuse provisions, and barriers to local development.

For mortgage sellers, this matters significantly because supply constraints have become one of the industry’s biggest long-term headwinds. Lenders cannot rely indefinitely on refinancing the same borrowers—the market needs more transactions and housing mobility. Manufactured housing provisions drew immediate praise from the Mortgage Bankers Association and Community Lenders Association, indicating broad industry support.

**Locking vs Floating**

Headline-driven volatility will likely define Friday’s rate environment, particularly with a three-day weekend approaching.

Markets may attempt to reach a geopolitical milestone before the break, which could trigger another rally if successful, or pull back if momentum stalls. Borrowers should remain cautious about floating as near-term moves remain unpredictable. Lock advisories depend heavily on individual borrower risk tolerance given the current whipsaw dynamics.

**Today’s Events**

Building Permits (April): 1.442M vs. 1.39M forecast, 1.363M prior

Continued Claims (May 9): 1,782K vs. 1,790K forecast, 1,782K prior

Housing Starts (April): 1.465M vs.

1.41M forecast, 1.502M prior

Jobless Claims (May 16): 209K vs. 210K forecast, 211K prior

Philly Fed Business Index (May): -0.4 vs. 18 forecast, 26.7 prior

Philly Fed Prices Paid (May): 47.90 vs.

forecast unavailable, 59.30 prior

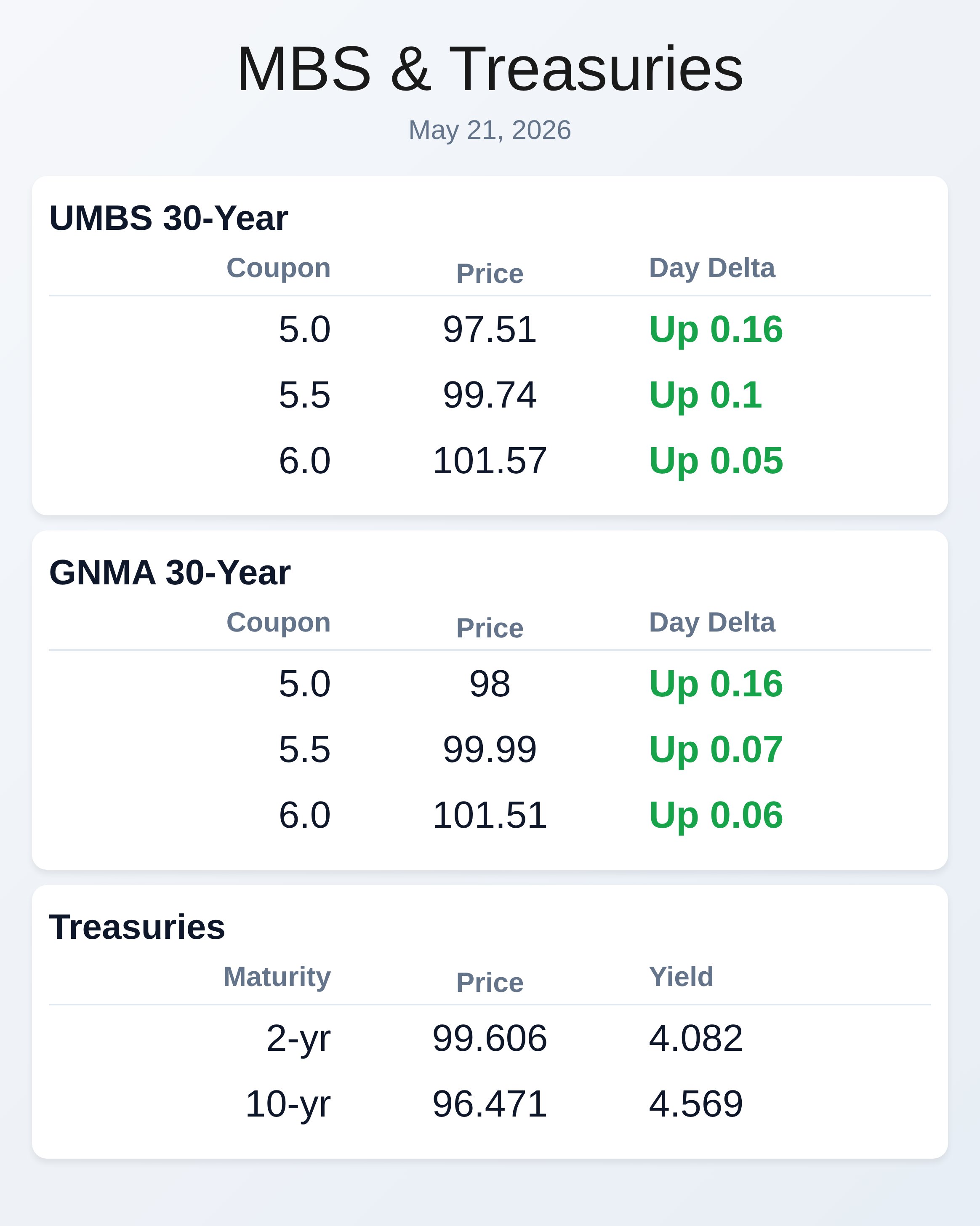

**Bond Pricing**

**UMBS 30 yr**

| Coupon | Price | Intra-Day Change |

**GNMA 30 yr**

| Coupon | Price | Intra-Day Change |

**Treasuries**

| Term | Yield | Price | Intra-Day Yield Change |