**WTMS Blog Today = What’s up in Mortgage Today (AM) – 06/01/2026**

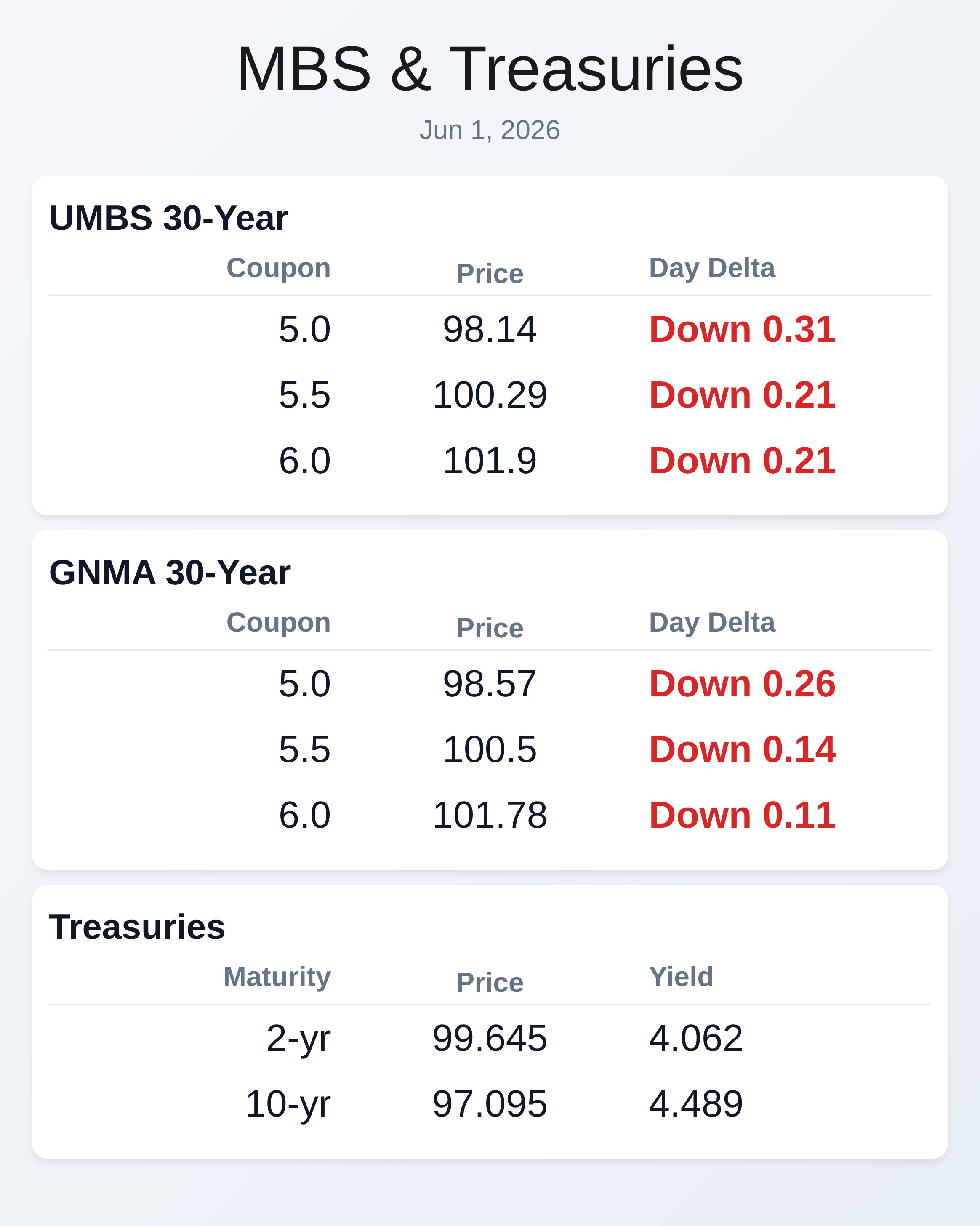

Markets turned skeptical of weekend peace headlines as Iran broke off nuclear negotiations, sending mortgage bonds lower and the 10-year Treasury yield up 3.6 basis points to 4.475 percent by mid-morning Monday. UMBS 5.5 coupon fell 21 ticks to 100.29 while GNMA 5.5 slipped 14 ticks to 100.5, reflecting renewed geopolitical risk and oil price rebounds that threaten the rate relief mortgage originators need. The Strait of Hormuz closure continues inflating supply chain costs and keeping inflation expectations sticky, which means the Federal Reserve is unlikely to cut rates anytime soon despite borrowers’ hopes for relief.

Bond traders are now pricing a 70 percent probability of a rate hike by December, a dramatic shift from earlier optimism about de-escalation and lower oil prices. Every day without a credible peace agreement adds uncertainty premium to the front end of the yield curve, keeping mortgage rates elevated and forcing lenders to manage volatile pipelines. Mortgage originators facing significantly softer June funding pipelines need to understand that current market dynamics favor defensive positioning rather than aggressive rate locking.

The 2s/10s curve remains inverted, meaning shorter-term rates carry more uncertainty about Fed policy than longer-term growth expectations. Once geopolitical risk subsides and oil prices normalize, expect the curve to re-steepen toward 50 basis points, signaling broader rate relief for borrowers and better lock-in opportunities. For now, the market is caught between stability in current economic data and persistent inflation from tariffs and war-related supply shocks.

Originators should prepare for continued volatility and advise borrowers that locking today protects against further upside risk, though rates may improve if negotiations resume credibly.

**Locking vs Floating**

Rates rallied solidly over the past week and a half as peace prospects improved, but that momentum reversed sharply today on new Iran headlines. More room for rate improvement exists when a peace deal actually materializes, but until then expect intraday whipsaws.

Borrowers sitting on the sidelines risk missing out if negotiations restart, yet locking now means locking in elevated levels that may prove unnecessary. Current volatility favors borrowers with moderate risk tolerance who split the difference by locking core business and floating marginal pipeline for potential weekend or week-ahead relief. The most prudent approach depends on borrower credit profiles and timeline urgency, but communications emphasizing geopolitical risk and energy prices will resonate better than discussing Fed policy alone.

**Today’s Events**

Final May S&P Global U.S. Manufacturing PMI at 9:45 a.m. ET.

ISM Manufacturing Index for May at 10:00 a.m. ET. U.S.

Treasury bill supply announcement for 3-month and 6-month bills at 11:30 a.m. ET. Friday’s May nonfarm payrolls report remains the week’s critical event, with expectations for 93,000 to 105,000 new jobs and unemployment rate holding steady at 4.3 percent or ticking up to 4.4 percent.

**Bond Pricing**

**UMBS 30 yr**

| Coupon | Price | Intra-Day Change |

| 5.0 | 98.14 | -0.31 |

| 5.5 | 100.29 | -0.21 |

| 6.0 | 101.9 | -0.21 |

**GNMA 30 yr**

| Coupon | Price | Intra-Day Change |

**Treasuries**

| Term | Yield | Price | Intra-Day Yield Change |

**GNMA 30 yr**

| Coupon | Price | Intra-Day Change |

|—:|—:|—:|

| 5.0 | 98.57 | -0.26 |

| 5.5 | 100.5 | -0.14 |

| 6.0 | 101.78 | -0.11 |

**Treasuries**

| Term | Yield | Price | Intra-Day Yield Change |

|—|—:|—:|—:|

| 2 yr | 4.062 | 99.645 | 0.061 |

| 3 yr | 4.111 | 98.291 | 0.061 |

| 5 yr | 4.201 | 98.545 | 0.057 |

| 7 yr | 4.34 | 99.465 | 0.056 |

| 10 yr | 4.489 | 97.095 | 0.05 |

| 30 yr | 5.007 | 96.033 | 0.039 |

Subscribe free at WellThatMakesSense.com for daily mortgage market intelligence and strategic insights for loan originators.