**WTMS Blog Today = What’s up in Mortgage Today (PM) – 07/15/2026**

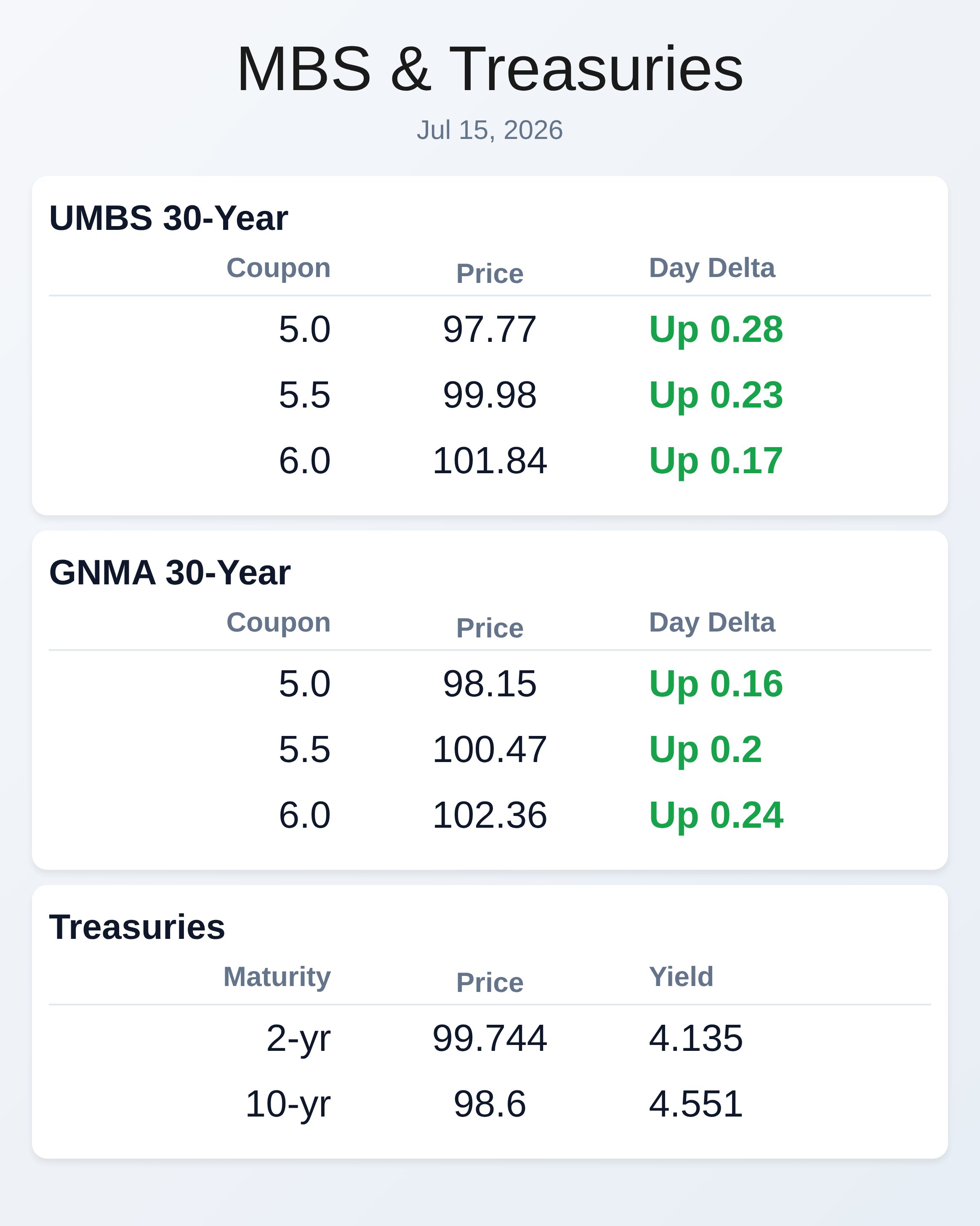

Bonds rallied steadily Wednesday on surprisingly weak inflation data, with the 10-year Treasury yield falling to 4.548% by afternoon, matching Tuesday’s post-data lows after PPI came in well below forecasts. Core PPI rose just 0.2% month-over-month versus 0.3% expected, while overall PPI actually fell 0.3% rather than holding flat, signaling persistent disinflation pressures despite earlier summer energy spikes. MBS prices strengthened throughout the day, gaining 22 basis points on UMBS 5.5s to 99.95, showing the rally had staying power unlike Tuesday’s CPI-driven pop that faded quickly.

The bond market’s resilience is notable given June’s lower fuel costs powered these gains, yet oil prices have since rebounded, creating genuine caution for momentum traders. Risk-tolerant originators can consider 4.61%–4.62% as an overhead lock trigger, but the critical resistance floor remains at 4.54%—breaking below requires conviction to soften the outlook further. UAD 3.6 appraisal form requirements take effect November 2nd for all GSE deliveries, yet fewer than 10% of lenders on major platforms have ordered a single 3.6 report, creating an execution crisis masked by summer deal flow.

The new standardized format replaces decades-old PDF workflows with hundreds of granular data fields covering property characteristics, designed to feed cleaner data into appraisal waiver and hybrid lending decisions. Appraisers face relearning entire inspection and software workflows, but form software from market leaders Cotality and First American remains glitch-ridden despite GSE verification, leaving many practitioners completing reports as 2.6 forms instead. Early adopters report 3.6 turnaround times starting at 3x slower than 2.6 work, improving to 25% slower with repetition, while both fees and frustration climb as AMCs drag on transition readiness.

Lenders must begin pilot testing immediately—not in October—to avoid delivery bottlenecks that could strand funded loans unable to reach GSEs. Wholesale pricing pressure continues flowing through the entire channel two years after UWM’s “All-In” policy severed Rocket Mortgage access through affiliated brokers. Academic research from the University of Kentucky now documents that competing lenders systematically lowered rates to capture borrowers blocked from Rocket, creating measurable spillover effects beyond UWM and its competitors.

VantageScore adoption remains marginal despite offering meaningful advantages for lower-credit borrowers, limited by lender LTV restrictions and credit score adjustment penalties that neutralize benefits on the borrower profiles where it matters most. UWM’s current 80% LTV cap on VantageScore conventional products eliminates the population most likely to see meaningful uplift, while a 20-point score haircut further dampens adoption signals. Expect minimal VantageScore market impact through early 2027 as current product constraints keep it practical for only a sliver of originations.

Mortgage applications fell 2.7% week-over-week as rates climbed to their highest level since August 2025, signaling demand destruction at the margin despite improved affordability news from weaker inflation prints. CFPB Acting Director Russell Vought faces congressional grilling over enforcement pullback, staffing cuts, deleted records, and an unexpectedly active rulemaking agenda—raising uncertainty over what regulatory guardrails remain for origination practices. Three ex-CFPB enforcement officials launched a new law firm, likely competing directly for mortgage industry clients seeking guidance as enforcement becomes unpredictable under new leadership.

First Horizon Bank promoted a 20-year veteran to lead its Baton Rouge market, signaling regional banks’ commitment to mortgage expansion even as wholesale channels face consolidation pressures. Non-QM securitizations remain active, with A&D Mortgage closing its fifth 2026 deal at $432.4 million, proving investor appetite for alternative documentation despite tight credit environment. The combination of softer inflation data, persistent rate resistance at 4.54%, and broad execution challenges across appraisal and origination workflows creates a compressed timeframe for competitive repositioning in H2 2026.

Originators locking clients at 4.61%–4.62% capture current strength while protecting against downside risk, yet the broader market signal remains cautious until yields convincingly break below the 4.54% floor. Capital markets remain sensitive to geopolitical oil dynamics and China trade developments, making today’s tactical gains fragile without fundamental momentum shift.

**Locking vs Floating**

Today’s additional gains create opportunities for risk-tolerant borrowers to lock at 4.61%–4.62% levels, but exercise caution given that yields failed to break yesterday’s post-CPI lows.

The critical resistance floor sits at 4.54%—breaking below that would meaningfully soften the bearish rate outlook and signal genuine trend strength rather than intraday tactical strength.

**Today’s Events**

Core PPI month-over-month (June): 0.2% vs. 0.3% forecast, 0.1% prior

Core PPI year-over-year (June): 4.7% vs.

5.2% forecast, 4.6% prior

PPI month-over-month (June): -0.3% vs. 0.0% forecast, 1.1% prior

PPI year-over-year (June): 5.5% vs. 6.2% forecast, 6.0% prior

**Bond Pricing**

**UMBS 30 yr**

| Coupon | Price | Intra-Day Change |

**GNMA 30 yr**

| Coupon | Price | Intra-Day Change |

**Treasuries**

| Term | Yield | Price | Intra-Day Yield Change |