**WTMS Blog Today = What’s up in Mortgage Today (AM) – 07/13/2026**

Geopolitical tensions in the Middle East are pushing yields higher and MBS prices lower as the U.S. and Iran escalate military strikes around the Strait of Hormuz. Crude oil jumped overnight, sending the 10-year Treasury yield to 4.59 percent and shaking equity markets with semiconductor stocks leading a selloff.

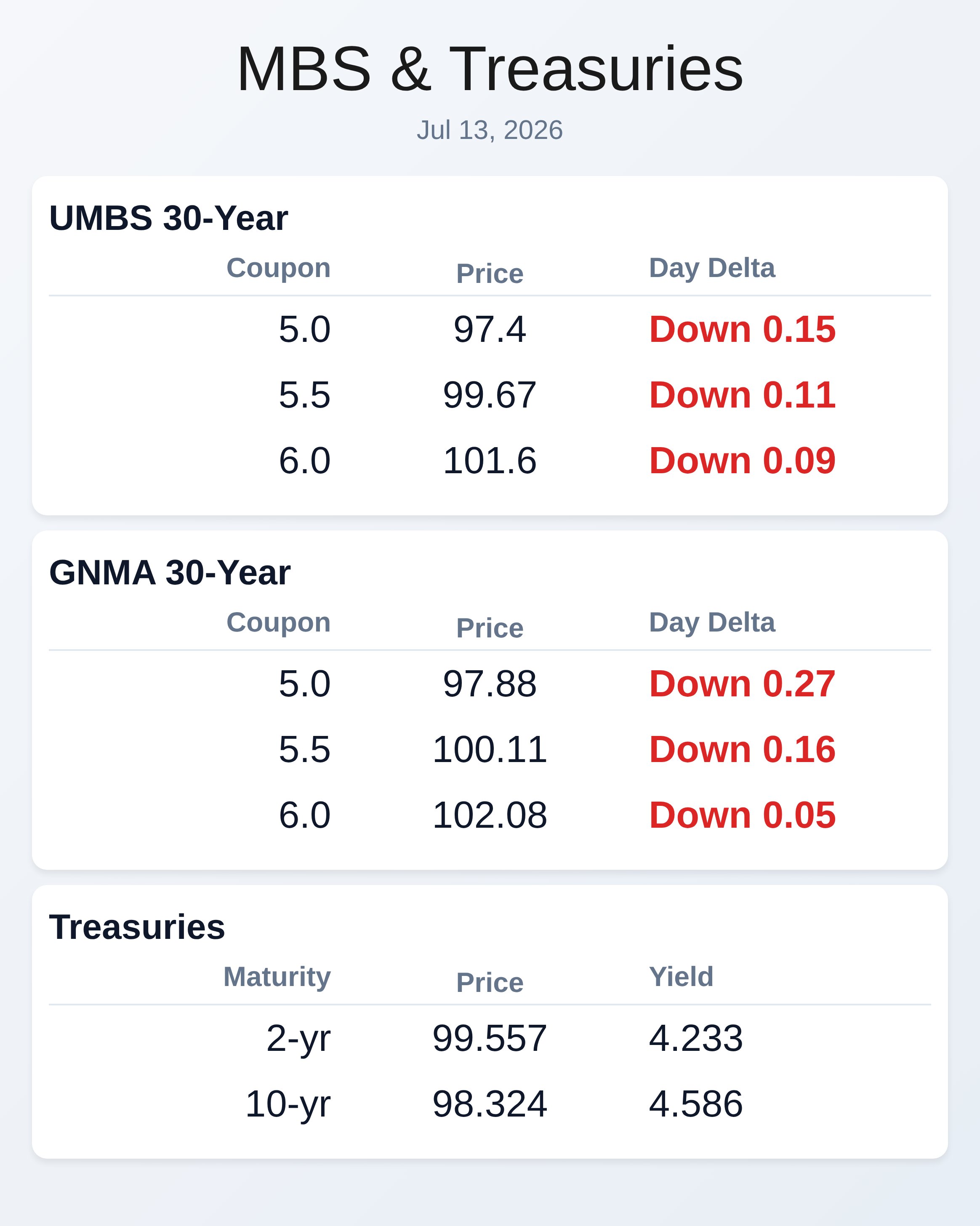

MBS investors face renewed weakness, with the 30-year UMBS 5.0 trading at 97.44, down 0.12 from the prior close. Bond market technicians view the 4.59 ceiling as critical resistance after last week’s eight-basis-point move higher. While financial markets are treating the escalation as negotiation theater rather than perpetual war, the inflation implications of higher oil prices are keeping duration traders on edge.

Financial engineers warn that energy-linked inflation remains the bigger concern than the geopolitical event itself. Oil’s seven-percent weekly gain pushed crude above $74 per barrel and drove longer-term yields upward despite Friday’s oversold technical setup. Treasury demand at last week’s auctions signaled investor appetite for duration, suggesting current yield levels may be acceptable to buyers stepping in.

The June Federal Open Market Committee Minutes indicated Fed officials remain data-dependent and skeptical of near-term rate hikes without persistent inflation evidence. Lenders should monitor this week’s Consumer Price Index report and Chair Warsh’s congressional testimony for clues on policy direction. The 10-year Treasury’s ability to hold above 4.59 will dictate whether repricing pressure eases for mortgage originators or accelerates.

Rate-sensitive lenders who did not adjust their sheets for Friday’s weakness face asymmetric risk on Monday morning without new bond strength. Risk-tolerant originators continue defending their float stance, betting that technical ceilings and oversold conditions will cap additional upside in yields. Shipping traffic through the Strait of Hormuz fell to five-week lows, underscoring supply chain anxiety even if markets believe the conflict remains manageable.

Mortgage pricing will remain volatile until CPI data and Fed testimony resolve uncertainty around inflation trajectory and monetary policy. Capital markets commentary from leading analysts suggests the selloff in South Korean chipmakers reflects broader AI trade fatigue rather than fundamental economic deterioration. A shift out of mega-cap technology stocks and into traditional sectors could benefit fixed-income buyers seeking stable duration in a sideways market.

The Bloomberg report noted that traders are positioning for possible Fed rate hikes as soon as September, contrary to recent Market expectations for a summer pause. Yet the Fed’s continued transparency in policy discussions and the June Minutes’ dovish lean suggest officials are in no rush to tighten further. Mortgage originators should prepare for continued volatility until inflation data confirms whether energy-price shocks will persist.

The Chrisman Commentary highlighted the passage of the 21st Century ROAD to Housing Act, which supports down payment and closing cost assistance for first-time homebuyers. This legislation reinforces the industry’s focus on affordability solutions and could expand origination opportunities in the FHA and DPA space. Meanwhile, MISMO’s new white paper on eNotes and eClosing guidance offers lenders a roadmap for digitizing mortgage workflows to reduce costs and speed liquidity.

Technology providers are racing to implement UAD 3.6 compliance and AI-powered appraisal tools before industry adoption accelerates. Non-QM and HELOC lenders continue offering July promotions, with pricing improvements of up to 25 basis points for niche borrower segments. Pipeline management remains critical as the mortgage market navigates geopolitical uncertainty and seasonal summer slowdowns in origination volume.

Major banks including JPMorgan Chase, TD Bank, and Zillow Home Loans are actively recruiting high-performing loan officers, signaling confidence in pipeline growth through year-end. Employment trends across the industry show demand for experienced originators, appraisal managers, and operations leaders who can drive technology modernization. The Chrisman Job Board and industry conferences including the Western Secondary Market Conference in August provide networking and hiring platforms for growth-focused lenders.

Mortgage professionals should capitalize on promotional pricing and emerging talent opportunities while yields remain elevated and market dislocations persist.

**Locking vs Floating**

Mortgage originators who failed to reprice for Friday’s weakness face slight asymmetric risk favoring rate locks on Monday. The 10-year Treasury’s technical ceiling at 4.59 percent offers a defensive level if bond buyers step in and stabilize yields.

Risk-tolerant lenders defending their float stance should recognize that geopolitical catalysts like Middle East escalations are unpredictable and could trigger sharp intraday reversals. Shipping disruptions and crude oil strength justify caution, but market participants believe the conflict remains manageable rather than systemic. Lenders with tighter rate sheets should consider modest repricing to account for weekend weakness unless news flow stabilizes by market open.

**Today’s Events**

No scheduled economic data releases are listed for today. The week begins quietly but Fed Chair Warsh’s congressional testimony and the June Consumer Price Index report are due tomorrow. Additional data points this week include PPI, jobless claims, housing data, industrial production, and the Fed’s Beige Book.

Short-duration Treasury auctions and remarks from Fed members Bowman and Waller are also on the calendar.

**Bond Pricing**

**UMBS 30 yr**

| Coupon | Price | Intra-Day Change |

**GNMA 30 yr**

| Coupon | Price | Intra-Day Change |

**Treasuries**

| Term | Yield | Price | Intra-Day Yield Change |