**WTMS Blog Today = What’s up in Mortgage Today (AM) – 07/08/2026**

Geopolitical tensions reignited overnight as Trump declared Iran’s ceasefire “over” following attacks on commercial vessels in the Strait of Hormuz and subsequent U.S. retaliatory strikes, sending oil prices up nearly six percent and mortgage rates higher across all coupons. The 30-year fixed rate moved to 6.63 percent as crude oil surged, reinforcing the simple equation that higher oil equals higher inflation and elevated rates.

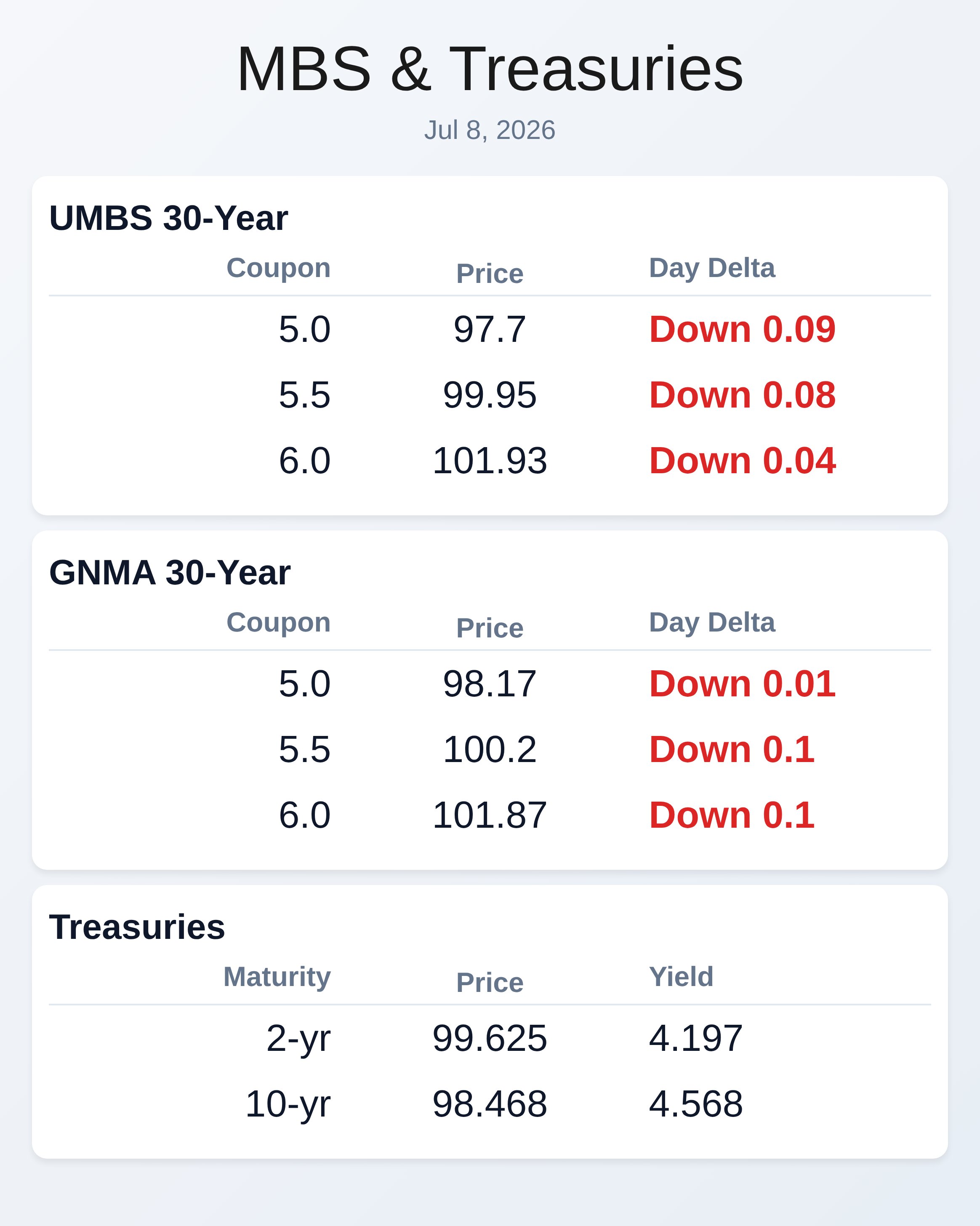

Mortgage-backed securities weakened sharply with the 10-year Treasury yield climbing to 4.568 percent on the day, though the market’s morning reaction proved modest at only 3 ticks (.09) lower on UMBS. Most traders expect next week’s consumer price data and ongoing Federal Reserve positioning to dominate market movement more than geopolitical headlines. Despite the volatility, refinance opportunities remain extremely limited with year-over-year basis points shrinking to just 19 points below historical thresholds.

Mortgage demand contracted for the second consecutive week as total application volume dropped 2.2 percent for the week ending July 3, with refinance applications falling 4 percent and purchase applications declining 1 percent on a seasonally adjusted basis. The weakness reflects Fourth of July holiday seasonality combined with elevated rate levels that continue to suppress refinancing activity. Purchase applications remain five percent higher year-over-year while refinances sit eight percent above last year’s level, but these comparisons offer little comfort to lenders facing historically depressed refinancing spreads.

Government-backed VA purchase applications rose five percent for the week, suggesting lower-down-payment products are gaining traction as conventional purchase activity softens. The MBA refinance index remains near historical lows, pointing to minimal prospects for a meaningful refinance wave unless rates drop substantially. VantageScore released a white paper claiming its 4.0 credit model can identify more than five million creditworthy borrowers that FICO Score 10T cannot, potentially unlocking up to one trillion dollars in origination volume.

The company attributes this broader reach to machine learning, trended credit data, and alternative payment histories including rent, telecom, and utility payments, which it says provides 400 percent more data than legacy FICO models when assessing thin-file borrowers. This competitive challenge to FICO’s dominance comes as lenders increasingly seek tools to expand credit box access in a tight refinance environment. The dispute underscores ongoing tension between traditional credit scoring methodologies and newer approaches that leverage alternative data sources.

For mortgage originators, this development means potential access to previously unavailable borrower populations if lenders adopt VantageScore’s expanded framework. Better Mortgage settled an underwriter overtime wage lawsuit for 7.185 million dollars, reflecting broader labor cost pressures facing large lending platforms. Lennar stock declined following intensified litigation with a Florida Native American tribe over allegedly uninhabitable homes constructed on tribal land, a lawsuit that began gaining traction nearly a year ago.

Former Stockton Mortgage employees denied allegations they orchestrated a mass departure to competitor Novus Home Mortgage and stole borrower data and trade secrets. Equity Prime Mortgage announced it would deliver full loan disclosures in six languages, positioning itself as the only 100 percent third-party lender offering such comprehensive language access. These diverse industry developments highlight ongoing regulatory scrutiny and operational challenges facing mortgage lenders across multiple fronts.

**Locking vs Floating**

Caution remains warranted given weak follow-through after recent attempts to hold mortgage rates below 4.42 percent on the 10-year Treasury. The 4.51 percent technical ceiling on the 10-year has now been challenged, and war-related headlines continue introducing additional volatility to an already uncertain market. Mortgage-backed security price movements provide intraday risk signals, while 10-year yield ceilings and floors help track longer-term bond market momentum, offering mortgage sellers critical insight into macro positioning beyond daily noise.

**Today’s Events**

MBA mortgage applications for the week ending July 3 reported early morning; May wholesale inventories, weekly crude oil inventories, June FOMC minutes, May consumer credit, and a Treasury auction of 39 billion dollars in 10-year notes all scheduled for later in the session.

**Bond Pricing**

**UMBS 30 yr**

| Coupon | Price | Intra-Day Change |

| 5.0 | 97.7 | -0.09 |

| 5.5 | 99.95 | -0.08 |

| 6.0 | 101.93 | -0.04 |

**GNMA 30 yr**

| Coupon | Price | Intra-Day Change |

| 5.0 | 98.17 | -0.01 |

| 5.5 | 100.2 | -0.1 |

| 6.0 | 101.87 | -0.1 |

**Treasuries**

| Term | Yield | Price | Intra-Day Yield Change |