**WTMS Blog Today = What’s up in Mortgage Today (AM) – 07/07/2026**

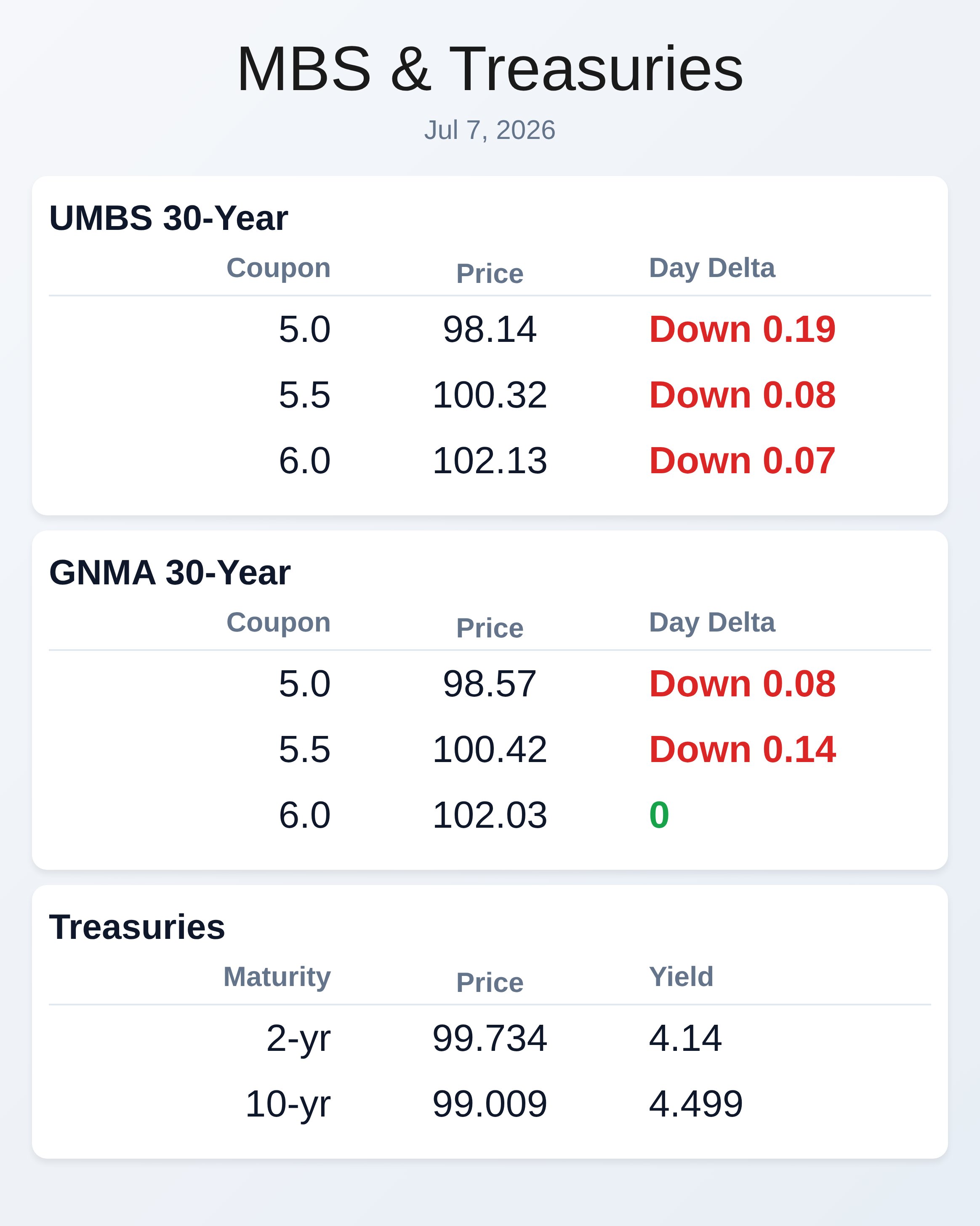

Bond markets opened Tuesday with modest downward pressure as Amazon’s $25 billion debt offering signaled corporate borrowing momentum, pushing the 10-year Treasury yield up 2.1 basis points to 4.492 percent by morning. UMBS securities declined across coupons, with the 5.0 coupon down 0.19 and the 6.0 coupon down 0.07, while GNMA 5.5 coupons fell 0.14 points in early trading. The overnight weakness followed a weekend hold above the 4.51 percent ceiling, though risk-tolerant clients view continued price support as constructive relative to yesterday’s close.

MBS investors remain focused on supply dynamics and issuance trends as the spring homebuying season gradually fades into summer activity patterns. Agency MBS supply continues recovering from 2023 lows, with refinancing activity driving growth even as purchase originations remain modest. Equity volatility in semiconductor stocks, particularly Samsung’s 11 percent Seoul tumble despite record AI-driven profits, added overhead pressure to risk sentiment and tempered bond demand.

Oil prices rose on Strait of Hormuz shipping attacks, climbing to $72.60 per barrel for Brent crude, which historically correlates with inflation expectations and bond yield movements. The week ahead brings the Federal Open Market Committee minutes release, which markets expect could reveal shifts in the Fed’s inflation assessment given uncertain labor market data and mixed price pressures. Private payroll data from ADP showed just 21,000 average weekly gains through mid-June, suggesting continued labor market softness that may inform near-term Fed deliberation.

While core inflation remains a concern for some officials, softer employment trends and retreating oil prices have raised the bar for immediate monetary policy action. Mortgage industry focus shifted toward capacity and operational readiness as November 2 approaches for Universal Appraisal Dataset 3.6 implementation. Lenders considering the deadline as early October rather than November must coordinate with appraisers, technology vendors, and GSE workflows to ensure seamless UAD 3.6 adoption.

The MISMO leadership acknowledged the industry is not ready operationally, despite vendor technology being largely developed, because interconnected systems require coordinated change across thousands of firms. Summer activity typically lightens trading volume and hedging activity, which aligns with current subdued TBA hedge volumes and specified pool trading patterns observed this week. Disciplined pricing and attention to issuance patterns remain critical as volatility persists and mortgage lenders navigate a range-bound rate environment.

Consumer behavior continues reshaping mortgage origination workflows, with technology increasingly serving as a friction-reduction tool rather than a loan officer replacement. Zillow’s integration of pre-approval verification into home search exemplifies how digital experiences work best when they remove confusion and organize information around borrower questions. Only 28 percent of prospective buyers achieve pre-approval before searching for homes, leaving substantial opportunity for lenders to enhance transparency and compress decision timelines.

The most successful digital strategies eliminate routine work while preserving human expertise for judgment, problem-solving, and relationship management. Title services integration into transaction management software further streamlines closing workflows and reduces delays for borrowers and professionals alike. Today’s economic calendar includes May import and export prices, the May trade balance, Redbook same-store sales, June consumer inflation expectations, and the Atlanta Fed’s GDPNow for Q2.

A three-year Treasury note auction occurs this afternoon, which will provide market guidance on near-term demand for intermediate-duration fixed income. These data releases and auctions carry subdued importance given their lower market sensitivity compared to employment and inflation prints. Market participants remain positioned for patience from the Fed while awaiting clearer catalysts for directional rate movement.

No major surprises are expected today, leaving bond markets likely to consolidate within established technical ranges.

**Locking vs Floating**

Caution remains appropriate due to lack of follow-through below the 4.42 percent 10-year yield level, though the weekend hold above the 4.51 percent ceiling provides some encouragement. Risk-tolerant clients welcomed bonds holding ground, suggesting 4.51 percent as a conservative lock trigger with 4.57 percent available as a more aggressive option.

These yield ceilings and floors help track bigger-picture bond market momentum beyond intraday MBS price fluctuations. Current weakness and overnight corporate bond supply represent headwinds, but employment softness and oil price reversal offer offsetting support. Monitor Fed communications and economic data before committing rate locks given volatile positioning.

**Today’s Events**

May Import and Export Prices | May Trade Balance | Redbook Same Store Sales | June Consumer Inflation Expectations | Atlanta Fed GDPNow (Q2) | 3-Year Treasury Note Auction

**Bond Pricing**

**UMBS 30 yr**

| Coupon | Price | Intra-Day Change |

| 5.0 | 98.14 | -0.19 |

| 5.5 | 100.32 | -0.08 |

| 6.0 | 102.13 | -0.07 |

**GNMA 30 yr**

| Coupon | Price | Intra-Day Change |

| 5.0 | 98.57 | -0.08 |

| 5.5 | 100.42 | -0.14 |

| 6.0 | 102.03 | 0 |

**Treasuries**

| Term | Yield | Price | Intra-Day Yield Change |

| 2 yr | 4.14 | 99.734 | 0.028 |

| 3 yr | 4.164 | 99.891 | 0.031 |

| 5 yr | 4.231 | 99.526 | 0.035 |

| 7 yr | 4.358 | 99.354 | 0.028 |

| 10 yr | 4.499 | 99.009 | 0.029 |

| 30 yr | 5.012 | 99.818 | 0.025 |