**WTMS Blog Today = What’s up in Mortgage Today (AM) – 07/01/2026**

The sell-off that defined Tuesday is holding into Wednesday as mortgage-backed securities decline and Treasury yields rise, signaling investor caution ahead of major economic data and Federal Reserve commentary. MBS prices are down broadly, with the 10-year yield climbing to 4.49 percent after closing at 4.42 percent yesterday, extending quarterly weakness as markets price in lingering inflation concerns. A softer-than-expected June ADP jobs report showing just 98,000 private-sector job additions versus forecasts of 113,000 has failed to provide relief, with selling continuing across the curve despite month-end rebalancing pressure.

Federal Reserve Chair Kevin Warsh will speak today at 9 a.m. alongside European central bank officials in Portugal, and his remarks on price stability could set the tone for rate expectations through year-end. Holiday-shortened trading and lower market participation are keeping volatility elevated, making a defensive positioning strategy prudent until market direction becomes clearer.

Geographic disparities and loan size continue to drive uneven mortgage-backed securities performance, as some high-cost coastal markets outperform while Southern and Southwestern regions lag behind. Home price growth has cooled nationally without meaningfully improving affordability, creating a patchwork where borrowers in expensive markets face persistent headwinds while cheaper regions lose momentum. The FHFA index showed a slight monthly decline, yet home values remain stubbornly above levels that would ease mortgage origination demand.

This regional divergence means originators in slower-appreciation areas may face tighter margins and lower volume, while those in hot markets could see slightly better pricing. Understanding local market conditions is essential for locking rate risk and managing wholesale pricing. The labor market continues signaling strength despite the ADP disappointment, with private-sector job creation capping the best three-month stretch in more than a year and wage growth for job-changers accelerating to 6.6 percent annually.

Tomorrow’s official June payroll report is expected to show 115,000 net new jobs, which would mark the strongest six-month hiring streak since mid-2024 and support arguments for potential Federal Reserve rate increases. Job openings remain elevated relative to available workers, particularly in education, health services, and financial sectors, pointing to labor supply constraints rather than broad weakness. These employment trends continue to pressure the Fed’s rate-pause narrative, as policymakers must balance improving inflation data with persistent labor strength.

Originators should monitor tomorrow’s jobs report closely, as an outsized number could reignite rate-hike expectations and trigger bond market selling. Consumer confidence edged higher in June only after a downward revision to May’s reading, masking mixed underlying economic momentum that keeps Fed officials uncertain about the inflation trajectory. Business activity moderated while job openings remained stable, suggesting the economy is losing steam without deteriorating sharply—the textbook soft-landing scenario markets currently price.

Headline inflation has eased thanks to lower energy prices, but core inflation persists stubbornly, preventing the Fed from declaring victory and moving to rate cuts. The disconnect between cooling goods prices and sticky services inflation means policymakers will require more employment and inflation data before adjusting policy. Originators facing borrower rate-lock decisions should focus on data dependency risk rather than calling a clear directional trend.

Mortgage applications from the Mortgage Bankers Association were essentially flat for the week ending June 26, with purchase activity rising 1 percent week-over-week and up 3 percent year-ago, while refinance applications fell slightly but remain 9 percent above year-ago levels. This stability in application flow despite modestly higher rates suggests borrower demand remains genuine rather than driven by tactical window-shopping, though seasonal weakness could arrive as we enter summer months. May construction spending and today’s June ISM Manufacturing Index will provide additional color on economic momentum heading into the second half.

Purchase applications outpacing refinance growth indicates healthy housing demand relative to refi activity, a healthy diversification for origination pipelines. Monitor application trends closely as the busiest summer season approaches and rate volatility potentially increases. Trust and referrals, not artificial intelligence or online search, continue driving borrower lender selection, with less than 2 percent of refinance borrowers and just 4 percent of purchase borrowers finding lenders through online search, reviews, or AI recommendations combined.

Instead, nearly 90 percent of borrowers still select lenders through referrals, existing relationships, and prior experience, meaning the fundamental mortgage business remains relationship-driven despite industry hype around technology innovation. This reality underscores why customer experience, operational efficiency, and referral network strength matter far more than AI adoption for capturing market share. Originators chasing cutting-edge technology while neglecting core borrower experience and referral cultivation are misallocating resources and missing growth opportunities.

The lesson for mortgage professionals is clear: invest in people, processes, and relationships first; then layer in technology that enhances rather than replaces human connection.

**Locking vs Floating**

Tuesday’s volatility suggests borrowers and originators should maintain a more defensive stance through the end of this shortened week. Higher risk events remain on the calendar—Fed commentary today, tomorrow’s jobs report, and weekly economic data—making aggressive rate-lock strategies risky.

The combination of technical bounce recovery, lower holiday-week participation, and elevated uncertainty argues for protecting rate risk until clearer directional confirmation emerges. Traders are watching intraday MBS price movements and 10-year yield ceiling and floor levels to gauge broader bond market momentum, with Thursday’s payroll data potentially serving as the next major catalyst.

**Today’s Events**

ADP private-sector payrolls (June): 98,000 vs.

113,000 forecast, 122,000 prior

Federal Reserve Chair Kevin Warsh speaks at 9 a.m. ET in Portugal alongside European central bank officials

Final June S&P Global U.S. Manufacturing PMI

May Construction Spending

June ISM Manufacturing Index

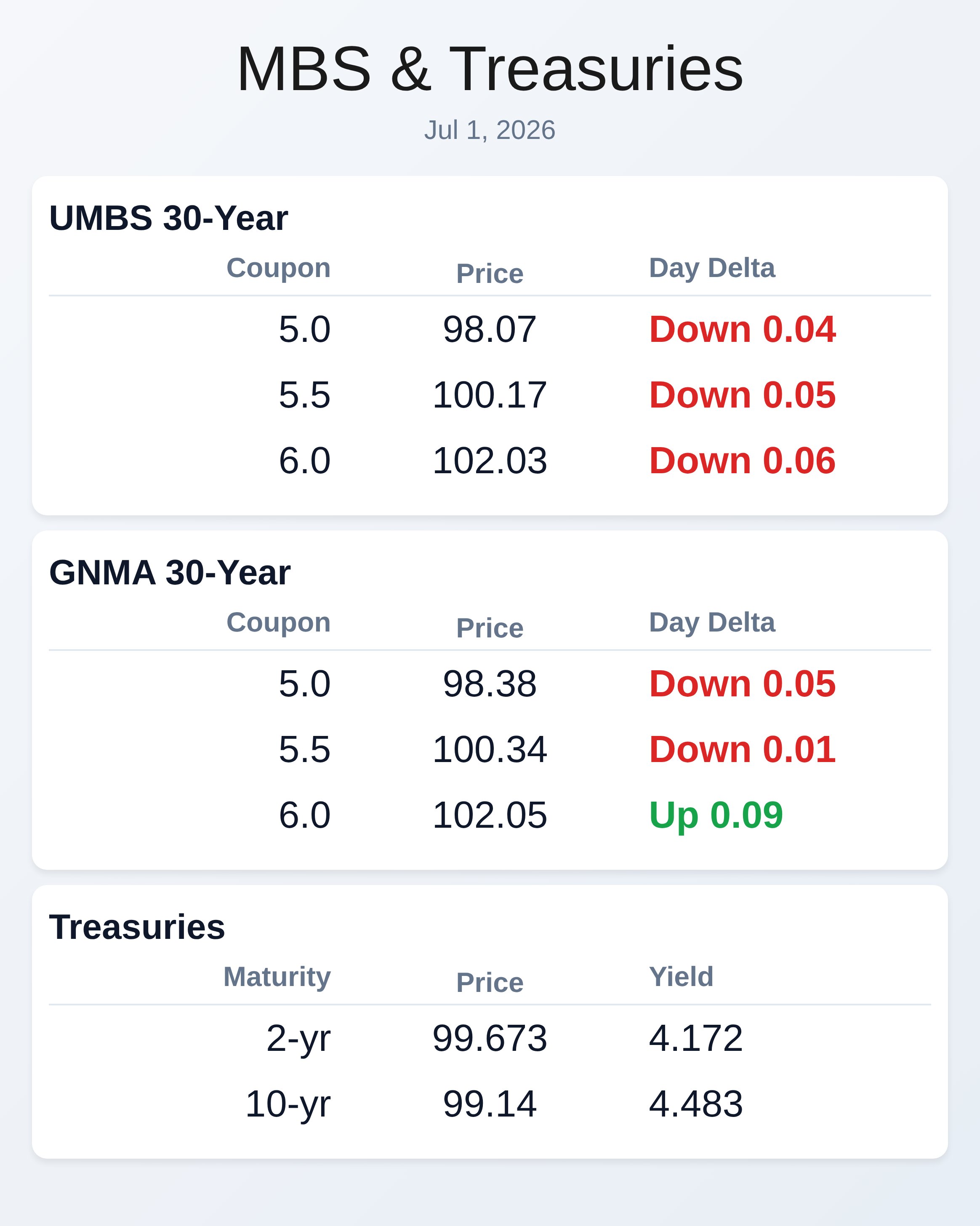

**Bond Pricing**

**UMBS 30 yr**

| Coupon | Price | Intra-Day Change |

| 5.0 | 98.07 | -0.04 |

| 5.5 | 100.17 | -0.05 |

| 6.0 | 102.03 | -0.06 |

**GNMA 30 yr**

| Coupon | Price | Intra-Day Change |

| 5.0 | 98.38 | -0.05 |

| 5.5 | 100.34 | -0.01 |

| 6.0 | 102.05 | 0.09 |

**Treasuries**

| Term | Yield | Price | Intra-Day Yield Change |

| 2 yr | 4.172 | 99.673 | -0.004 |

| 3 yr | 4.184 | 99.835 | 0.002 |

| 5 yr | 4.237 | 99.502 | 0.008 |

| 7 yr | 4.352 | 99.391 | 0.014 |

| 10 yr | 4.483 | 99.14 | 0.017 |

| 30 yr | 4.978 | 100.335 | 0.016 |