—

WTMS Blog Today = What’s up in Mortgage Today (PM) – 04/15/2026

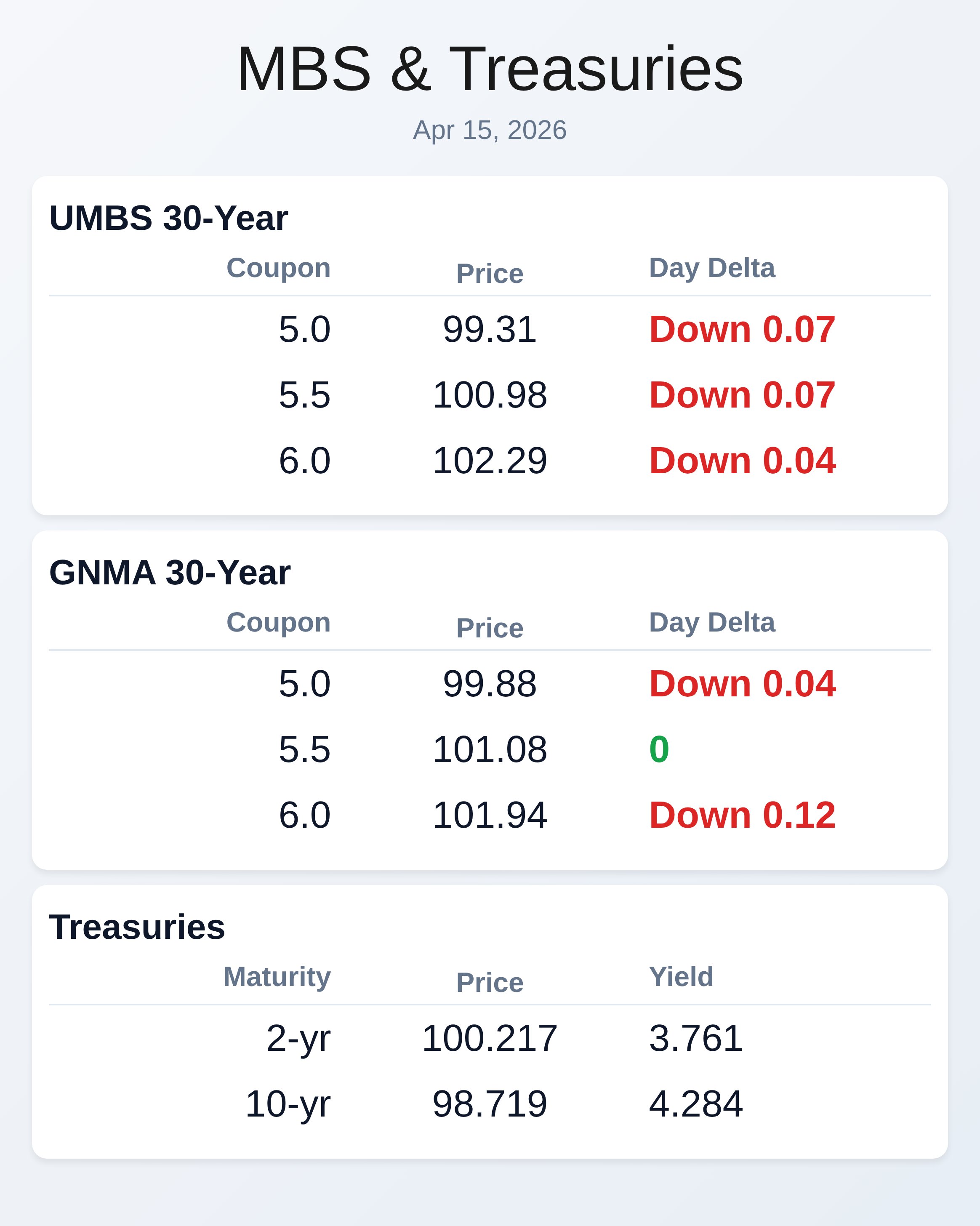

Mortgage origination ground to a halt today as the market staged only a token pullback, with UMBS 5.0 prices down just 0.10 and the 10-year Treasury yielding 4.28 percent. Wholesale import price data disappointed, rising 0.8 percent month-over-month against a 2 percent forecast, yet the broader inflation narrative remains stubbornly elevated above the Federal Reserve’s 2 percent target. The ceasefire agreement between the U.S.

and Iran this week caused oil to plummet over 15 percent, yet bond markets remain unmoved—signaling that geopolitical relief alone won’t restart the rate rally many originators are banking on. Energy prices remain the tether connecting Fed policy uncertainty to borrower expectations; as long as this uncertainty persists, originators should expect sideways movement rather than sustained directional breaks. Recent Fed minutes revealed growing unease among policymakers about inflation staying above target, with several officials now opening the door to potential rate hikes if conditions deteriorate.

Mortgage rates have become decoupled from Fed cuts that occurred earlier this year, and that structural shift changes everything for origination business models. The traditional playbook—Fed cuts, mortgage rate declines, refi volume surges—has broken down because Treasury yields are climbing independently of Fed policy, driven largely by rising federal debt and deficit concerns. This means longer-term rates can stay elevated even when the Fed is easing, which is exactly what we’re seeing right now with the short end lower but the 10-year stuck above 4.25 percent.

For loan officers, this forces a pivot away from waiting-for-rates-to-fall strategies and toward building sustainable purchase pipelines with disciplined rate-lock discipline. Refinance activity did surge in March, reaching 25 percent of total lock volume (its highest since September 2024), but that bump reflected borrowers chasing marginal improvements rather than a true inflection point. Product strategy and borrower positioning matter far more now than they did when rate direction was predictable.

The Fed’s March meeting minutes exposed deep internal conflict about the path forward. Some participants saw a strong case for signaling that the Fed might hike rates again if inflation persists, while others emphasized the downside risks to employment from prolonged geopolitical turmoil and elevated energy costs. The consensus leaning remains toward eventual rate cuts, with most officials still viewing a protracted Middle East conflict as serious enough to warrant additional easing beyond cuts already priced in.

However, the mere presence of hawkish voices in the minutes spooked rate traders and kept yields bid up throughout the afternoon. This mixed messaging translates to origination reality: lock-in clients quickly on improvement windows, but maintain flexibility because the next headline could swing the market either way. Technicals show the 10-year holding firm above the 4.12-percent floor, with a 4.34-percent ceiling acting as near-term resistance.

Economic data flow remains light, with only import prices and manufacturing sentiment released today. The New York Fed Manufacturing Index surged to 11.00, crushing expectations of a 0.5 decline, signaling manufacturing strength that defies the broader narrative of labor-market softness. Builder confidence slipped to 34 from 38, continuing the multi-month trend of housing pessimism as affordability collapses.

These mixed signals—strong manufacturing, weak housing demand, sticky inflation—have left bond traders frozen, unsure which economic story will dominate. Markets are waiting for the next big geopolitical escalation or permanent ceasefire announcement to move, as traders view the current equilibrium as temporary. Nothing here justifies locking borrowers unless rates actually move; floating remains the prudent stance for most scenarios.

Home sales collapsed to their slowest pace since 2009 in March, with existing-home transactions declining 3.6 percent month-over-month and dragging median prices down despite year-over-year gains in the South and West. Lower consumer confidence and softer job growth are creating a bifurcated market where only well-qualified borrowers in strong equity positions are moving. This slowdown contradicts assumptions that refi activity alone could sustain origination pipelines; purchase volume is the true barometer of business health, and right now it’s anemic.

The White House’s latest economic report acknowledged this affordability crisis and called for policy attention to rates, housing supply, and lending competition—a tacit admission that the government sees mortgage rates as an ongoing political problem. For originators, this underscores the urgency of shifting focus toward builder-sponsored financing, cash-out refi packages, and non-QM products that can capture borrowers priced out of traditional programs. Pricing remains soft across both UMBS and GNMA coupons, with no real conviction on either side of the bid-ask.

UMBS 5.5 fell 0.08 basis points, while the 6.0 coupon lost only 0.04, suggesting slight demand for premium coupons despite the overall weakness. GNMA 5.5 held flat, but the 6.0 coupon dropped 0.12, indicating some rotation into higher coupons ahead of potential rate moves. Lock-float decisions should hinge on client rate expectations and pipeline timeline rather than trying to game the 48-hour rally windows that have become the market’s only reliable pattern since the Iran conflict began.

Originators who can position clients around natural refi windows while locking younger borrowers before the next leg of volatility will outperform those waiting passively for a rate environment that may never fully cooperate again.

Locking vs Floating

Winning streaks in this market have proven limited to two-day windows, making extended floats dangerous without a clear rate-improvement thesis. Light economic data and subdued geopolitical headlines mean bonds are content to “kick the can,” maintaining sideways trading that favors neither longer floats nor aggressive locking.

Originators should lock clients showing rate sensitivity or shorter decision timelines, while float-capable borrowers with 3-plus week pipeline windows can afford patience—but only if they have meaningful rate floors or aggressive repricing agreements.

Today’s Events

Import prices (MoM, Mar): 0.8% vs. 2.0% forecast, 1.3% previous

NY Fed Manufacturing Index (Apr): 11.00 vs.

−0.5 forecast, −0.20 previous

NAHB Builder Confidence Index: 34 vs. 37 forecast, 38 previous

Bond Pricing

UMBS 30 yr

| Coupon | Price | Intra-Day Change |

GNMA 30 yr

| Coupon | Price | Intra-Day Change |

Treasuries

| Term | Yield | Price | Intra-Day Yield Change |