—

WTMS Blog Today = What’s up in Mortgage Today (PM) – 04/21/2026

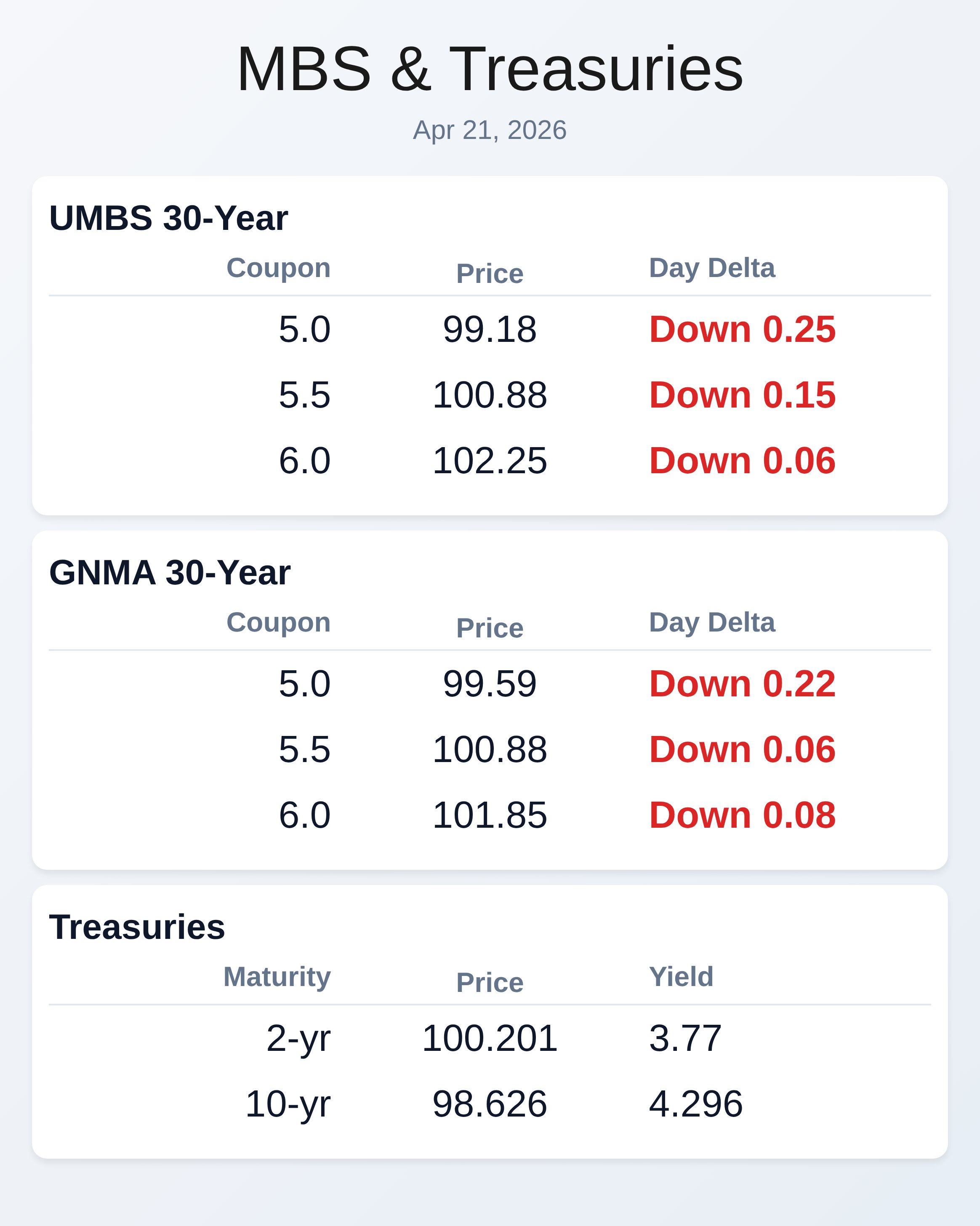

Geopolitical tensions over a stalled Iran ceasefire sent mortgage-backed securities down a quarter point by afternoon close, forcing lenders to weigh repricing risks as bond volatility remains elevated heading into Wednesday. The 10-year Treasury yield climbed 4.4 basis points to 4.297% amid headline swings between war escalation and diplomatic extensions, leaving market participants watching for any breakthrough in negotiations before the deadline expires. UMBS 5.0 traded at 99.18 and GNMA 5.0 at 99.60, reflecting weakness across the curve as risk-off sentiment briefly drove investors toward safety.

Earlier, strong March retail sales data—up 1.7% versus 1.4% forecast—failed to rattle bonds, suggesting traders remain glued to Middle East headlines rather than economic data. The market coped with today’s uncertainty in “a fairly calm way,” per MBS Live, though negative reprices remain possible if volatility persists through close. Edge Home Finance just secured strategic capital from Presidio Investors, a signal that venture money continues flowing into the broker model despite mounting origination pressure.

Tom Ahles, the company’s new president, made it crystal clear: no pivot to banking, no shift to correspondent lending—just scale the broker platform harder. When founders double down rather than diversify after raising capital, it reveals where conviction sits in a fragmented mortgage ecosystem dominated by UWM ($164.3B) and Rocket ($116.2B), yet carved up by hundreds of regional players. The move underscores that capital today favors platform agility and specialization over the traditional correspondent or bank balance-sheet models that defined mortgage growth for decades.

For smaller originators, this signals an existential choice: grow bigger or find a defensible niche fast. Retail sales crushed expectations at 1.7% month-over-month for March, beating the 1.4% forecast and marking the strongest monthly gain in a year despite war-fueled oil spikes. Consumer spending on merchandise remained resilient across categories, suggesting Americans continue to absorb inflation and higher energy costs without slowing their purchasing pace.

The control group—which excludes volatile auto and gasoline sales—also beat, advancing 0.7% against a 0.2% forecast, hinting that underlying demand strength runs deeper than headline numbers. Yet this economic resilience hasn’t lifted the mortgage market, as geopolitical risk continues to override positive domestic data and cap bond strength. Originators watching pending home sales (up 1.5% versus 0.1% forecast) see a spring home-buying season taking shape, though rates remain a structural headwind to refinance volume.

Volatility risk intensifies heading into Wednesday due to the ceasefire deadline combined with uncertain peace negotiations, though intraday swings today proved manageable despite headline whipsaws. Neither JD Vance nor Iran confirmed attendance at Wednesday’s scheduled talks in Pakistan, sparking a brief selloff that pushed MBS down nearly three-eighths of a point by mid-afternoon before Trump extended the ceasefire, triggering a partial recovery. Oil prices spiked above $96 a barrel as traders repriced the war premium, and Treasury yields climbed in lockstep with equities selling off sharply after earlier all-time-high momentum.

Mortgage originators already repricing borrowers saw losses between an eighth and a quarter point depending on timing and coupon, while some lenders remained in motion with reprices at close. The path forward depends entirely on whether geopolitical talks produce an actual framework or collapse again Wednesday night. Kevin Warsh, President Trump’s Federal Reserve nominee, testified before the Senate Banking Committee that the Fed needs a “different, new inflation framework,” sidestepping specifics on rate-cut timing.

Warsh blamed the central bank for allowing post-pandemic inflation to surge and acknowledged that hard-working Americans continue to feel elevated prices despite recent deceleration in the rate of change. When pressed on Trump’s public pressure for rate cuts, Warsh said independence is ultimately the Fed’s call, a careful response that avoids appearing captured while acknowledging executive preference. With $192 million in reported assets, Warsh would become one of the wealthiest Fed officials in history if confirmed, though conflicts-of-interest disclosures and asset sales remain pending.

This testimony signals that whoever leads the Fed will likely maintain focus on inflation rather than capitulate fully to Trump’s cutting rhetoric, suggesting mortgage originators shouldn’t expect aggressive rate relief in 2026. The mortgage origination market remains bifurcated: scale leaders like UWM and Rocket dominate with combined $280.5 billion in production, while second-tier players from JPMorgan Chase ($59.4B) through Pennymac ($35.4B) compete fiercely, and a long tail of nonbanks, IMBs, and regional specialists carve out niche segments. Banks skew toward larger loan balances while specialized lenders target specific borrower cohorts, creating a fragmented ecosystem where profitability matters more than raw volume in today’s compressed-margin environment.

Edge Home Finance’s capital raise reinforces that investors now reward platform efficiency, technology integration, and market positioning over mere production scale. For your business, this means the 2026 playbook requires ruthless cost discipline, differentiated customer acquisition, and defensible moat—not just more volume. The winners this cycle will be those who can scale lean operations that turn profit on 60 basis points instead of chasing 300-basis-point pipelines built in the 2020s.

\n\n

Locking vs Floating

Volatility risk intensifies heading into Wednesday owing to the ceasefire deadline and uncertain status of ongoing peace negotiations. Current MBS prices are only 1 tick below the previous intraday low, suggesting a technical support level, though another wave of geopolitical headlines could trigger negative reprices. That said, bonds coped with today’s uncertainty in a relatively calm fashion overall, indicating some resilience despite headline swings.

\n\n

Today’s Events

ADP Employment Change Weekly: 54.75K vs forecast N/A, prior 39K

Retail Sales (Mar): 1.7% vs 1.4% forecast, 0.6% prior

Retail Sales Control Group MoM (Mar): 0.7% vs 0.2% forecast, 0.5% prior

Pending Home Sales (Mar): 1.5% vs 0.1% forecast, 1.8% prior

\n\n

Bond Pricing

UMBS 30 yr

| Coupon | Price | Intra-Day Change |

GNMA 30 yr

| Coupon | Price | Intra-Day Change |

Treasuries

| Term | Yield | Price | Intra-Day Yield Change |