WTMS Blog Today = What’s up in Mortgage Today (AM) – 04/16/2026

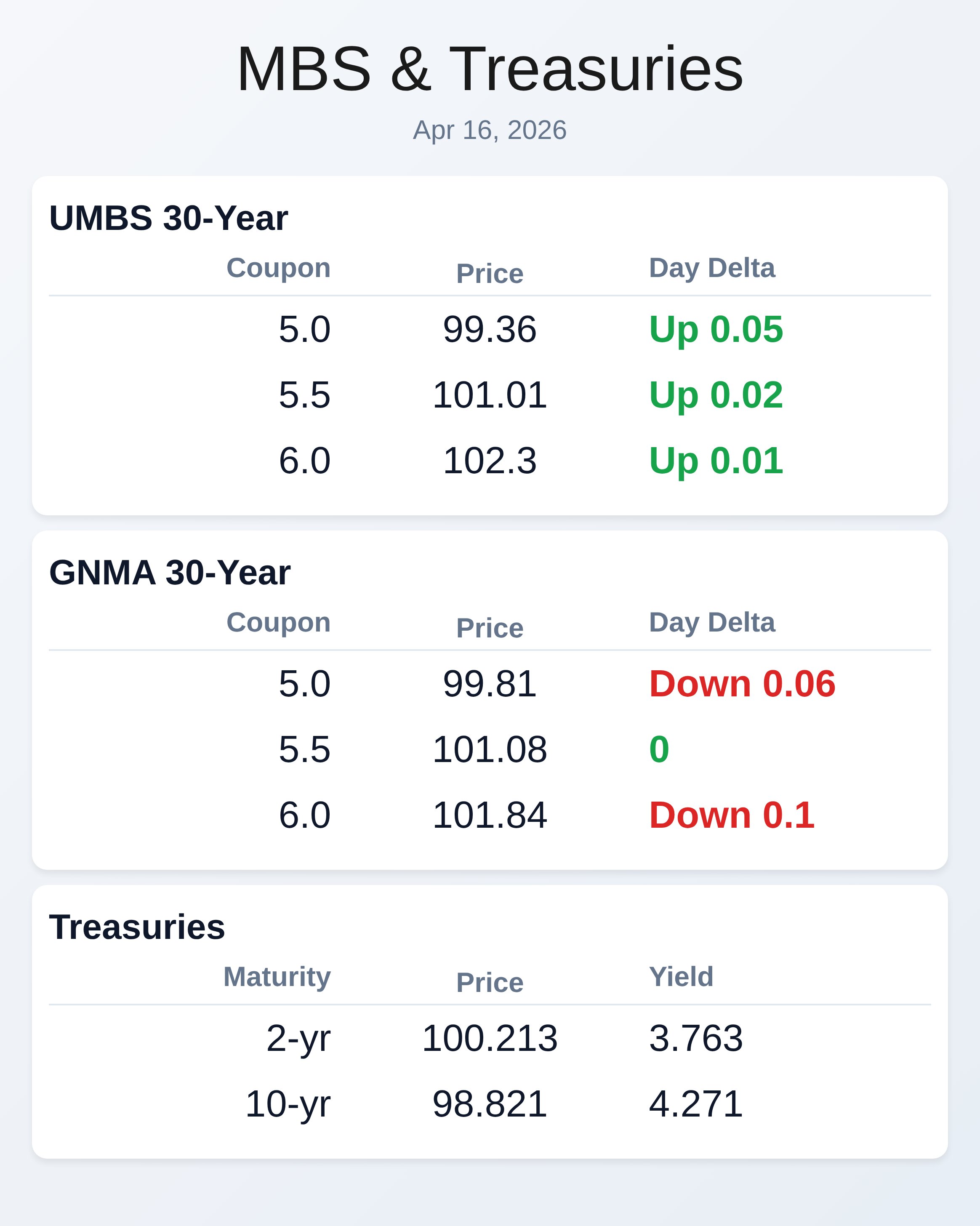

Markets are sideways and traders are waiting for the ceasefire to tell them what bonds should do. Today began quietly with the slowest trading activity since February 24th, before the Iran war escalated tensions and forced investors into a defensive holding pattern. UMBS 5.0 sits at 99.38, up 8 basis points from the previous close, while the 10-year Treasury yield has drifted lower to 4.27%, offering mild relief for originators pricing new loans.

The message from market participants is clear: without either a permanent peace deal or a sharp deterioration in the Middle East, volatility will remain subdued and bonds are unlikely to spark meaningful momentum. Economic data released today proved that even solid numbers can be ignored when geopolitical uncertainty dominates investor psychology. Jobless claims fell to 207,000 versus the 215,000 forecast, while the Philadelphia Fed Business Index surprised to the upside at 26.7 compared to a 10 expectation, marking genuine strength in manufacturing sentiment.

Yet neither report triggered a rush into Treasury positions, leaving MBS prices virtually flat and keeping rate-sensitive borrowers in a holding pattern. The Federal Reserve’s Beige Book reinforced the cautious environment, noting that businesses remain hesitant to hire, invest, or adjust pricing until Middle East tensions clarify. For loan officers managing borrower locks, this stasis is both a relief and a curse: stability beats volatility, but the lack of conviction buying suggests originators should brace for continued margin compression if cash window executions remain the dominant secondary market activity.

GNMA securities experienced mixed intraday action, with the 5.0 coupon down 6 basis points while higher coupons held steadier, signaling that traders are rotating away from lower-coupon FHA and VA pools in favor of more defensive positioning. This divergence matters because Government National Mortgage Association pricing typically leads when risk-off sentiment takes hold, yet today’s pattern suggests investors are simply rotating rather than fleeing. The 5.5 coupon GNMA held flat at 101.08, and the 6.0 remained stable, indicating that servicers and portfolio managers are comfortable with their holdings as long as the ceasefire holds.

If tensions escalate again or another Middle East headline breaks, expect fresh selling pressure on lower coupons as traders seek to reduce exposure quickly. Builder confidence hit another speed bump with the NAHB index falling to 34 from a forecast of 37, extending the slide from 38 the prior month and confirming that the housing market remains hamstrung by mortgage rates stuck above 6%. This weakness directly affects mortgage origination volume because builders are the engines of purchase business, and softer construction confidence signals softer demand for new mortgages in the pipeline.

Although March import prices came in much cooler than expected at 0.8% month-over-month versus a 2% forecast, the disinflationary signal has not translated into rate relief for borrowers. Originators should interpret this data as a reminder that rate cuts depend on consistent, broad-based evidence of cooling inflation and slowing economic growth—neither of which is guaranteed as long as energy prices remain elevated and labor markets retain their resilience. New York Fed President Williams expressed concern that the Middle East war could slow U.S.

growth and worsen inflation, a view echoed by International Monetary Fund and World Bank delegates who argue markets are underestimating the war’s economic damage. His comments carry weight because rate expectations hinge partly on the Fed’s assessment of growth and inflation risks, and a growth slowdown coupled with sticky inflation creates the stagflationary scenario mortgage market watchers fear most. The stock market’s record highs, driven by artificial intelligence enthusiasm and strong technology earnings, stand in sharp contrast to the caution pervading fixed-income markets.

This divergence is unsustainable long-term; if equities finally acknowledge the war’s economic headwinds, Treasury yields could spike sharply, forcing mortgage rates higher and creating havoc for borrowers who float their rate locks in the hopes of better terms. Ginnie Mae’s mortgage-backed securities portfolio grew to $2.91 trillion as of March 2026, with total issuance of $46.1 billion driving net portfolio growth of $4.16 billion in the month. The agency facilitated pooling and securitization of over 150,000 loans year-to-date and more than 128,000 households in March alone, underscoring the steady demand for FHA and VA financing despite higher rates.

However, traders note that Ginnie Mae 6.5% MBS is becoming expensive and difficult to buy back, creating unusual pricing dynamics that favor lenders who originated those loans earlier when rates were lower. For mortgage originators, this signals that while government-backed lending remains robust, the competitive landscape is shifting toward lenders with lower cost-of-funds and greater flexibility in their servicing operations. Maintain disciplined lock management and aggressive hedging until the geopolitical picture clarifies and bond markets find conviction again.

Locking vs Floating

Economic data is light and does not carry the force needed to drive meaningful bond market moves by itself. War headlines would need to be considerably more dramatic than current developments to shake markets from their current sideways drift. Most importantly, with the ceasefire holding and oil prices unpredictable, the market is simply kicking decisions down the road until clarity emerges on Middle East resolution.

Lenders should favor slightly defensive lock positioning over the next few days, as the pattern of winning streaks limited to two days suggests volatility could return without warning once geopolitical confidence shifts.

Today’s Events

Jobless Claims (Apr/11): 207.0K vs 215K forecast, 219K prior

Continued Claims (Apr/04): 1818.0K vs 1810K forecast, 1794K prior

Philadelphia Fed Business Index (Apr): 26.7 vs 10 forecast, 18.1 prior

Philadelphia Fed Prices Paid (Apr): 59.30 vs no forecast, 44.70 prior

March Industrial Production: 0.1% forecast, 0.2% prior (result: -0.5%)

NY Fed Manufacturing (Apr): 11.00 result vs -0.5 forecast, -0.20 prior

NAHB Builder Confidence: 34 result vs 37 forecast, 38 prior

March Import Prices (month-over-month): 0.8% result vs 2% forecast, 1.3% prior

Bond Pricing

UMBS 30 yr

| Coupon | Price | Intra-Day Change |

| 5.0 | 99.81 | -0.06 |

| 5.5 | 101.08 | 0.00 |

| 6.0 | 101.84 | -0.10 |

GNMA 30 yr

| Coupon | Price | Intra-Day Change |

Treasuries

| Term | Yield | Price | Intra-Day Yield Change |