WTMS Blog Today = What’s up in Mortgage Today (AM) – 04/17/2026

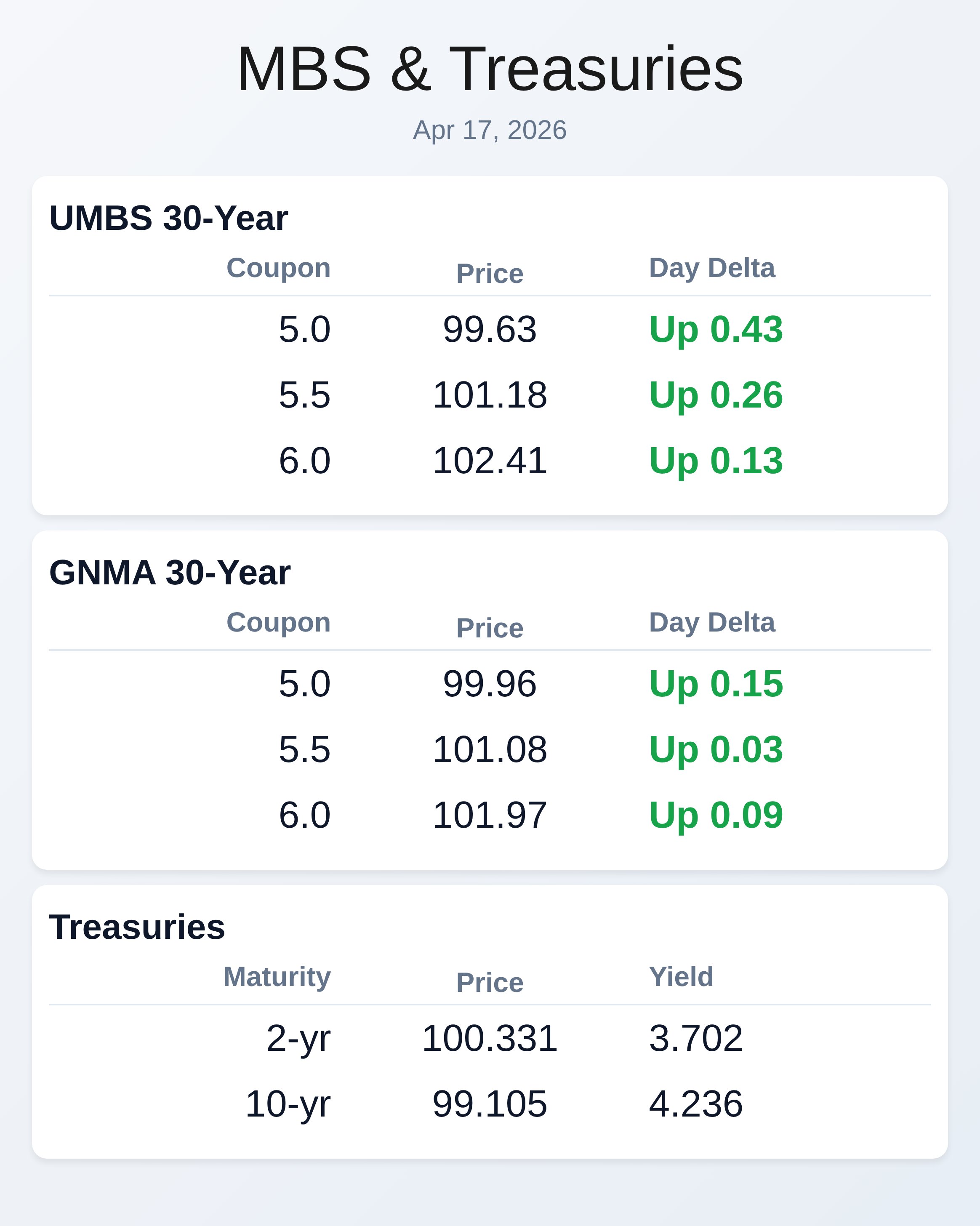

Middle Eastern ceasefire optimism is driving bond prices sharply higher this Friday morning, with UMBS 5.0 rallying 37 basis points and the 10-year Treasury yielding 4.237% as geopolitical tensions ease.

The rally accelerated at 8:41 a.m. EDT when Iran’s Foreign Minister announced a reopening of the Strait of Hormuz for the duration of a ceasefire, removing a major supply chain risk that had pressured energy and mortgage markets. Overnight reports of unfrozen Iranian assets and negotiations scheduled for Sunday in Islamabad—potentially with Trump’s personal attendance—compounded the flight-to-risk sentiment across global markets.

MBS prices are now the strongest performer today, reflecting bond market enthusiasm for lower rate expectations. For originators, this intraday volatility presents both immediate pricing opportunities and caution, as the broader downtrend since late March remains the dominant technical pattern. Equity markets are riding alongside the bond rally on war-de-escalation hopes and robust earnings season momentum.

The S&P 500 is on track for a third consecutive week of gains exceeding 3%, marking one of the fastest rallies from oversold to overbought territory in decades. Brent crude fell 3.3% toward $96 per barrel following Trump’s claim of key Iranian concessions, while the Bloomberg Dollar Index weakened toward February lows. Energy market relief translates indirectly to mortgage market relief, reducing inflation pressures that the Federal Reserve has cited as reasons to hold rates steady.

However, strategists warn that true durability depends on whether crude flows actually resume through Hormuz and whether consumer spending remains resilient amid higher year-to-date energy costs. Treasury yields across the curve declined sharply, with the 2-year falling to 3.704% (-7.3 basis points) and the 10-year reaching 4.235% (-7.8 basis points) by mid-morning. The 30-year Treasury yielded 4.876%, reflecting a 5.8 basis point decline from Thursday’s close.

This steepening of the long end demonstrates classic risk-off positioning and suggests market participants are pricing in durability to ceasefire hopes. The morning’s economic data included a better-than-forecast jobless claims print at 207K versus 215K expected, which added confidence to the labor market narrative without derailing bond strength. Importantly, volatility remains light this week, which increases lock-and-float optionality for originators even as geopolitical headlines remain unpredictable.

Housing market conditions continue deteriorating beneath the surface of stronger equity and bond rallies. Existing home sales fell to their slowest first-quarter pace since 2009, driven by a severe shortage of inventory and buyers locked into historically low mortgage rates. Builder sentiment remains deeply negative across most regions, particularly the West and South, while affordability continues to stretch despite the morning’s modest mortgage rate relief.

Rising mortgage rates following the earlier U.S.–Iran conflict pushed marginal buyers to the sidelines and contributed to what Chrisman Commentary described as the “weakest start to a year for home sales since 2009.” New home sales remain relatively resilient due to pricing flexibility, but consumer sentiment deterioration poses increasing risk to the origination pipeline. Chicago Federal Reserve President Austan Goolsbee has warned of a “double danger” to inflation control from the Iran conflict and Trump’s tariffs, urging the central bank to delay rate cuts until inflation stabilizes. Current market expectations have shifted toward prolonged Fed inaction with anticipated cuts pushed out to 2027, a stark reversal from earlier 2026 optimism.

Treasury markets remain range-bound amid balanced geopolitical and inflation risks, while debates about Fed balance sheet reduction are expected to surface in upcoming leadership discussions. The political dimension added complexity yesterday when President Trump vowed to fire Federal Reserve Chair Jerome Powell if he does not voluntarily resign when his term ends next month, though Powell could remain as a governor until 2028. For mortgage originators, extended rate stability combined with housing demand weakness creates a challenging volume environment heading into summer.

Servicing rights have gained renewed market attention, with mortgage servicing rights (MSR) trading multiples rising to the mid-5x range for certain cohorts, up significantly from the 4×1 levels that persisted for years. This increase reflects stronger confidence in borrower retention and servicing execution, despite the strained housing market backdrop. Originators and portfolio managers are actively buying and selling servicing portfolios, understanding that lock-in values on borrower relationships justify higher prices in today’s environment.

The combination of higher MSR valuations and tighter origination margins is prompting industry consolidation and strategic partnerships. Friday’s bond rally provides short-term relief but does not fundamentally alter the structural challenges facing housing demand or the necessity for efficiency-focused business models in mortgage origination. ## Locking vs Floating

Locking vs Floating

Volatility has remained light since Tuesday, creating expanded optionality for borrowers deciding between locked and floating rate positions.

The pending two-week ceasefire deadline approaching in early May introduces uncertainty that does not adhere to scheduled economic report releases, meaning volatility could spike with minimal warning. Today’s rally demonstrates that MBS price action is the best real-time risk indicator for intraday decisions, while tracking 10-year yield ceiling and floor levels helps assess broader bond market momentum. Originators should maintain elevated rate-lock discipline given geopolitical tail risks, even as short-term technicals appear favorable following this morning’s rally.

## Today’s Events

Today’s Events

No scheduled economic data releases are on today’s calendar. Market activity will be driven by remarks from Federal Reserve speakers: San Francisco President Mary Daly, Richmond Fed President Thomas Barkin, and Governor Christopher Waller. The Treasury Department will conduct an auction of 5-year TIPS (Treasury Inflation-Protected Securities), which will test investor demand for inflation-protected instruments at current yield levels.

## Bond Pricing

Bond Pricing

UMBS 30 yr

| Coupon | Price | Intra-Day Change |

GNMA 30 yr

| Coupon | Price | Intra-Day Change |

Treasuries

| Term | Yield | Price | Intra-Day Yield Change |

| 2yr | 3.704 | 100.327 | -0.073 |

| 3yr | 3.717 | 99.389 | -0.088 |

| 5yr | 3.831 | 100.199 | -0.090 |

| 7yr | 4.020 | 101.394 | -0.084 |

| 10yr | 4.235 | 99.109 | -0.078 |

| 30yr | 4.876 | 98.025 | -0.058 |