**WTMS Blog Today = What’s up in Mortgage Today (PM) – 06/01/2026**

Warren Buffett’s $6.8 billion bet on Taylor Morrison signals that savvy investors still see housing upside despite affordability headwinds and tight inventory. The deal marks Berkshire Hathaway’s first major acquisition under CEO Greg Abel, who plans to merge Taylor Morrison with Clayton Homes into a vertically integrated platform. With a combined mortgage origination operation approaching $4 billion annually plus title and insurance operations, Berkshire is positioning itself to capture customers across multiple stages of the homeownership journey.

This move demonstrates that long-term investors are thinking in years, not weeks, about housing demand fundamentals. For independent loan officers, the takeaway is clear: builders controlling customer relationships and mortgage companies present mounting competition for retail originations. Meanwhile, Canadian banks are making strategic moves into U.S.

mortgage warehouse lending just as domestic players retreat. Scotiabank acquired MapleMark Bank in Dallas to gain FDIC deposit insurance credentials—a critical requirement for attracting independent mortgage bankers to its warehouse platform. The timing capitalizes on recent exits by Flagstar and Comerica, leaving supply-side gaps for new entrants.

This cross-border consolidation reflects broader capital markets confidence in mortgage lending infrastructure despite near-term rate uncertainty. Warehouse lenders remain essential infrastructure for the independent channel’s survival. Credit scoring continues its slow transformation as Rocket Mortgage pulls both FICO and VantageScore 4.0 simultaneously across Fannie Mae, Freddie Mac, and VA products.

Running dual scores in tandem gives borrowers the broadest qualification opportunity during this pilot phase, though industry consensus on a single standard remains distant. TransUnion’s CEO indicated that widespread adoption with the GSEs likely won’t materialize until 2027, despite “tremendous economic incentive” to move faster. The broader shift acknowledges that alternative scores can capture creditworthy borrowers traditional FICO might miss.

Originators should prepare for years of score complexity before clarity emerges. Property tax increases hit every major U.S. metro in 2024, with mortgaged homeowners bearing disproportionate burden through escrow.

National median property tax bills climbed 5.1% to $3,119, while borrowers with mortgages paid a median $3,489 annually—a $913 gap versus owners free and clear. Tampa, Denver, and Miami led increases above 7%, while New York City’s bills exceeded $10,000. These rising escrow obligations directly inflate monthly housing payments and compress buyer purchasing power.

Loan officers should factor compounding tax increases into debt-to-income calculations and affordability discussions with clients. Bond markets digested mixed economic signals Monday with 10-year Treasury yields ending 2.8 basis points higher at 4.464%. Construction spending came in hotter than forecast at 0.4%, while ISM manufacturing employment deteriorated to 48.6 and pricing pressure eased with the ISM Prices Paid index falling to 82.1.

The trading pattern remained tethered to Iran war developments, with yields spiking on escalation headlines and recovering on de-escalation news. Uncertainty around geopolitical outcomes means overnight lock-float decisions remain essentially coin flips. Mortgage professionals should position clients based on long-term conviction rather than headline whiplash.

**Locking vs Floating**

Overnight lock-float decisions are essentially 50-50 coin flips given the unpredictable war news cycle. Geopolitical uncertainty will likely persist through early June until concrete peace developments emerge. When peace is actually achieved, bonds should respond favorably and rates should improve.

For now, clients with flexible timelines should hold rather than lock, but those with imminent closing dates should lock to eliminate execution risk.

**Today’s Events**

Construction Spending (Apr): 0.4% vs. 0.2% forecast, 0.6% previous

ISM Manufacturing Employment (May): 48.6 vs.

— forecast, 46.4 previous

ISM Manufacturing PMI (May): 54.0 vs. 53 forecast, 52.7 previous

ISM Mfg Prices Paid (May): 82.1 vs. 85.5 forecast, 84.6 previous

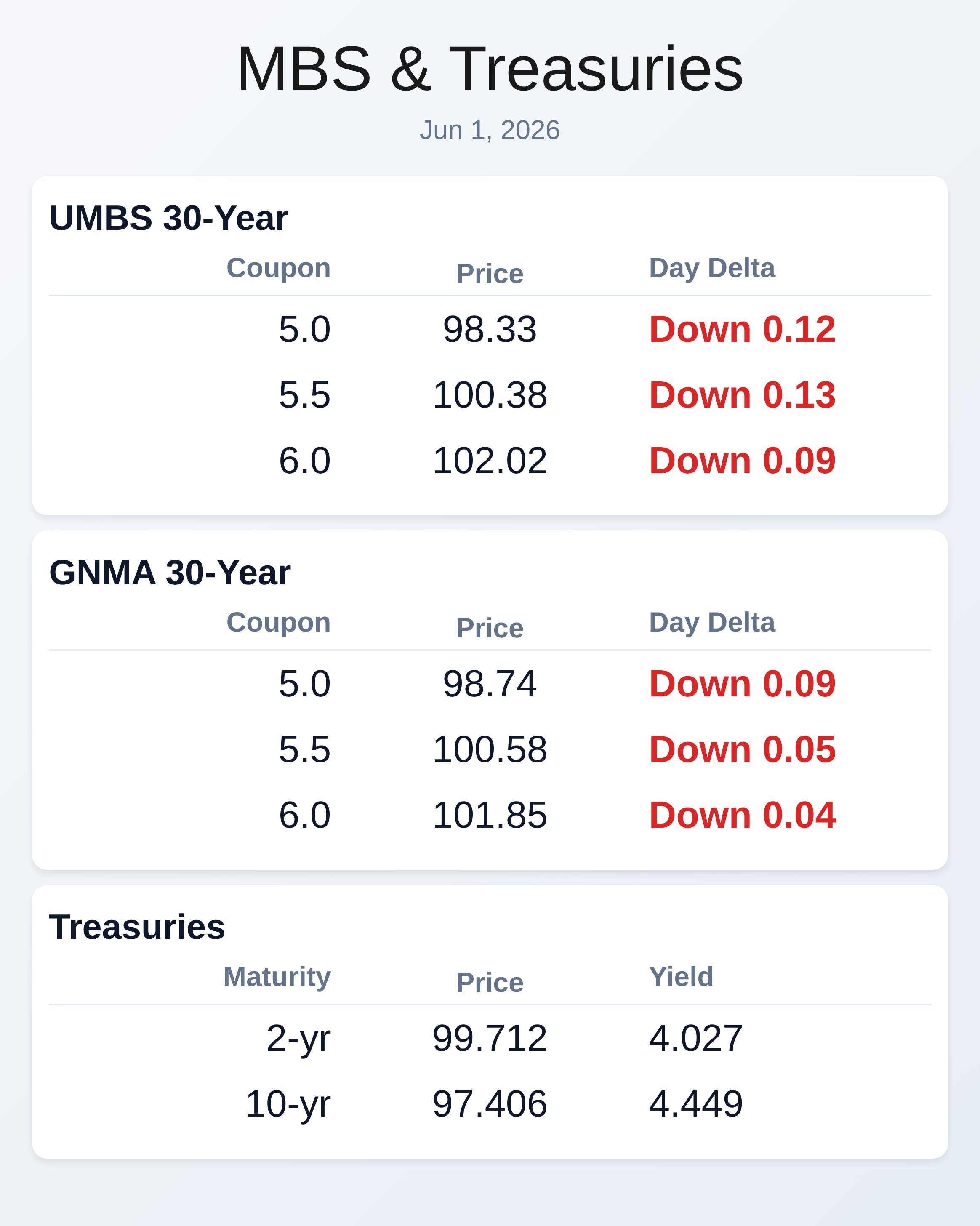

**Bond Pricing**

**UMBS 30 yr**

| Coupon | Price | Intra-Day Change |

| 5.0 | 98.25 | -0.20 |

| 5.5 | 100.34 | -0.16 |

| 6.0 | 102.02 | -0.09 |

**GNMA 30 yr**

| Coupon | Price | Intra-Day Change |

| 5.0 | 98.67 | -0.16 |

| 5.5 | 100.58 | -0.05 |

| 6.0 | 101.85 | -0.04 |

**Treasuries**

| Term | Yield | Price | Intra-Day Yield Change |