“Damn, there is so much great knowledge out there. Did you know that “BOOKS” are full of smart?? No, I mean like life changing, I-wish-I-knew-that-years-ago type stuff.

I know that I was waaaayyy late to the game figuring it out. And I know that a lot of you are too busy to read as much as you ‘should’. And that is why you need me.

I still remember how it started for me. It started in June of 2008. After 11 years …..Click to continue

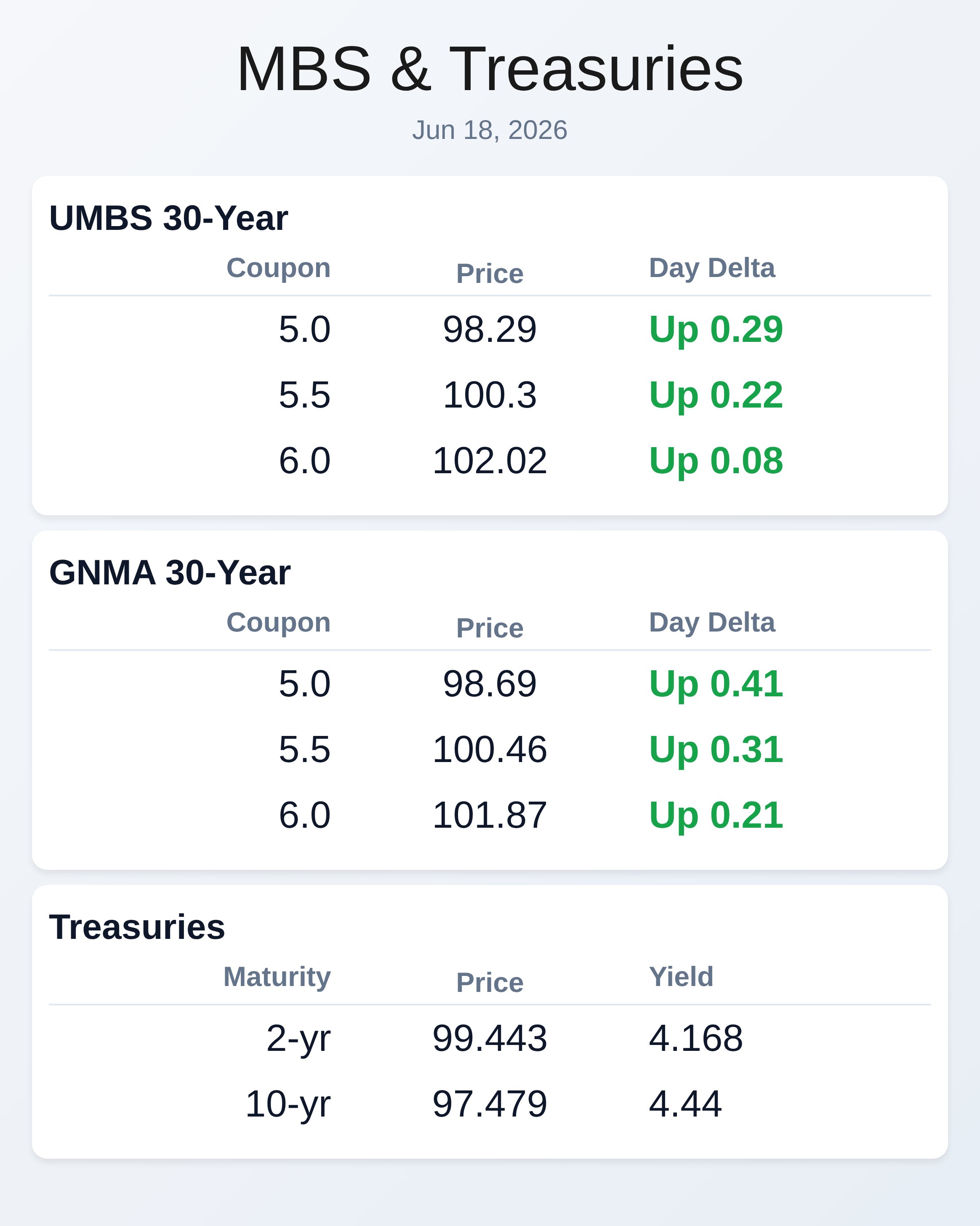

June 18, 2026

June 18, 2026

The Real Reason You Can't Scale Your Real Estate Business (Hint: It's Not About Working Harder)

Alex Hormozi's framework for why most agents hit an income ceiling and how to actually break through it

Blog post

The Three Scaling Constraints Nobody Talks About

Hormozi identifies three primary constraints that prevent businesses from scaling: time, energy, and attention. You have limited time—twenty-four hours per day, same as everyone else. You have limited energy—you can only personally do so much before burning out. You have limited attention—you can only focus on so many things at once before quality suffers. Every business that fails to scale is hitting one or more of these constraints. For real estate professionals, time constraint shows up when you're personally involved in every showing, every negotiation, every transaction detail. There are only so many hours available, which means there's a hard ceiling on how many deals you can personally close. Energy constraint shows up when you're working sixty-hour weeks and can't maintain that pace without burning out. Attention constraint shows up when you're trying to manage leads, current clients, marketing, and administration simultaneously and everything suffers. Most agents try to scale by working harder—more hours, more hustle, more personal effort. This temporarily increases output but inevitably hits one of the three constraints. You run out of time, energy, or attention, and growth stops. Hormozi's solution: remove yourself as the constraint by building systems and teams that don't require your personal time, energy, or attention to execute. This requires a fundamental mindset shift from "I need to do more" to "I need to build systems that do more without me." For most real estate professionals, this is terrifying because their entire identity is wrapped up in being personally excellent. Hormozi would say your personal excellence should be in building systems, not in executing transactions. The latter has a ceiling, the former doesn't.The Delegation Disaster Most Agents Create

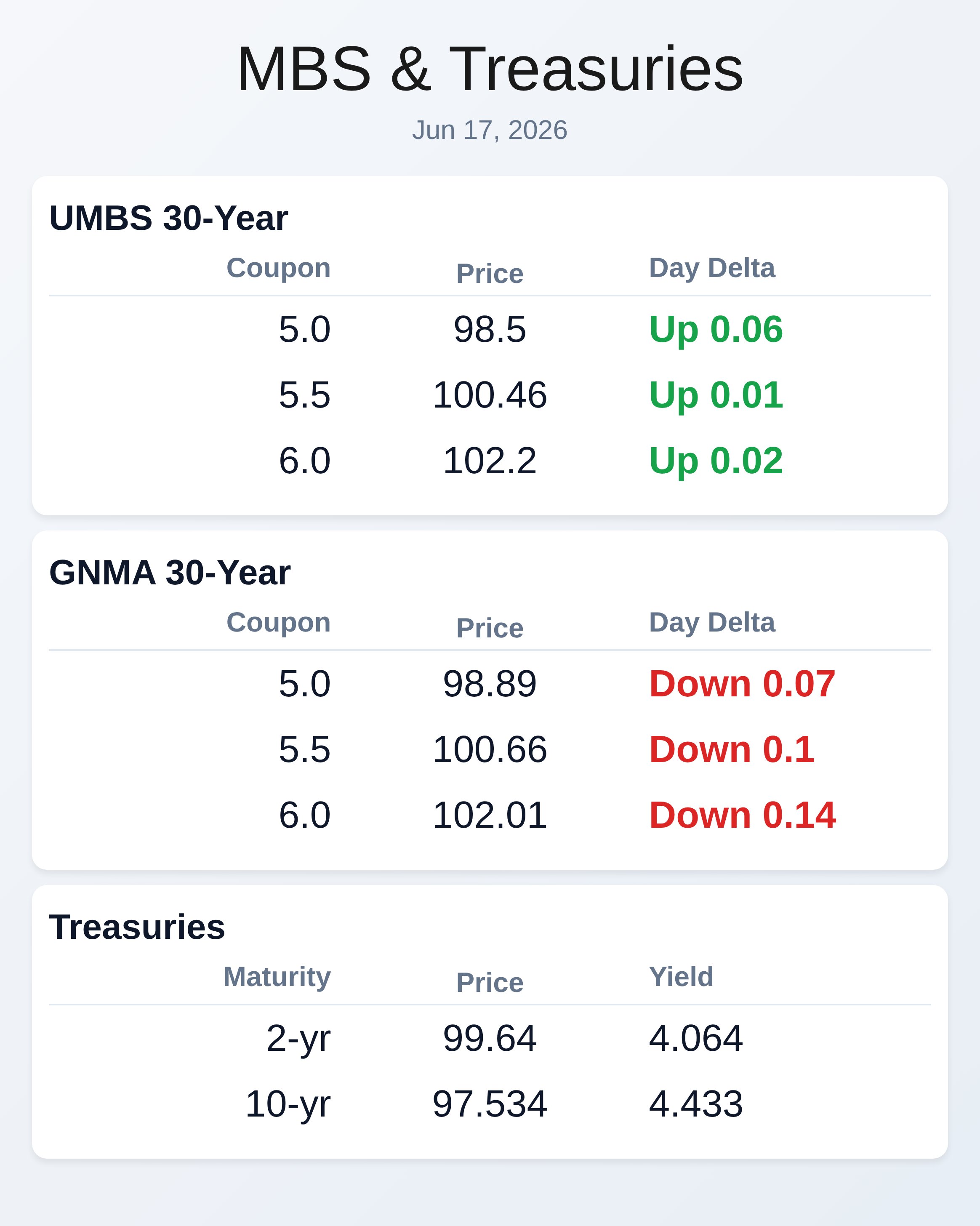

When real estate professionals finally decide to scale, they usually hire an assistant or buyer's agent and immediately screw it up. They delegate tasks without delegating authority, they micromanage every detail, they step in whenever something isn't perfect, and they wonder why their team can't execute without them. Hormozi would say they're delegating wrong, which is almost worse than not delegating at all. Real delegation means transferring both responsibility and authority. It means creating systems so clear that someone else can execute them without constantly asking for your input. It means accepting that they'll do things differently than you would and that's okay as long as results are achieved. It means building accountability systems rather than supervision systems. For listing agents, this might mean creating a complete listing presentation system that a team member can execute—scripts, materials, pricing analysis templates, marketing plans—everything documented so thoroughly that youJune 17, 2026

RECENT ARTICLES

The “Phantom” Paychecks: Why Wall Street Thinks the 2026 Jobs Boom is a Statistical Illusion

In early 2026, the financial world is witnessing a surreal disconnect. While the S&P 500 reaches new heights, a growing chorus of Wall Street analysts and economists is sounding the alarm: the "strong" jobs data [...]

Mortgage Today (AM) – 02/23/26

WTMS Blog Today = What's up in Mortgage Today (AM) - 02/23/2026 Markets woke up to a tariff ruling that briefly rattled traders but ultimately failed to derail the bond rally. Despite headline noise about [...]

Mortgage Today (PM) – 02/20/26

WTMS Blog Today = What's up in Mortgage Today (PM) - 02/20/2026 Mortgage markets close the week with a dramatic split narrative as economic data delivers both inflationary heat and economic cooling. Core PCE inflation [...]

Article Archive

What’s up in Mortgage Today (AM) – 08/20/2025

WTMS Blog Today = What's up in Mortgage Today (AM) - 08/20/2025 Mortgage Backed Securities markets are showing relative stability this morning, with UMBS prices holding fairly steady ahead of key economic data releases [...]

Mortgage Today (PM) 08/19/2025

Mortgage Today (PM) 08/19/2025 The mortgage-backed securities market experienced notable pressure today as MBS prices declined across the yield curve, with the benchmark UMBS 5.5% coupon losing approximately 6-8 basis points intraday. This weakness stemmed [...]

What’s up in Mortgage Today (AM) – 08/19/2025

**WTMS Blog Today = What's up in Mortgage Today (AM) - 08/19/2025** Mortgage-backed securities are showing mixed signals this morning as the 10-year Treasury yield hovers around 4.34%, roughly unchanged from Friday's close. Bond prices [...]

What’s up in Mortgage Today (AM) – 8/15/25

**WTMS Blog Today = What's up in Mortgage Today (AM) - 8/15/25** Mortgage-backed securities are experiencing modest volatility this morning as markets digest recent economic data and Fed policy expectations. The UMBS market is showing [...]

What’s up in Mortgage Today (AM) – 08/12/2025

**WTMS Blog Today = What's up in Mortgage Today (AM) - 08/12/2025** Mortgage backed securities are facing continued pressure this morning as investors remain cautious ahead of key economic data releases. The 10-year Treasury [...]

What’s up in Mortgage Today (AM) – 08/11/2025

**WTMS Blog Today = What's up in Mortgage Today (AM) - 08/11/2025** The bond market is experiencing mixed signals this morning as traders digest the latest economic data and Federal Reserve commentary. Mortgage-backed securities (MBS) [...]

What’s up in Mortgage Today (AM) – 8/8/2025

**WTMS Blog Today = What's up in Mortgage Today (AM) - 8/8/2025** The mortgage-backed securities market is experiencing continued pressure as bond prices face headwinds following recent Federal Reserve actions and evolving economic data. [...]

WTMS Blog Today = What’s up in Mortgage Today (AM) – 8/7/2025

**WTMS Blog Today = What's up in Mortgage Today (AM) - 8/7/2025** The mortgage-backed securities market is showing mixed signals this Monday morning as traders digest recent Federal Reserve communications and prepare for this [...]