“Damn, there is so much great knowledge out there. Did you know that “BOOKS” are full of smart?? No, I mean like life changing, I-wish-I-knew-that-years-ago type stuff.

I know that I was waaaayyy late to the game figuring it out. And I know that a lot of you are too busy to read as much as you ‘should’. And that is why you need me.

I still remember how it started for me. It started in June of 2008. After 11 years …..Click to continue

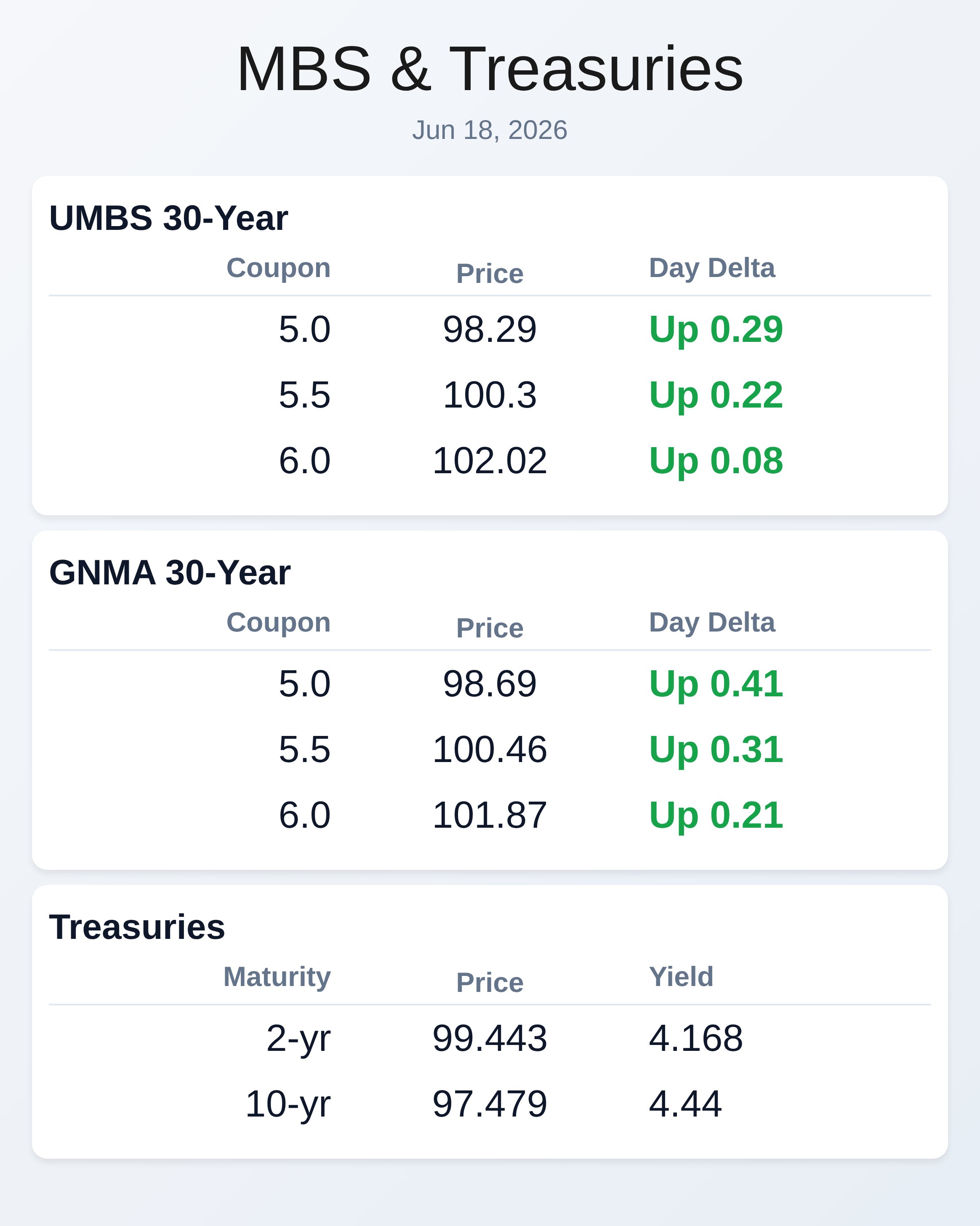

June 18, 2026

June 18, 2026

The Real Reason You Can't Scale Your Real Estate Business (Hint: It's Not About Working Harder)

Alex Hormozi's framework for why most agents hit an income ceiling and how to actually break through it

Blog post

The Three Scaling Constraints Nobody Talks About

Hormozi identifies three primary constraints that prevent businesses from scaling: time, energy, and attention. You have limited time—twenty-four hours per day, same as everyone else. You have limited energy—you can only personally do so much before burning out. You have limited attention—you can only focus on so many things at once before quality suffers. Every business that fails to scale is hitting one or more of these constraints. For real estate professionals, time constraint shows up when you're personally involved in every showing, every negotiation, every transaction detail. There are only so many hours available, which means there's a hard ceiling on how many deals you can personally close. Energy constraint shows up when you're working sixty-hour weeks and can't maintain that pace without burning out. Attention constraint shows up when you're trying to manage leads, current clients, marketing, and administration simultaneously and everything suffers. Most agents try to scale by working harder—more hours, more hustle, more personal effort. This temporarily increases output but inevitably hits one of the three constraints. You run out of time, energy, or attention, and growth stops. Hormozi's solution: remove yourself as the constraint by building systems and teams that don't require your personal time, energy, or attention to execute. This requires a fundamental mindset shift from "I need to do more" to "I need to build systems that do more without me." For most real estate professionals, this is terrifying because their entire identity is wrapped up in being personally excellent. Hormozi would say your personal excellence should be in building systems, not in executing transactions. The latter has a ceiling, the former doesn't.The Delegation Disaster Most Agents Create

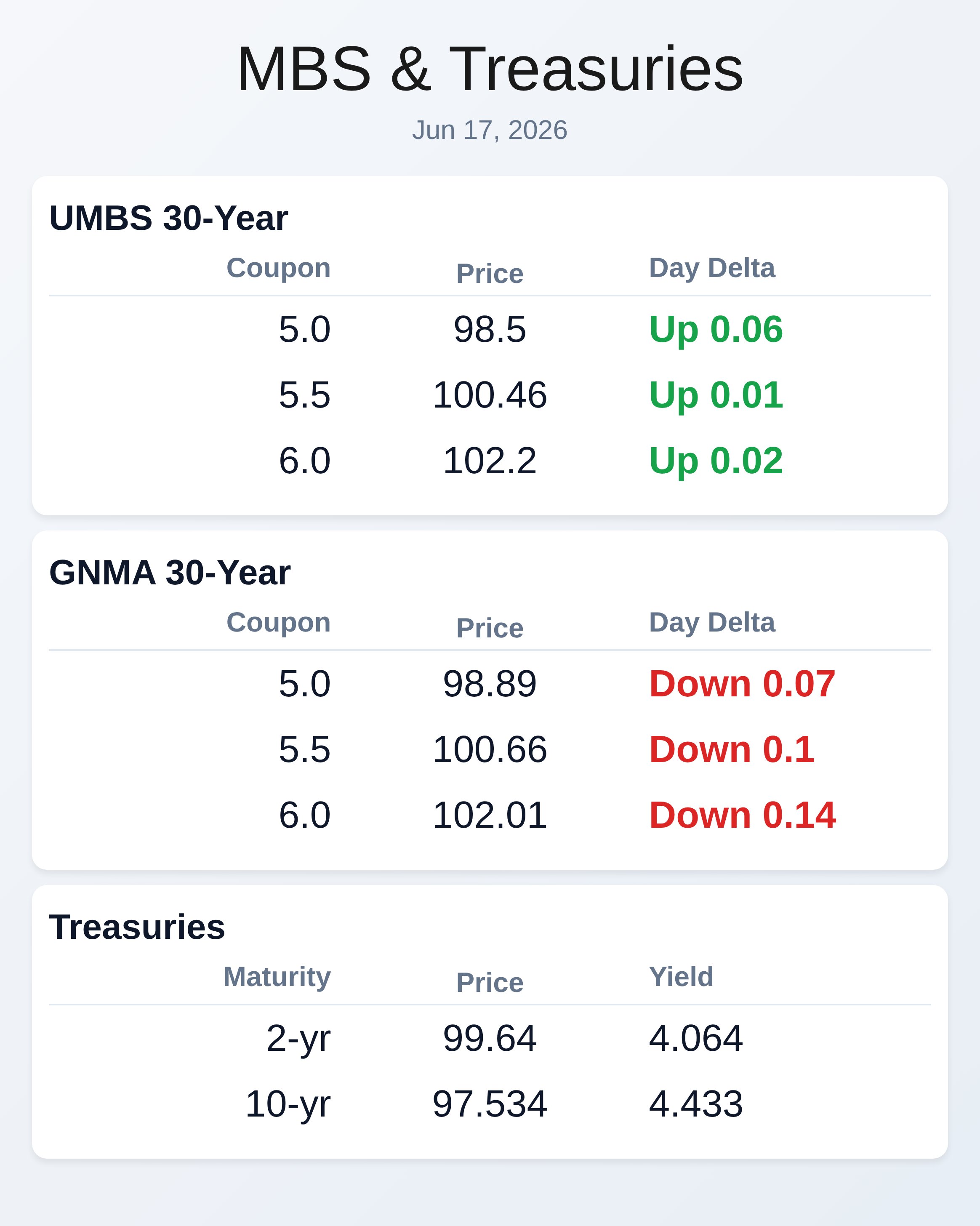

When real estate professionals finally decide to scale, they usually hire an assistant or buyer's agent and immediately screw it up. They delegate tasks without delegating authority, they micromanage every detail, they step in whenever something isn't perfect, and they wonder why their team can't execute without them. Hormozi would say they're delegating wrong, which is almost worse than not delegating at all. Real delegation means transferring both responsibility and authority. It means creating systems so clear that someone else can execute them without constantly asking for your input. It means accepting that they'll do things differently than you would and that's okay as long as results are achieved. It means building accountability systems rather than supervision systems. For listing agents, this might mean creating a complete listing presentation system that a team member can execute—scripts, materials, pricing analysis templates, marketing plans—everything documented so thoroughly that youJune 17, 2026

RECENT ARTICLES

Warren Buffett’s Company Just Dropped a Major Hint About the Housing Market — Here’s What It Means for You

Warren Buffett's Company Just Dropped a Major Hint About the Housing Market — Here's What It Means for You The Oracle of Omaha's real estate arm sees a turning point coming. Should you pay attention? [...]

Mortgage Today (AM) – 01/12/26

WTMS Blog Today = What's up in Mortgage Today (AM) - 01/12/2026 Markets are under pressure this morning as the Department of Justice escalated its attack on Fed independence with criminal investigation threats. Fed Chair [...]

What’s up in Mortgage Today (AM) – 01/09/2026

WTMS Blog Today = What's up in Mortgage Today (AM) - 01/09/2026 MBS markets exploded higher this morning after Trump announced his plan to buy $200 billion in mortgage bonds. The president instructed Fannie Mae [...]

Article Archive

Mortgage Today 07/19/24: UMBS Down, Bond Rally Hits Wall, Microsoft Outage Impacts Financial Systems

Friday - July 19, 2024 UMBS opened down 11 bps in the first hour of trading. Stocks futures are up 6.75 This week's bond rally hit a wall at the 3pm close on [...]

Mortgage Today 07/18/24: UMBS Open Up 4 bps, Jobless Claims Rise, Rate Cuts Anticipated

Thursday - July 18, 2024 UMBS were up 4 bps on the open. Small number but at least it's green. S&P Stock Futures are up 8.50 points. A mixed bag of data in [...]

Mortgage Today 07/17/24: UMBS Flat, S&P Futures Down 56 Points, Tech Stocks Hit by Trade Tensions

Wednesday - July 17, 2024 UMBS opened down 12 bps in the first hour of trading. S&P Futures down 56.25 Worries that US politicians are taking a harder stance on China and Taiwan [...]

Mortgage Today 07/15/24: UMBS Down 9 bps, S&P Futures Up 24 Points, Trump Speculation and Rate Cut Hints

UMBS started the week off down 9 bps. S&P futures are up 24 pts US stock futures rose and longer-maturity bonds retreated as investors ratcheted up wagers that Donald Trump would win the [...]

Mortgage Today 07/12/24: UMBS Up 20 bps, Surprising PPI Surge Raises Eyebrows, Rate Cut Still Expected

Friday - July 12, 2024 Happy Friday! UMBS are up 16 bps on the open. Stock Futures are Flat. Core PPI M/M = 0.4 vs 0.2 f'cast last month revised to 0.3 from [...]

Mortgage Today 07/11/24: UMBS Surge 41 bps on Lower CPI, S&P Futures Down 9.5 Points

Thursday - July 11, 2024 Oooooh-Weee. UMBS are up 41 bps on the open, so far. S&P futures down 9.5 points Headline CPI M/M = -0.1 vs 0.1% f'cast, [0.0 prev] Headline CPI [...]

Mortgage Today 07/10/24: UMBS Up 3 bps, S&P 500 Futures Rise 14.25 Points, Powell’s Testimony Highlights Inflation Caution

UMBS up 3 bps on the open. Stock futures up 14.25 points. Stock futures pointed to a longer advance for the S&P 500 as investors sought vindication from Federal Reserve Chair Jerome Powell [...]

Yeah But…. Too Many People are moving here!

WTMS Blog Today >>>> Yeah But.........Too Many People are moving here! In this world, there are no solutions - only trade-offs. And that is the case when your area gets a whole bunch [...]