“Damn, there is so much great knowledge out there. Did you know that “BOOKS” are full of smart?? No, I mean like life changing, I-wish-I-knew-that-years-ago type stuff.

I know that I was waaaayyy late to the game figuring it out. And I know that a lot of you are too busy to read as much as you ‘should’. And that is why you need me.

I still remember how it started for me. It started in June of 2008. After 11 years …..Click to continue

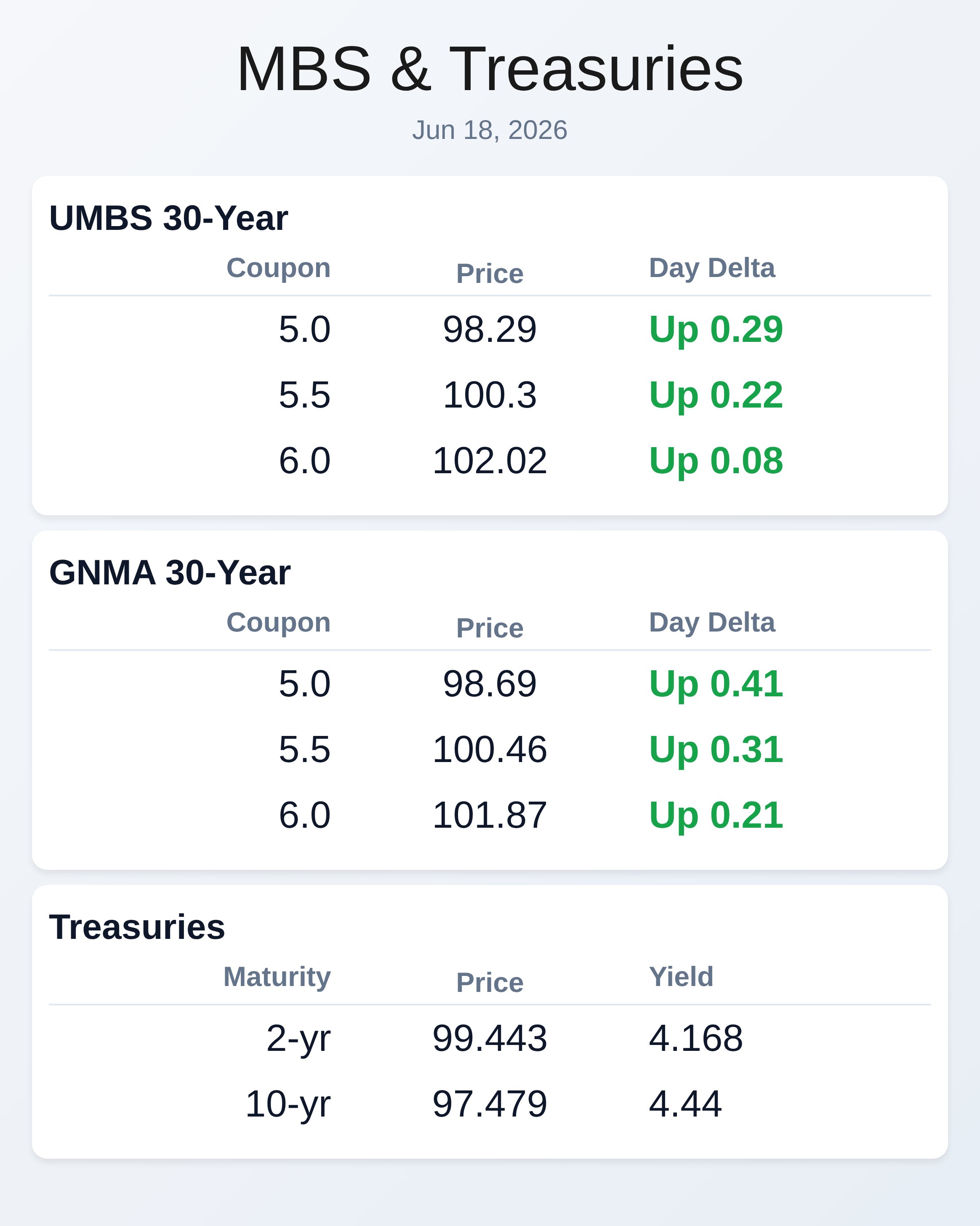

June 18, 2026

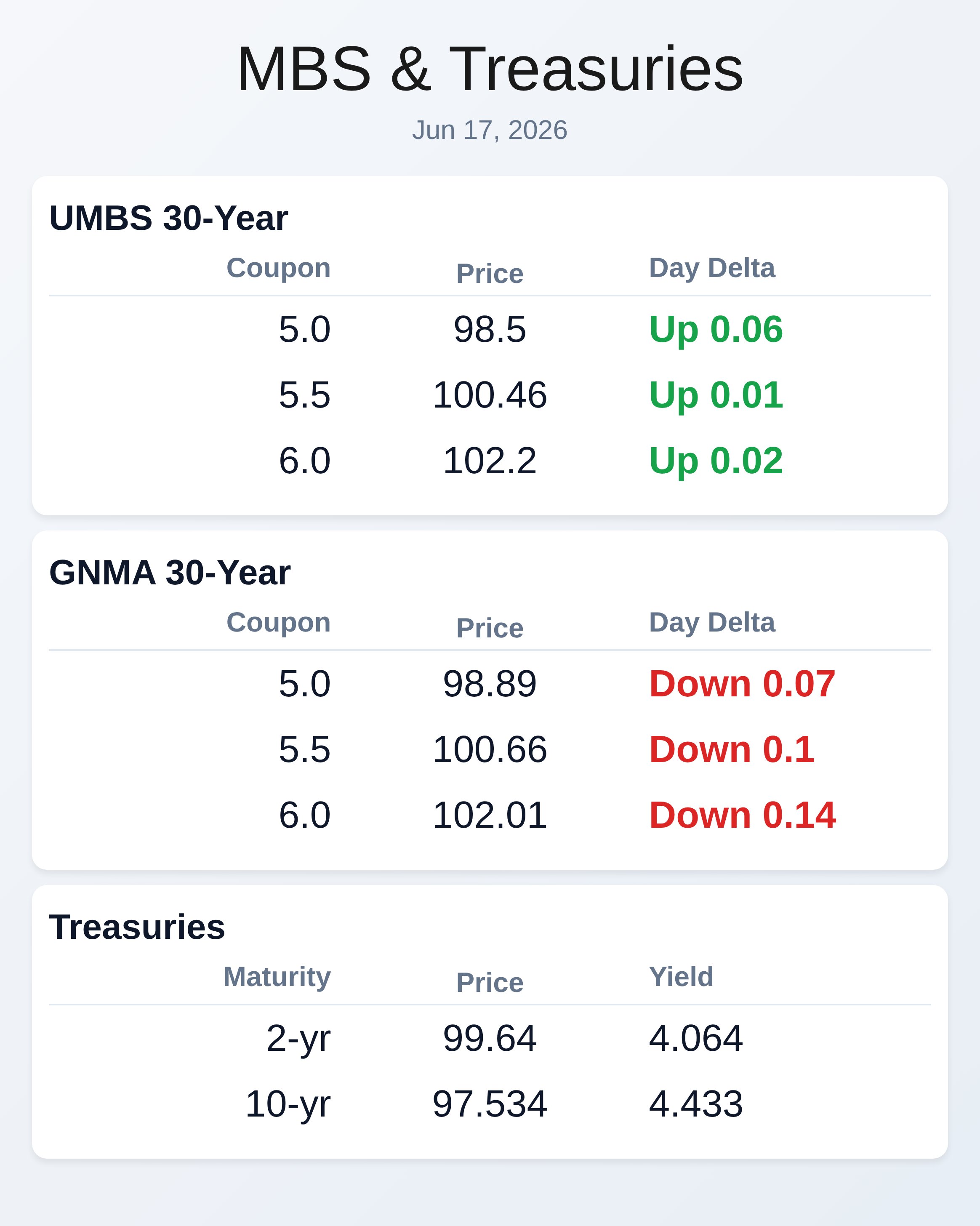

June 18, 2026

The Real Reason You Can't Scale Your Real Estate Business (Hint: It's Not About Working Harder)

Alex Hormozi's framework for why most agents hit an income ceiling and how to actually break through it

Blog post

The Three Scaling Constraints Nobody Talks About

Hormozi identifies three primary constraints that prevent businesses from scaling: time, energy, and attention. You have limited time—twenty-four hours per day, same as everyone else. You have limited energy—you can only personally do so much before burning out. You have limited attention—you can only focus on so many things at once before quality suffers. Every business that fails to scale is hitting one or more of these constraints. For real estate professionals, time constraint shows up when you're personally involved in every showing, every negotiation, every transaction detail. There are only so many hours available, which means there's a hard ceiling on how many deals you can personally close. Energy constraint shows up when you're working sixty-hour weeks and can't maintain that pace without burning out. Attention constraint shows up when you're trying to manage leads, current clients, marketing, and administration simultaneously and everything suffers. Most agents try to scale by working harder—more hours, more hustle, more personal effort. This temporarily increases output but inevitably hits one of the three constraints. You run out of time, energy, or attention, and growth stops. Hormozi's solution: remove yourself as the constraint by building systems and teams that don't require your personal time, energy, or attention to execute. This requires a fundamental mindset shift from "I need to do more" to "I need to build systems that do more without me." For most real estate professionals, this is terrifying because their entire identity is wrapped up in being personally excellent. Hormozi would say your personal excellence should be in building systems, not in executing transactions. The latter has a ceiling, the former doesn't.The Delegation Disaster Most Agents Create

When real estate professionals finally decide to scale, they usually hire an assistant or buyer's agent and immediately screw it up. They delegate tasks without delegating authority, they micromanage every detail, they step in whenever something isn't perfect, and they wonder why their team can't execute without them. Hormozi would say they're delegating wrong, which is almost worse than not delegating at all. Real delegation means transferring both responsibility and authority. It means creating systems so clear that someone else can execute them without constantly asking for your input. It means accepting that they'll do things differently than you would and that's okay as long as results are achieved. It means building accountability systems rather than supervision systems. For listing agents, this might mean creating a complete listing presentation system that a team member can execute—scripts, materials, pricing analysis templates, marketing plans—everything documented so thoroughly that youJune 17, 2026

RECENT ARTICLES

My Full Reading Notes for “Tools of Titans” by Tim Ferriss

Reading Notes For: 📍 My reading notes for Tools of Titans by Tim Ferriss. Tools of Titans by Tim Ferriss distills insights from hundreds of interviews with top performers [...]

What’s up in Mortgage Today (PM) – 12/17/2025

WTMS Blog Today = What's up in Mortgage Today (PM) - 12/17/2025 Mortgage bonds are testing investor patience as the 30-year UMBS 5.0 coupon dropped to 99.47, down 7 basis points from yesterday's close. The [...]

What’s up in Mortgage Today (AM) – 12/17/2025

WTMS Blog Today = What's up in Mortgage Today (AM) - 12/17/2025 Mortgage rates climbed higher again after last week's Fed rate cut, creating the paradoxical situation we've seen repeatedly this year. The 30-year UMBS [...]

Article Archive

Getting Things Done Explained – Part 3

???? My reading notes for getting things done - Part 3. GTD is now shorthand for an entire way of approaching professional and personal tasks, and has spawned an entire culture of organizational [...]

Mortgage Today 05/06/24: UMBS Slip Amid Fed Commentary and ISM Services Contraction

UMBS were up 3 bps, on the open. Stocks up 21.5 The week ahead is pretty data-light, although we will get a lot of Fed-speak. The main number will be consumer sentiment on [...]

Getting Things Done Explained – Part 2

???? My reading notes for getting things done - part 2. Creating relevant placeholding notes, for example, purge and process boat storage shed, and deal with hall closet. Reasons to gather everything before [...]

Mortgage Today 05/01/24: UMBS Gains 40bps as Market Digests Economic Data and Fed’s Cautious Outlook

UMBS opened up 15 bps on the morning. S&P futures down 15 points Bonds were roughly unchanged overnight, but began to improve modestly after the ADP data. Considering the numbers were higher than [...]

Getting Things Done Explained – Part 1

???? My reading notes for getting things done - Part 1. The art of stress free productivity, David Allen and James Fallows. David Allen's getting things done has become one of the most [...]

Mortgage Today 04/29/24: UMBS Edges Up as Markets Eye Fed Meeting and Await Key Economic Data

UMBS up 9 bps on the open. At least it's green. S&P Futures up 12.75 Stocks were buoyed by earnings optimism as traders looked ahead to a busy week for company results. The [...]

Mortgage Today 04/26/24: UMBS Climbs Amidst Slowing PMI and Housing Market Dip

UMBS opened up 27 bps. S&P futures are up 35.75 points After yesterday's somewhat dire implications from quarterly data, today's monthly numbers are surprisingly in line with forecasts. Quarterly numbers were 0.3% higher [...]

Elevate Your Sales Strategy: Unlock Success with Steve Pressfield’s Expert Guidance!

WTMS Blog Today - - Elevate Your Sales Game with Steve Pressfield's Insights ???? Dive into the transformative wisdom of "Turning Pro" and "The War of Art" to unlock the secrets of sales [...]