“Damn, there is so much great knowledge out there. Did you know that “BOOKS” are full of smart?? No, I mean like life changing, I-wish-I-knew-that-years-ago type stuff.

I know that I was waaaayyy late to the game figuring it out. And I know that a lot of you are too busy to read as much as you ‘should’. And that is why you need me.

I still remember how it started for me. It started in June of 2008. After 11 years …..Click to continue

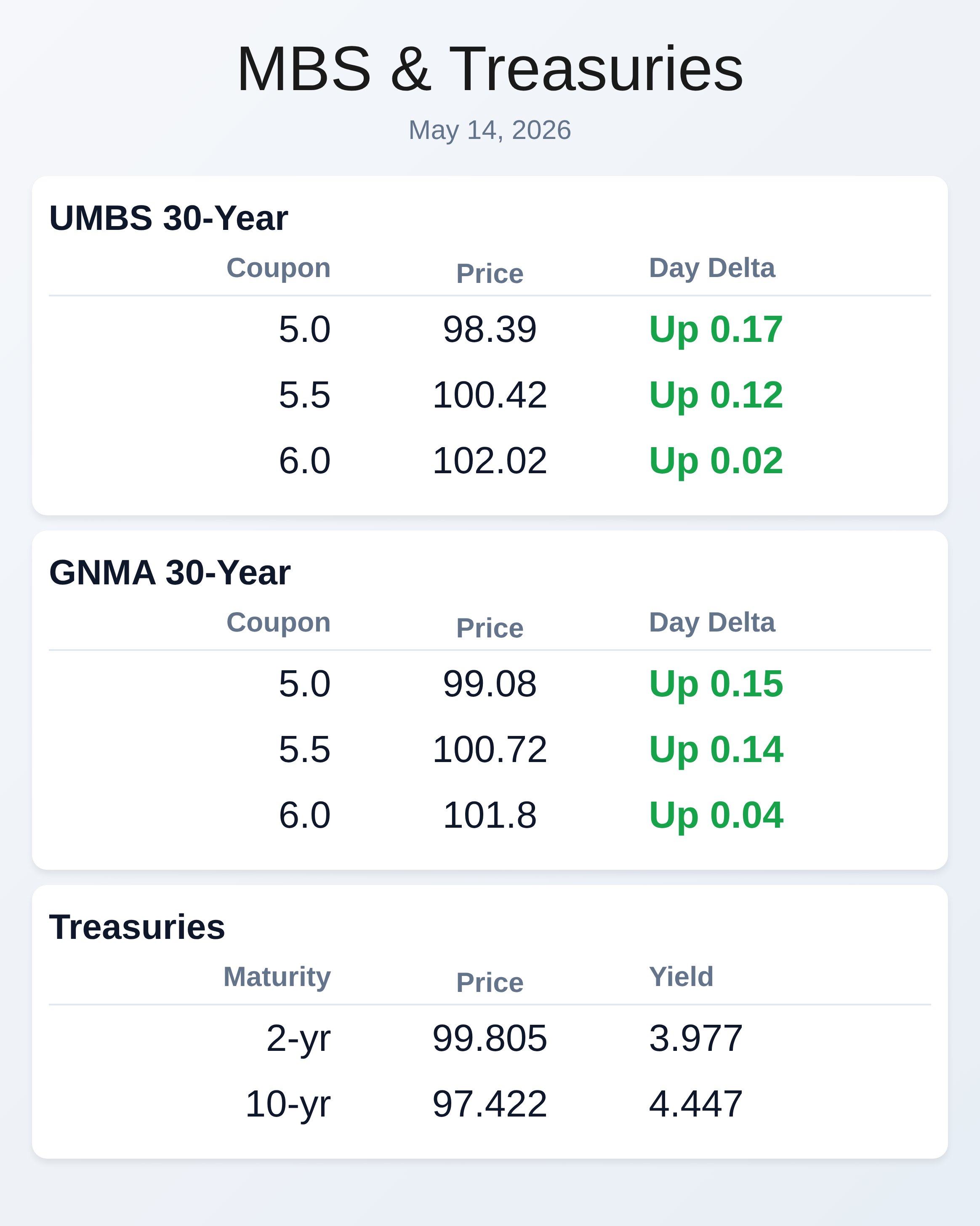

May 14, 2026

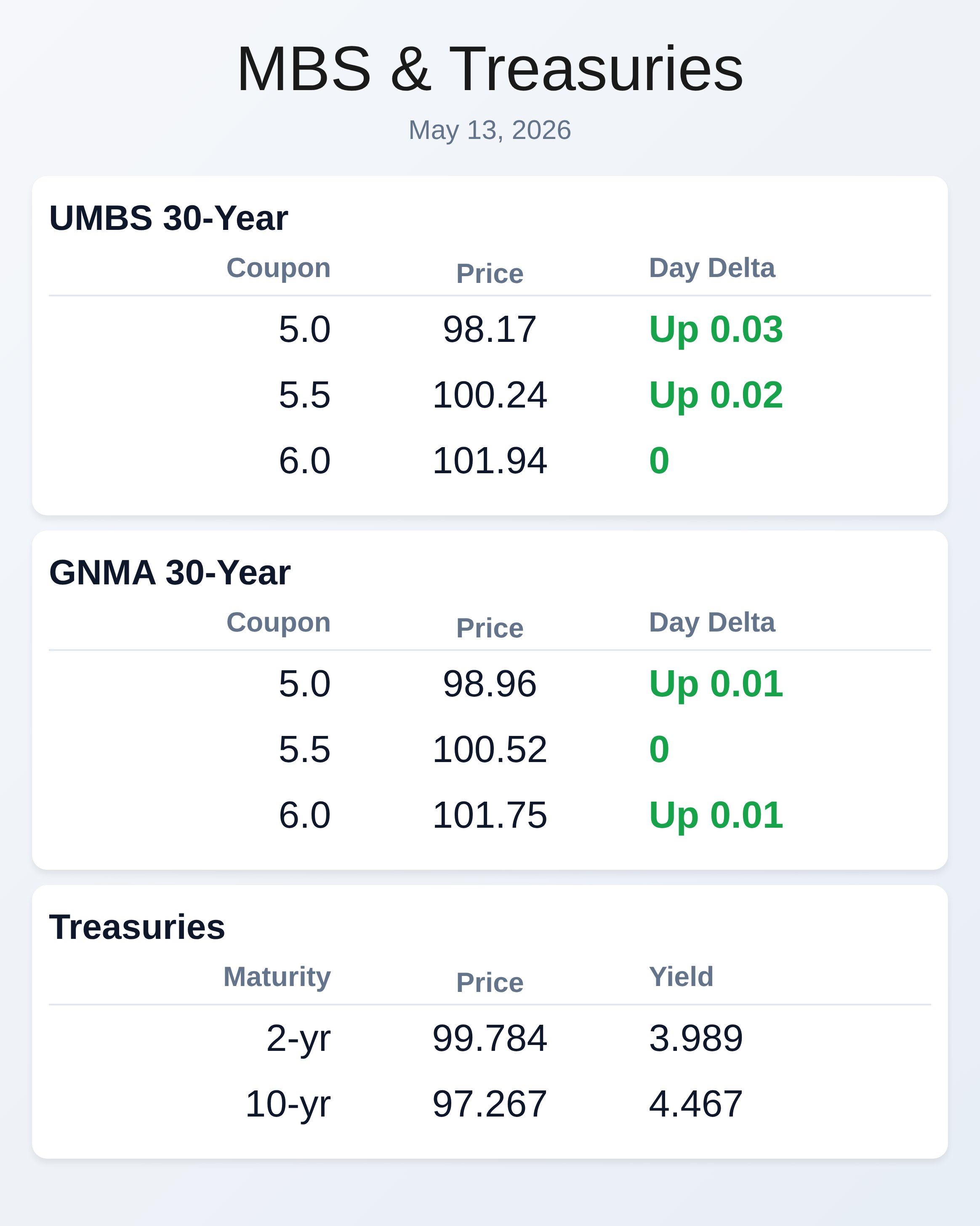

May 13, 2026

May 13, 2026

RECENT ARTICLES

What’s up in Mortgage Today (PM) – 09/30/2025

WTMS Blog Today = What's up in Mortgage Today (PM) - 09/30/2025 The mortgage-backed securities market closed mixed on Monday, with UMBS pricing showing modest weakness amid ongoing concerns about Federal Reserve policy direction. The [...]

What’s up in Mortgage Today (09/30/2025)

WTMS Blog Today = What's up in Mortgage Today (09/30/2025) Mortgage-backed securities (MBS), particularly the Uniform Mortgage-Backed Securities (UMBS) market, saw mixed activity today. UMBS prices showed a slight decline, reflecting a cautious investor sentiment [...]

What’s up in Mortgage Today (PM) – 09/29/2025

WTMS Blog Today = What's up in Mortgage Today (PM) - 09/29/2025 The mortgage-backed securities market experienced mixed trading conditions today as investors continue to navigate uncertainty around Federal Reserve policy direction and economic data. [...]

Article Archive

Mortgage Today 9/27: Market Volatility Amid Uncertain Economic Data and Shutdown Concerns

MBS are down 17 bps on the open - again. S&P futures up 15.25 Much like yesterday, bonds were stronger in the overnight session as European investors have been willing to "buy the [...]

Mortgage Today 9/26: Rate Concerns Impact Housing Market – Key Data Revealed

In today's mortgage update on September 26th, Mortgage-Backed Securities (MBS) opened down 5 basis points. Treasury and European government bond yields dipped after reaching decade highs, while the Bloomberg dollar index remained stable. [...]

Mortgage Today 9/25: Markets React to Central Banks and Inflation Worries

Ouch! UMBS are down a big 39 bps in the morning. S&P Futured down 10.5 points as traders returned to their desks following the worst weekly selloff on Wall Street since March. Most [...]

Mortgage Today 9/22: UMBS 6’s Rise, Treasuries Rally, and Eyes Set on October for Bond Market Battl

UMBS 6's are up 25 bps on the morning so far. S&P Futures up 14.75 It's been a fairly calm and decent trading morning, between the overnight and early domestic hours. Treasuries rallied [...]

Mortgage Today 9/21: Market Reacts to Fed’s Stance, UMBS Drops, and Re/Max Settles Lawsuits

Financial markets faced turbulence following the Federal Reserve's recent announcements. UMBS dropped significantly, with the 5.5% down by 33 bps and the 6.0% down by 40 bps. S&P futures also declined by 40.25 [...]

Mortgage Today 9/20: Fed Holds Steady, UMBS Up but MBS Down Amid Rising Home Sale Failures

Solid start to Fed Day, with UMBS up 13 bps. S&P Futures up 16.5 points 2am ET brought inflation data for Germany and the UK. Both were cooler than expected. Due to base [...]

Mortgage Today 9/19: MBS Down Amid Pre-Fed Jitters and Inflation Concerns

MBS are down another 17 bps on the open. S&P futures down 4.25 In addition to the housing starts data, Canadian inflation came in a bit hotter than expected at the headline level [...]

What’s up in Mortgage Today – 9.18.23 = MBS Starts Flat as Market Eyes FOMC Meeting and GDP Forecasts

MBS starting the week pretty much flat. Bonds began the overnight session in moderately weaker territory, although it looked significantly weaker at times due to a market holiday in Japan. The problem was [...]