**WTMS Blog Today = What’s up in Mortgage Today (AM) – 05/26/2026**

Peace optimism is driving bonds sharply higher this morning as geopolitical tensions ease and market focus shifts toward infrastructure investments over military spending. Overnight, MBS prices surged half a point while the 10-year Treasury plunged eight basis points to 4.482 percent, signaling investor confidence that a potential Middle East resolution could unlock meaningful bond rally potential. However, this optimism comes with a critical caveat: the same market will punish bonds aggressively if diplomatic progress falters, so lenders should view today’s rally as opportunity rather than certainty.

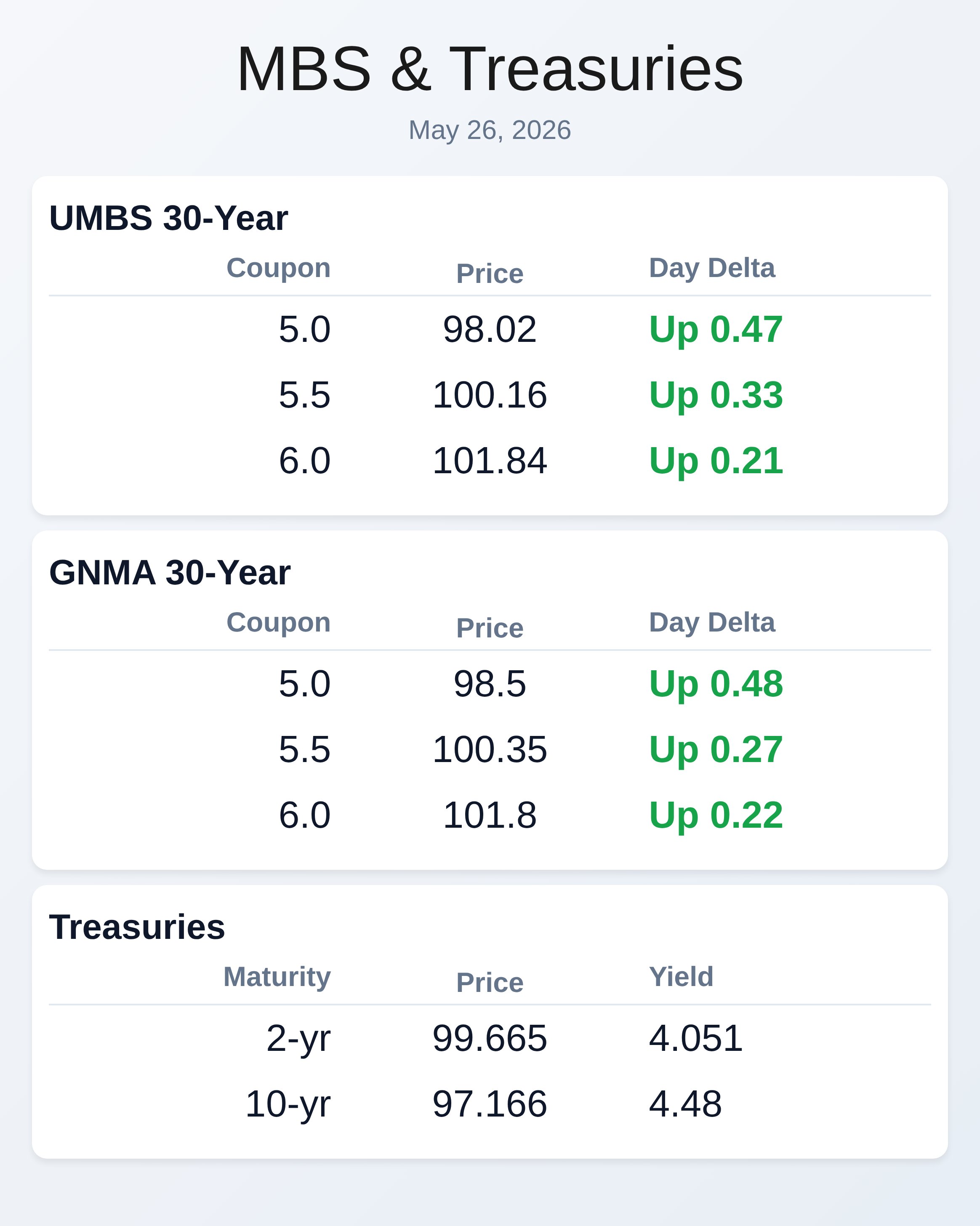

UMBS 5.0 coupons rallied 47 basis points intraday while GNMA 5.0 gained 48 basis points, demonstrating the market’s willingness to reprice quickly on peace headlines. The takeaway is clear—lock when rates favor you, but remain alert to geopolitical flip-flops that could reverse these gains just as fast. Economic data this morning painted a mixed picture that kept the peace narrative intact but offered no clear resolution to inflation concerns.

The Philly Fed Non-Manufacturing Index crashed to -23.6 versus a -13.0 forecast, signaling broader weakness in services-oriented businesses, yet the Chicago Fed Activity Index posted a modest positive 0.14 reading when expectations called for -0.03. This divergence suggests pockets of economic resilience even as regional weakness persists, which means the Federal Reserve’s hawkish tone on inflation risk remains justified. The Fed’s April meeting minutes reinforced that rate hike risk is still on the table if energy-driven inflation spills into housing and wages, a scenario markets are now pricing as possible before year-end.

Treasury auctions for short-term bills and 2-year notes are scheduled for today, along with critical housing data including new home sales, the Case-Shiller index, and Consumer Confidence readings. Builder sentiment rebounded in May back to pre-war levels while pending home sales posted their strongest April reading since 2023, evidence that affordability-bruised buyers are gradually adapting to elevated mortgage rates. Builders continue relying on aggressive incentives—rate buydowns and direct price cuts—to move 481,000 units sitting in inventory, yet mortgage remains central to the product strategy, not a back-end function.

This fundamental shift means mortgage originators who integrate financing solutions into builder incentive packages are better positioned to win JV deals and protect margins. However, with mortgage rates entrenched in the mid-6 percent range, new home sales are expected to decline in April as affordability barriers worsen. Input costs and financing charges are rising alongside demand pressure, squeezing builder margins even as sales incentives expand.

White House adviser Kevin Hassett believes falling oil prices after a Middle East deal could eventually support rate cuts, though most strategists expect long-term borrowing costs to stay elevated even if geopolitical tensions cool. Chair Kevin Warsh of the Federal Reserve took office this week after the FOMC unanimously selected him, and investors expect him to prioritize inflation control over political pressure for easing. The consensus view among bond strategists is that rates may remain “higher for longer” regardless of economic growth moderating, a reality that should inform lender rate lock advice and pricing strategy.

Oil prices remain tightly coupled to Treasury yields, meaning any deterioration in Middle East negotiations could immediately reverse today’s bond gains. This dynamic underscores why borrowers should act decisively on favorable rate windows rather than betting on further refinance opportunities down the road. Consumer spending momentum is slowing as real wage growth remains nearly flat despite nominal income gains, because rising prices are consuming wage improvements entirely.

Forecasts suggest that nominal spending will be almost entirely offset by inflation, meaning consumers are treading water rather than expanding purchasing power. This dynamic will likely force households to pull back on discretionary spending in coming months, a pressure that could cascade into mortgage demand through delayed home purchases and refinance demand. The disconnect between headline income growth and real purchasing power is reshaping generational wealth expectations—with the minority of Americans now believing their children will ever afford homeownership.

Lenders focused on borrower retention and recapture should recognize that rate locks and product innovations addressing affordability (like rate buydowns and ARMs) will remain critical retention tools through the cycle. Industry leaders are converging on artificial intelligence as transformational for mortgage origination, but true competitive advantage comes from blending AI efficiency with the empathy, wisdom, and experience that originate relationships generate. The Coastal Connect Mortgage Expo (May 28), MISMO Summit (June 1–4), and MBA’s Chairman’s Conference (June 7–10) will showcase technology innovations and operator best practices, while specialized webinars on AI governance, borrower recapture, and climate risk integration dominate the calendar.

Developer platforms like Dark Matter’s Empower now allow lenders to auto-generate integration code using ChatGPT or Cursor from OpenAPI specification files, compressing multi-month engineering projects into minutes. This democratization of tech capability means smaller originators can now compete with scale players on platform flexibility and feature deployment. The real differentiator will be teams that use these tools to strengthen borrower relationships and pipeline velocity, not simply replace headcount.

**Locking vs Floating**

Bonds remain transfixed by war-related headlines and are surprisingly receptive regardless of news quality. The clear opportunity exists to rally meaningfully when peace becomes official, but the downside risk is equally sharp if the peace process falters, so borrowers should lock when favorable windows appear rather than speculate on further gains.

**Today’s Events**

Philly Fed Non Manufacturing Index: -23.6 vs.

-13.0 forecast

Chicago Fed Activity Index: 0.14 vs. -0.03 forecast

S&P/Case-Shiller Home Price Index

FHFA House Price Index

Consumer Confidence

Dallas Fed Manufacturing Index

Treasury auctions (short-term bills and 2-year notes)

April new home sales data

**Bond Pricing**

**UMBS 30 yr**

| Coupon | Price | Intra-Day Change |

| 5.0 | 98.02 | 0.47 |

| 5.5 | 100.16 | 0.33 |

| 6.0 | 101.84 | 0.21 |

**GNMA 30 yr**

| Coupon | Price | Intra-Day Change |

| 5.0 | 98.5 | 0.48 |

| 5.5 | 100.35 | 0.27 |

| 6.0 | 101.8 | 0.22 |

**Treasuries**

| Term | Yield | Price | Intra-Day Yield Change |

| 2 yr | 4.051 | 99.665 | -0.071 |

| 3 yr | 4.095 | 98.337 | -0.077 |

| 5 yr | 4.176 | 98.655 | -0.082 |

| 7 yr | 4.316 | 99.608 | -0.086 |

| 10 yr | 4.48 | 97.166 | -0.08 |

| 30 yr | 5.005 | 96.063 | -0.061 |