**WTMS Blog Today = What’s up in Mortgage Today (AM) – 05/27/2026**

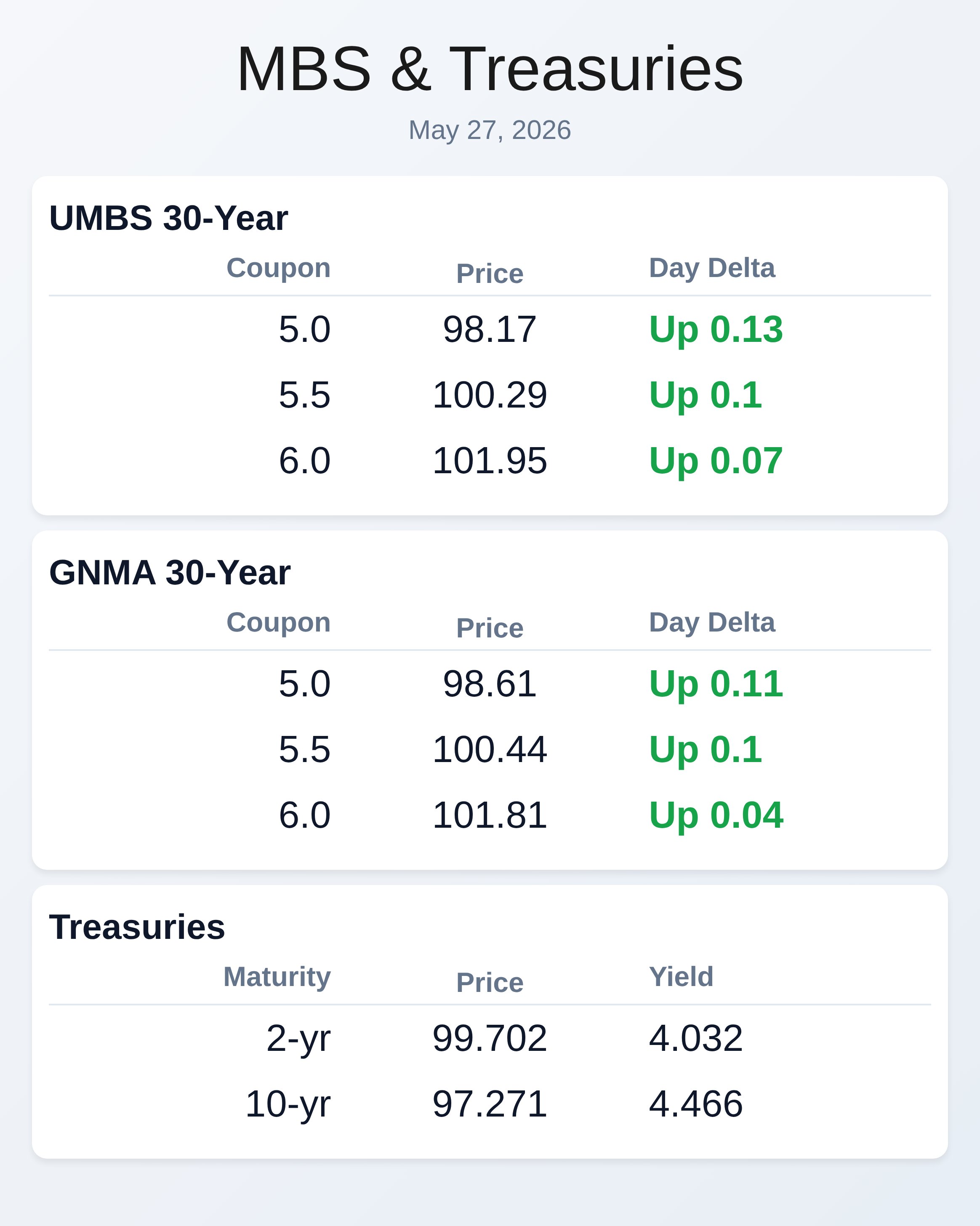

Bonds are rallying sharply on fresh peace deal headlines from Iran, with the 10-year Treasury yield dropping 2 basis points to 4.46 percent as markets price in lower energy costs and reduced geopolitical risk. UMBS 5.0 securities are up 16 basis points to 98.20, while GNMA 5.0 gained 13 basis points to 98.63 as investors fled risk assets. The market’s reaction remains measured despite optimistic news about reopening the Strait of Hormuz, suggesting traders are cautious about the sustainability of any peace framework.

Oil prices have collapsed nearly 6 percent on the speculation, which could help ease inflation concerns that have weighed on Federal Reserve policy expectations. Mortgage originators should note that while intraday volatility is modest, geopolitical headlines are now the primary driver of bond prices—not economic data. Refinance demand collapsed this week as rates hit their highest level since August 2025, with applications falling 18 percent as borrowers abandoned hope for better pricing.

The average 30-year fixed rate climbed to 6.65 percent, making rate-and-term refinances uneconomical for most borrowers, though purchase applications held relatively steady and declined just 0.4 percent. Average purchase loan sizes hit a survey high of $473,600, indicating that smaller-balance borrowers are being priced out of the market entirely. Purchase activity remains resilient in absolute terms but the lack of refi volume is a serious headwind for lender revenue this quarter.

Originators should expect refi volume to remain subdued unless rates fall materially below current levels. Luxury home sales are booming across the country as artificial intelligence-driven wealth creation funnels into high-end real estate. San Francisco luxury home pending sales surged 48 percent year-over-year with median prices reaching $6.7 million, driven by stock compensation, rising tech valuations, and generous sign-on bonuses flooding into the market.

The median U.S. luxury home sale price rose 3.6 percent to $1.39 million over the past three months—more than double the 1.4 percent appreciation in non-luxury homes. Real estate professionals are calling this wealth phenomenon “AI money,” reflecting the structural shift in compensation toward technology workers.

For mortgage originators, this represents a distinct opportunity in the jumbo and high-balance lending space where margins remain stronger than in the mass market. The Federal Housing Finance Agency has settled an industry debate by confirming that tri-merge credit reports will remain mandatory as it transitions to VantageScore 4.0 and FICO 10T scoring models. The decision prioritizes “prudent risk management” and prevents borrowers and lenders from gaming the system through selective reporting to individual credit bureaus.

While the Mortgage Bankers Association had pushed for single-file reports in limited cases to reduce costs, the CHLA and Consumer Data Industry Association backed the FHA’s position on risk management grounds. This provides regulatory clarity for lenders and reduces uncertainty around compliance requirements during the scoring transition. Originators should ensure their systems and processes support tri-merge verification through the transition period.

Consumer confidence dipped for the first time in three months as inflation pressures and geopolitical tensions weigh on household sentiment. The Conference Board’s consumer confidence index fell 0.7 points to 93.1 in May, marking the lowest level since mid-2025 and reflecting persistent anxiety about rising prices and economic stability. While this decline is modest, it signals that gains in consumer mood from earlier spring months may not be sustainable if energy costs surge or Middle East tensions escalate.

Mortgage origination activity is historically sensitive to consumer confidence shifts, and any material deterioration could suppress purchase intent and refinance appetite. Lenders should monitor sentiment indices closely as a leading indicator of pipeline strength in the second half of the year. Treasury auction results from yesterday’s $69 billion two-year note offering came in cleanly, with the issue yielding 4.07 percent and attracting a 2.64x bid-to-cover ratio that reflected solid non-dealer demand at 88 percent.

The front-end of the yield curve continues to underperform longer maturities as Fed policy expectations shift toward a more neutral stance, making 2-year bonds less attractive relative to current policy rates. Today’s economic calendar includes a $70 billion five-year Treasury auction at 1 p.m. EDT, which will test investor appetite for intermediate duration bonds as yields remain elevated.

MBA data released this morning confirmed weakness in mortgage applications overall, with 8.5 percent decline week-over-week driven entirely by refi weakness. The spread between mortgage rates and Treasury yields remains tight, leaving little room for portfolio compression if bond markets sell off.

**Locking vs Floating**

Bonds remain transfixed by geopolitical headlines and are surprisingly responsive to any peace deal optimism, regardless of news quality.

The key takeaway for originators is that meaningful rallies are possible when peace becomes official, but sharp sell-offs could follow if negotiations falter or new military escalation emerges. MBS valuations have improved modestly but volatility will likely remain elevated until Iran peace talks are definitively concluded.

**Today’s Events**

MBA Refi Index (May 22): 920.2

MBA Purchase Index (May 22): 170.4

ADP Employment Change (weekly): 42.25K

5-Year Treasury Note Auction: $70 billion

**Bond Pricing**

**UMBS 30 yr**

| Coupon | Price | Intra-Day Change |

**GNMA 30 yr**

| Coupon | Price | Intra-Day Change |

**Treasuries**

| Term | Yield | Price | Intra-Day Yield Change |

| 2 yr | 4.032 | 99.702 | -0.002 |

| 3 yr | 4.078 | 98.384 | -0.007 |

| 5 yr | 4.161 | 98.723 | -0.015 |

| 7 yr | 4.302 | 99.691 | -0.019 |

| 10 yr | 4.466 | 97.271 | -0.022 |

| 30 yr | 5.003 | 96.093 | -0.008 |