“Damn, there is so much great knowledge out there. Did you know that “BOOKS” are full of smart?? No, I mean like life changing, I-wish-I-knew-that-years-ago type stuff.

I know that I was waaaayyy late to the game figuring it out. And I know that a lot of you are too busy to read as much as you ‘should’. And that is why you need me.

I still remember how it started for me. It started in June of 2008. After 11 years …..Click to continue

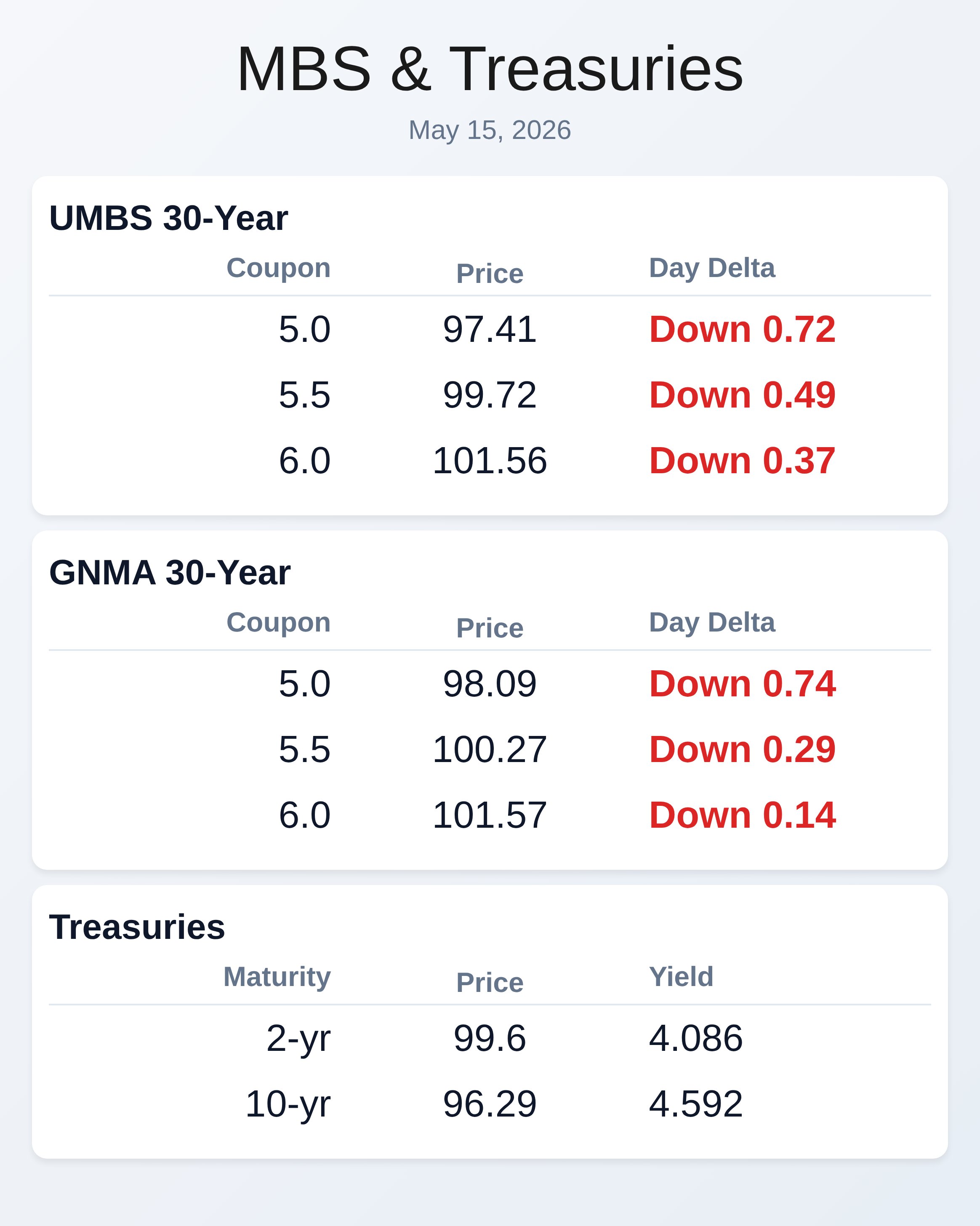

May 15, 2026

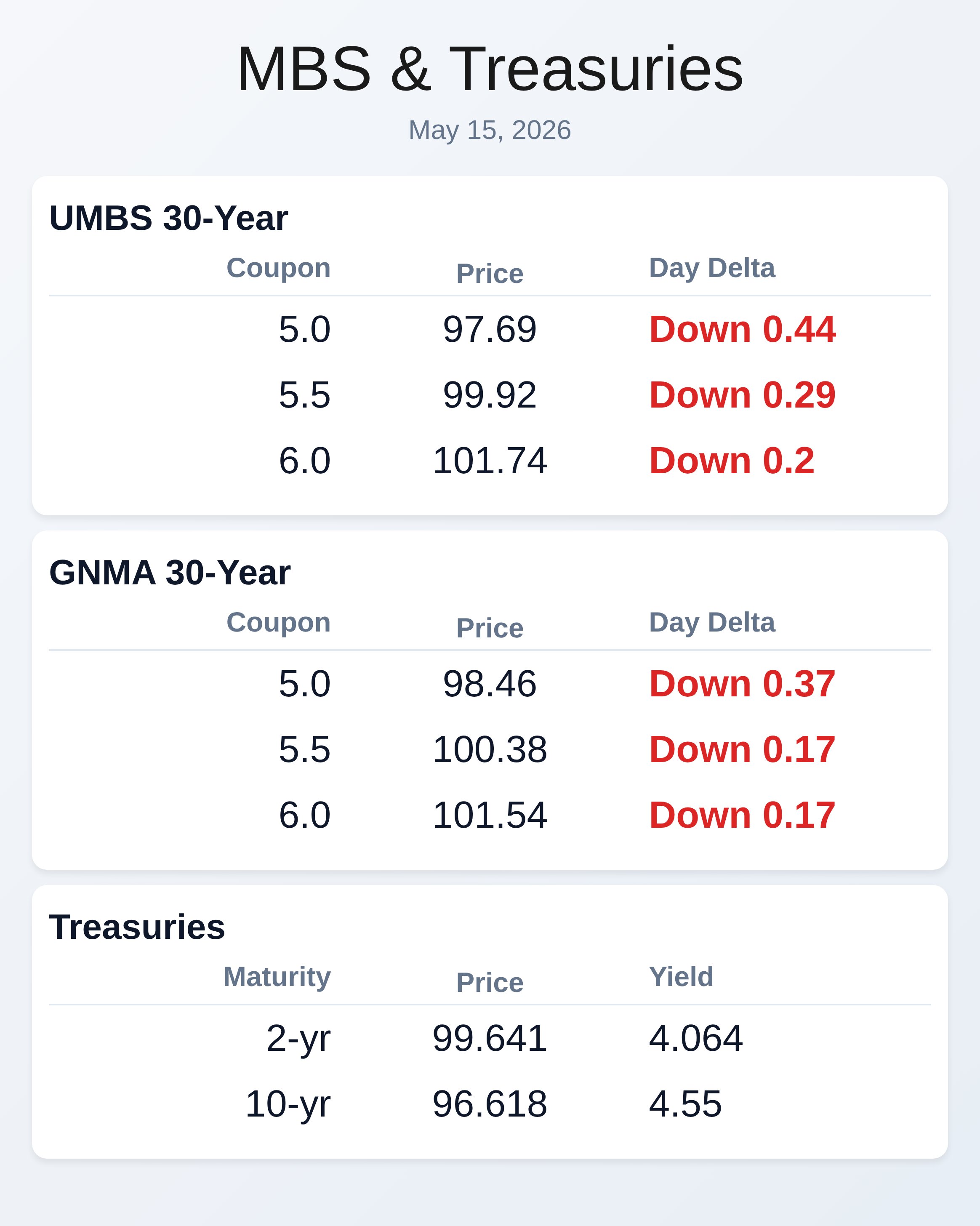

May 15, 2026

May 15, 2026

This $1.3 Billion Mortgage Brawl Just Got Nastier — And It's About to Hit a Breaking Point

If you work in the mortgage industry and you have not been watching the war between UWM and CrossCountry Mortgage over a company called Two Harbors Investment Corp., you have been missing the most dramatic corporate fight the business has seen in years. Open letters. Competing bids. A board calling a rival's offer "predatory." A major shareholder advisory firm flipping the script days before a vote. And a shareholder meeting on Monday that could reshape the industry for a long time.

This is not Wall Street noise. This story touches your pipeline, your pricing, and the economics of the channel you work in every day.

Let's start from the beginning — because this one moves fast.

How It Started

Back in December 2025, United Wholesale Mortgage — the largest wholesale lender in the country — agreed to acquire Two Harbors Investment Corp. in an all-stock deal worth roughly $1.3 billion. Two Harbors is not a household name for most loan officers, but it matters enormously to anyone who cares about mortgage servicing. Two Harbors owns RoundPoint Mortgage Servicing, a platform that sits on top of a $176 billion mortgage servicing rights portfolio. For UWM, which has been aggressively building its in-house servicing capabilities, acquiring RoundPoint would fast-track that strategy in a major way.

The deal looked done. Then March happened.

CrossCountry Mortgage, one of the largest retail lenders in the country and based out of Cleveland, showed up with an unsolicited all-cash offer of $10.80 per share and agreed to cover the $25.4 million termination fee that Two Harbors would owe UWM for walking away. The Two Harbors board looked at cash certainty vs. UWM stock — which had lost 28% of its value in the preceding months — and called CrossCountry's offer superior. They terminated the UWM agreement.

UWM did not go quietly. What followed was one of the most publicly fought corporate battles in recent mortgage industry history.

The Bidding War in Numbers

At one point, a mystery third bidder surfaced with a $10.75 per share offer, only to be quickly passed by CrossCountry raising to $10.80. UWM fired back. CrossCountry raised again to $11.30, which the Two Harbors board accepted. UWM went to $12. CrossCountry matched at $12. UWM raised to $12.50, with shareholders able to choose either $12.50 in cash or 2.3328 shares of UWM stock per Two Harbors share.

The shareholder vote on whether to approve the CrossCountry deal is scheduled for Monday, May 19. That means, as of today, there are four days left on the clock.

The Board's Response Was Not Subtle

When UWM raised to $12.50 this week, the Two Harbors board did not just say no. They dismantled the offer in a sharply worded public statement, calling it "illusory, predatory, and unactionable" — three words you do not typically see in a polished corporate press release. The board's case is this: UWM's $12.50 headline price sounds good, but the default consideration for any shareholder who does not proactively elect cash is UWM stock, currently worth about $7.58 per share as of Monday's close. The board estimates that as many as 30% of Two Harbors shareholders could end up defaulting into stock rather than cash — a scenario the board says UWM has deliberately designed into the offer structure to reduce what it actually pays.

The board also raised pointed financial concerns about UWM's ability to close a deal at all. Fitch has downgraded UWM's credit outlook twice in the past six months. UWM's cash position dropped from $503 million at year-end to $424 million by March 31. The company's leverage is at an all-time high of 3.2 times. And UWM's latest $12.50 bid was not accompanied by an increase in its financing commitment from Mizuho Bank, raising questions about whether the full all-cash option is even funded.

UWM shot back within hours, accusing the board of a "complete and illogical distortion" of its duties to shareholders.

The Proxy Advisor That Changed the Narrative

Here is where it gets interesting for the CrossCountry side of the ledger. Institutional Shareholder Services — known as ISS — is one of the most influential proxy advisory firms in the world. Major institutional investors take their recommendations seriously. And just two days before this writing, ISS issued a recommendation telling Two Harbors shareholders to vote against the CrossCountry deal.

ISS concluded that the board had not run a process designed to maximize shareholder value, and noted that UWM's presence had already been the catalyst that pushed CrossCountry to improve its offer twice. Without UWM staying in the fight, shareholders would have been cashing out at $10.80 per share instead of $12.00. ISS said the board's approach did not appear to be "one that will facilitate full price discovery."

The Two Harbors board called the ISS analysis wrong and doubled down on CrossCountry, but institutional investors do not dismiss ISS recommendations lightly. With the vote five days out, this one genuinely matters.

Why Every Loan Officer Should Be Paying Attention

The surface-level story here is about which company wins a bidding war. The deeper story is about why these two companies are fighting this hard in the first place.

Two Harbors and RoundPoint represent a major chunk of mortgage servicing infrastructure. Whoever ends up owning RoundPoint will control how hundreds of thousands of borrowers' loans get managed after closing — including the borrowers you helped get into their homes. That means retention opportunities, refinance pipelines, and ongoing borrower relationships that flow directly from the servicing platform.

More importantly, mortgage servicing rights have become the strategic resource that major lenders are quietly building empires around. In a market where origination volume is constrained by rates, servicing income is what keeps the lights on. The fight over Two Harbors is a fight over that income — and the pricing strategy that comes with it.

How this ends on Monday will matter for a long time after Monday.

In our next post, we are going to go deeper on what this whole saga is revealing about the financial pressure building underneath the mortgage industry — including some genuinely uncomfortable comparisons that respected analysts are now making in public.

If you want to be the loan officer who actually understands why things work the way they do, subscribe to Well That Makes Sense and we will keep the explanations coming. No jargon. No fluff. Just the stuff that actually matters to your business — delivered to your inbox before your competitors figure out it was important.

RECENT ARTICLES

What’s up in Mortgage Today (PM) – 09/04/2025

WTMS Blog Today = What's up in Mortgage Today (PM) - 09/04/2025 Mortgage-backed securities showed mixed performance today as the 10-year Treasury yield declined to 4.16%, dropping 6 basis points from yesterday's session. This movement [...]

What’s up in Mortgage Today (AM) – 09/04/2025

**WTMS Blog Today = What's up in Mortgage Today (AM) - 09/04/2025** The bond market is experiencing mixed signals this morning as the 10-year Treasury yield fell following weak private payrolls data, providing some relief [...]

What’s up in Mortgage Today (PM) – 09/03/2025

WTMS Blog Today = What's up in Mortgage Today (PM) - 09/03/2025 Bond markets showed signs of stabilization this morning as Treasury yields pulled back from recent highs, providing some relief to mortgage-backed securities. The [...]

Article Archive

What’s up in Mortgage Today – 6.15.23

MBS down 17 bps on the open. Stocks gained 19.74 Bonds were already moderately stronger on the day and are extending the gains cautiously so far. Coming in as-expected at the core level [...]

Hormozi: If your life sucks, the easiest thing to do is to change your environment.

Reading Notes for: Change Your Environment To Improve Your Life If your life sucks, the easiest thing to do is to change your environment. It is better to change your environment [...]

What’s up in Mortgage Today – 6.14.23

Stocks & Bonds winning on the open. MBS up 16. Stocks up 12.5 Bonds were flat to slightly stronger in the overnight session with minimal volatility and average volume. Core Producer Prices, m/m [...]

What’s up in Mortgage Today – 6.13.23

MBS down 17 bps on the open. Stocks gained 19.74 Bonds were already moderately stronger on the day and are extending the gains cautiously so far. Coming in as-expected at the core level [...]

Hormozi: If you fail in a Forest and nobody is there to see it – does it matter.

Reading Notes for: If you fail in a Forest and nobody is there to see it - does it matter. The other odd thing is - When you are starting out, [...]

What’s up in Mortgage Today – 6.12.23

MBS down 23 bps and Stocks up 7 Many lenders are not yet out with prices for the day. Those who are could already be considering negative reprices as MBS are currently down [...]

What’s up in Mortgage Today – 6/9/23

MBS down 14 bps on the day. Stocks up 24 points Friday started with a noticeable increase in market activity and interest due to the release of important economic data. The Canadian employment [...]

What’s up in Mortgage Today – 6/8/23

MBS were up 9 bps early. Stocks were flat Bonds were modestly weaker in the overnight session, but have bounced back into positive territory following the much weaker than expected jobless claim numbers. [...]