“Damn, there is so much great knowledge out there. Did you know that “BOOKS” are full of smart?? No, I mean like life changing, I-wish-I-knew-that-years-ago type stuff.

I know that I was waaaayyy late to the game figuring it out. And I know that a lot of you are too busy to read as much as you ‘should’. And that is why you need me.

I still remember how it started for me. It started in June of 2008. After 11 years …..Click to continue

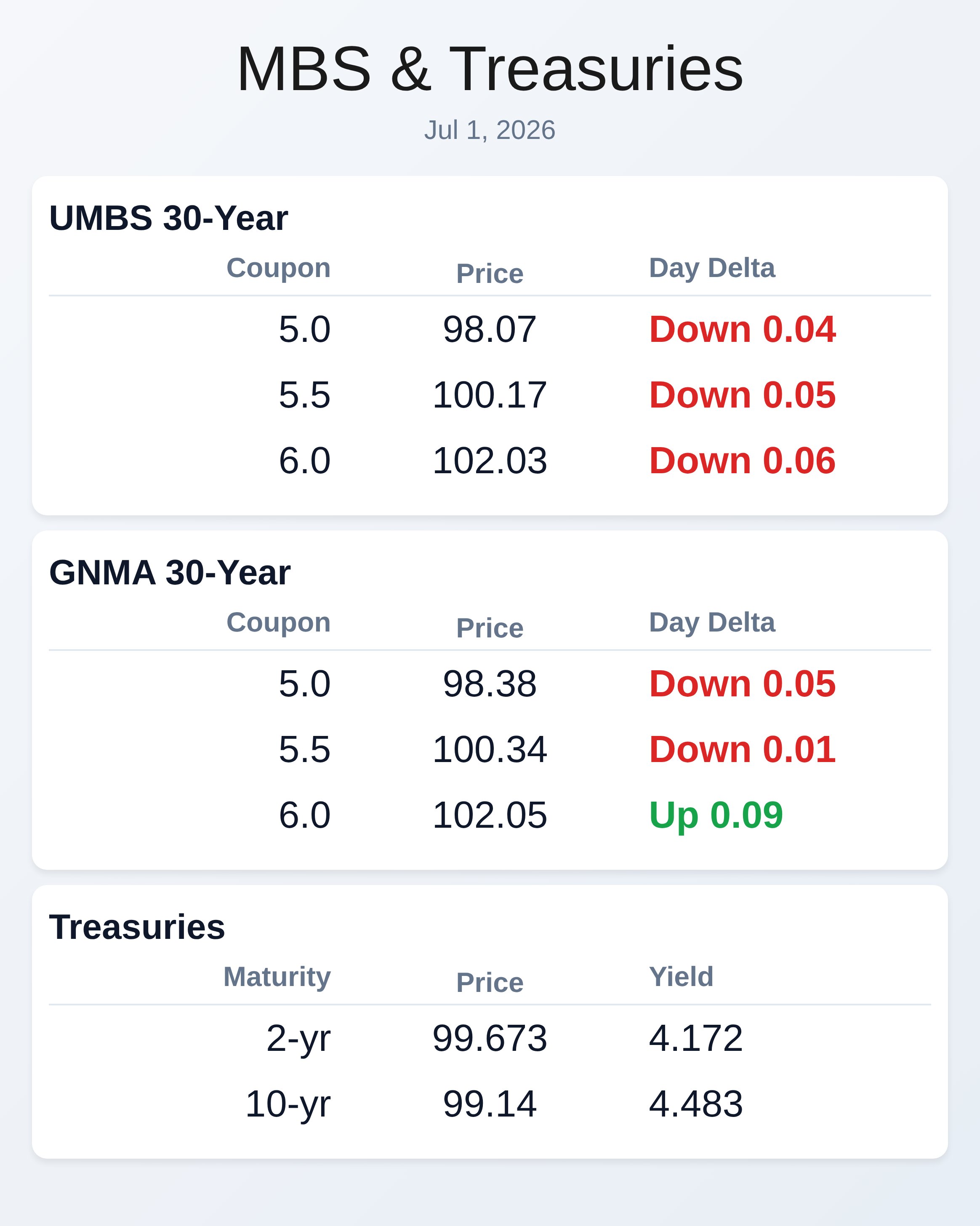

July 1, 2026

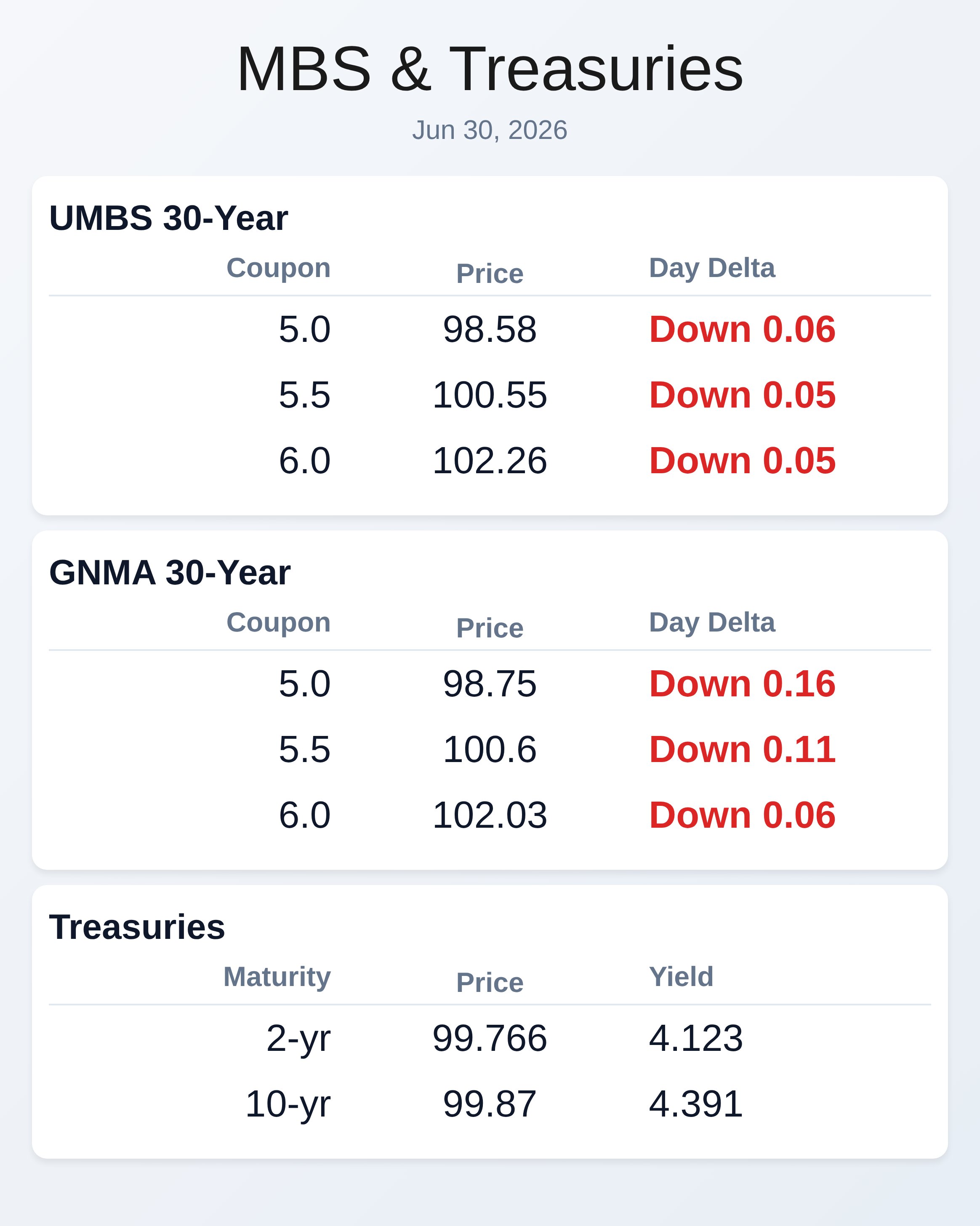

June 30, 2026

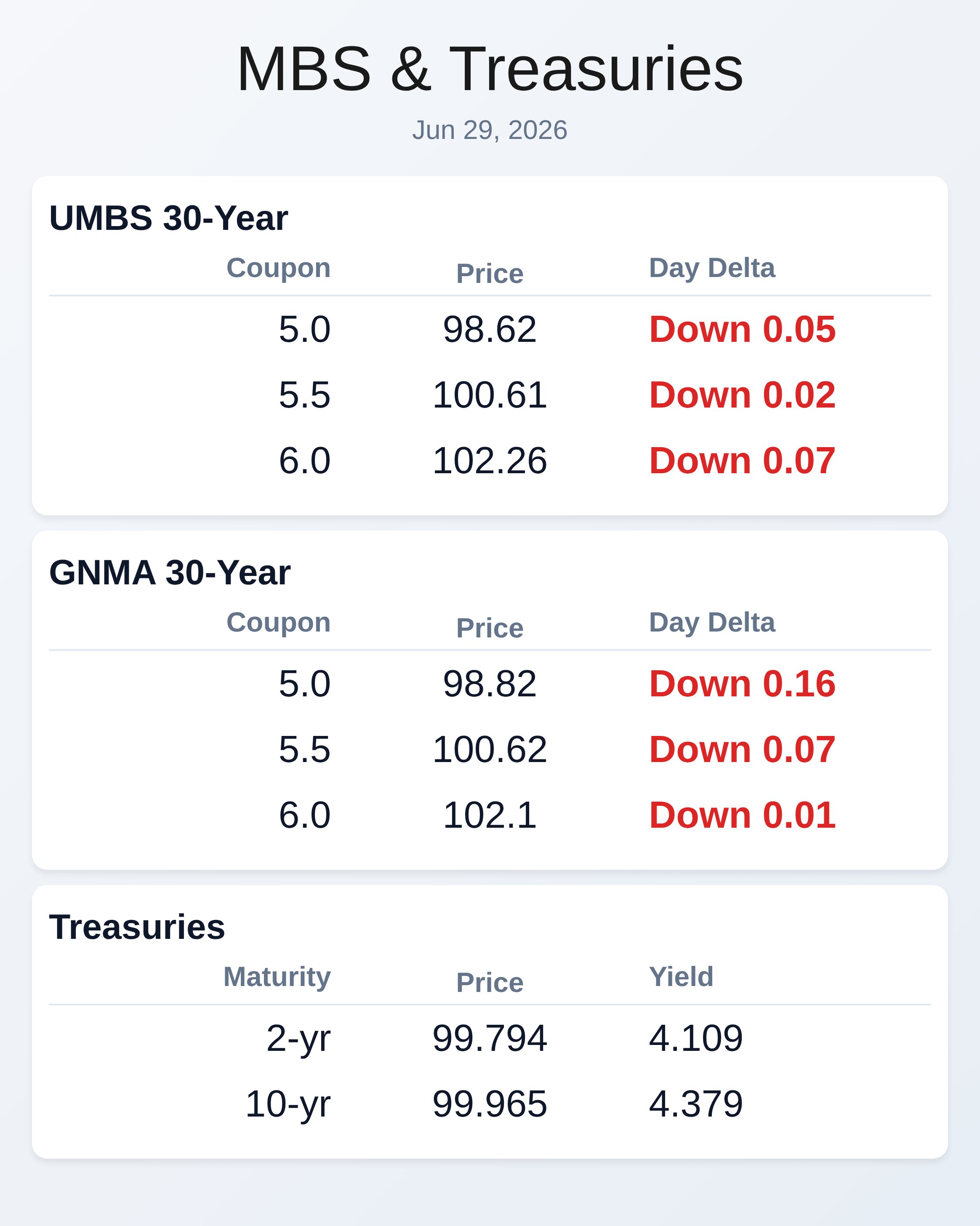

June 29, 2026

RECENT ARTICLES

On “overnight success”, Compliments behind your back, & Sustained outrage makes you stupid.

Reading Notes for: Kevin Kelly's 99 Pieces of Unsolicited Advice from https://kk.org/thetechnium/99-additional-bits-of-unsolicited-advice/ Click here for a Bio on Kevin Kelly another bunch of unsolicited advice. Compliment people behind their [...]

99 Pieces of Unsolicited Advice: Multitude, Maturity, Respect, Training

Reading Notes for: Kevin Kelly's 99 Pieces of Unsolicited Advice from https://kk.org/thetechnium/99-additional-bits-of-unsolicited-advice/ Click here for a Bio on Kevin Kelly another bunch of unsolicited advice. Train employees well enough [...]

99 Pieces of Unsolicited Advice: Pyramid Schemes, Failure, Tyranny

Reading Notes for: Kevin Kelly's 99 Pieces of Unsolicited Advice from https://kk.org/thetechnium/99-additional-bits-of-unsolicited-advice/ Click here for a Bio on Kevin Kelly another bunch of unsolicited advice. If someone is trying [...]

Article Archive