“Damn, there is so much great knowledge out there. Did you know that “BOOKS” are full of smart?? No, I mean like life changing, I-wish-I-knew-that-years-ago type stuff.

I know that I was waaaayyy late to the game figuring it out. And I know that a lot of you are too busy to read as much as you ‘should’. And that is why you need me.

I still remember how it started for me. It started in June of 2008. After 11 years …..Click to continue

July 6, 2026

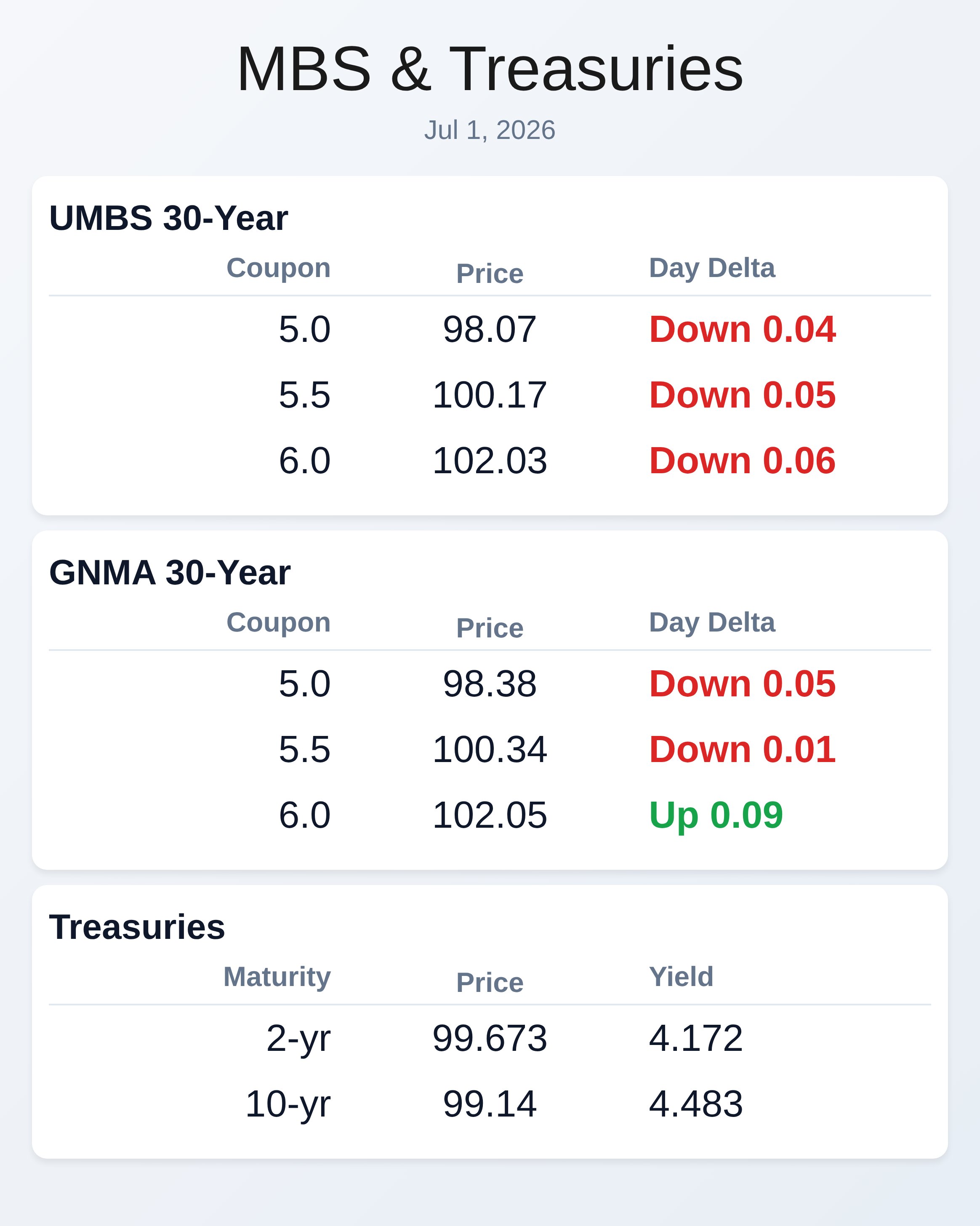

July 1, 2026

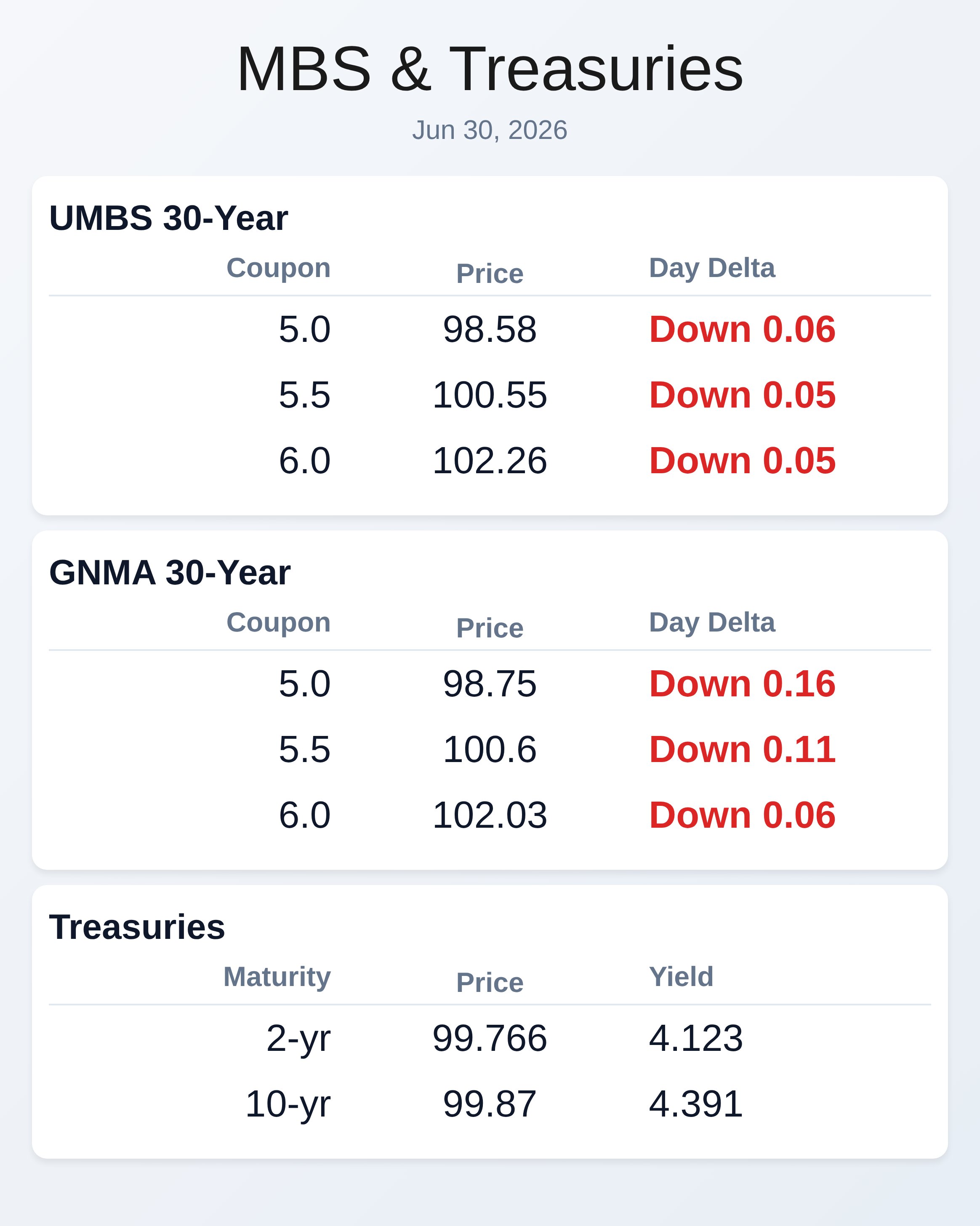

June 30, 2026

RECENT ARTICLES

When making more money, how open minded are you

When it comes to selling a lot more, how open minded are you? I mean, who's really going to say NO to that? Basically just a true hardcore curmudgeon (keeping it PG here) that [...]

I’m not sure if it’s for you but you should read this

To be great at sales you have to know what to say. Like everything, these things you say can be beginner, immediate, and advanced. The coming series on WellThatMakesSense.com are from an excellent book [...]

That’s Amor Fati

You cannot "get over" or "get around" most of your life's problems. He says the best way out is always through. And I agree to that, or in so far. I can see no [...]

Article Archive