“Damn, there is so much great knowledge out there. Did you know that “BOOKS” are full of smart?? No, I mean like life changing, I-wish-I-knew-that-years-ago type stuff.

I know that I was waaaayyy late to the game figuring it out. And I know that a lot of you are too busy to read as much as you ‘should’. And that is why you need me.

I still remember how it started for me. It started in June of 2008. After 11 years …..Click to continue

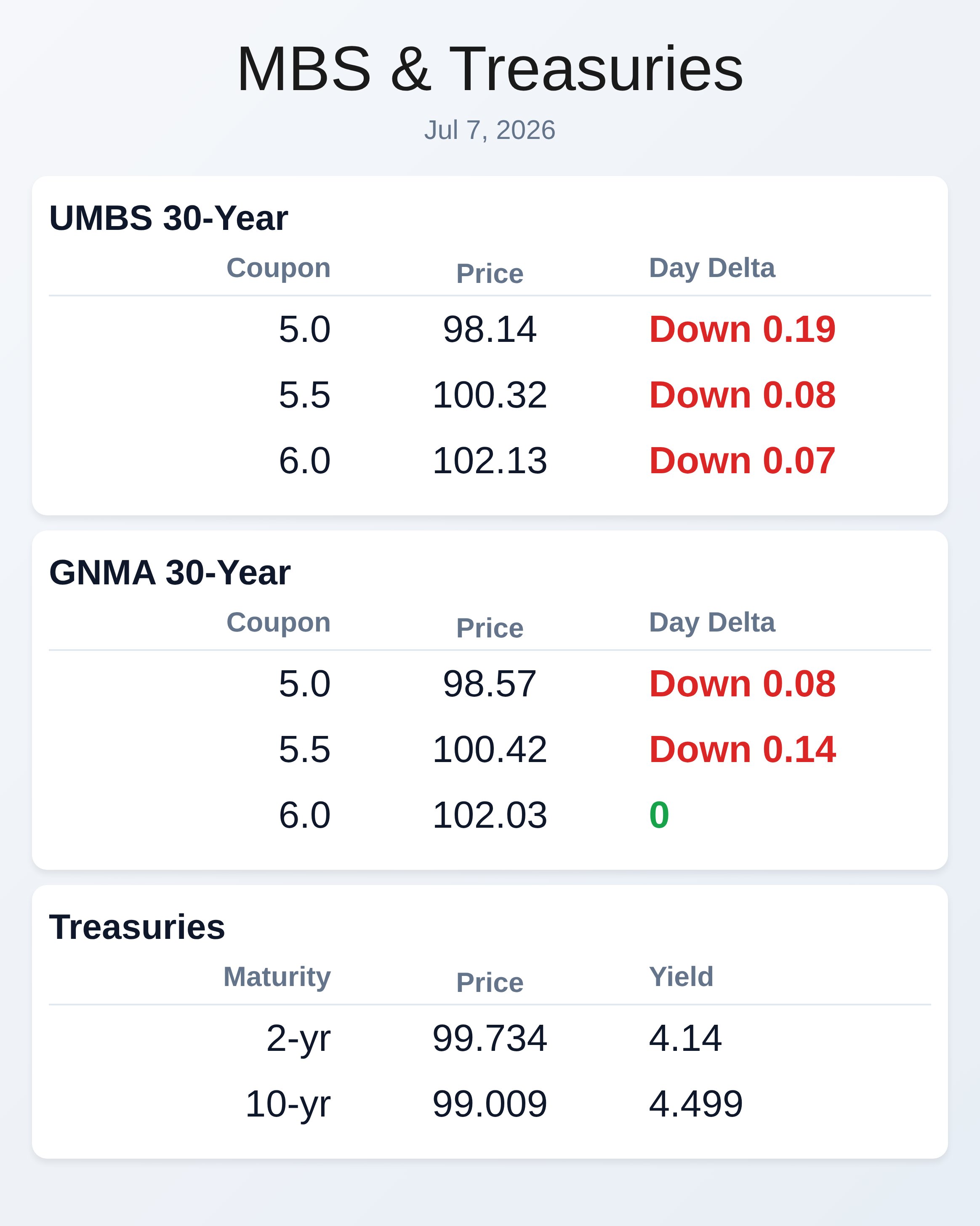

July 7, 2026

July 6, 2026

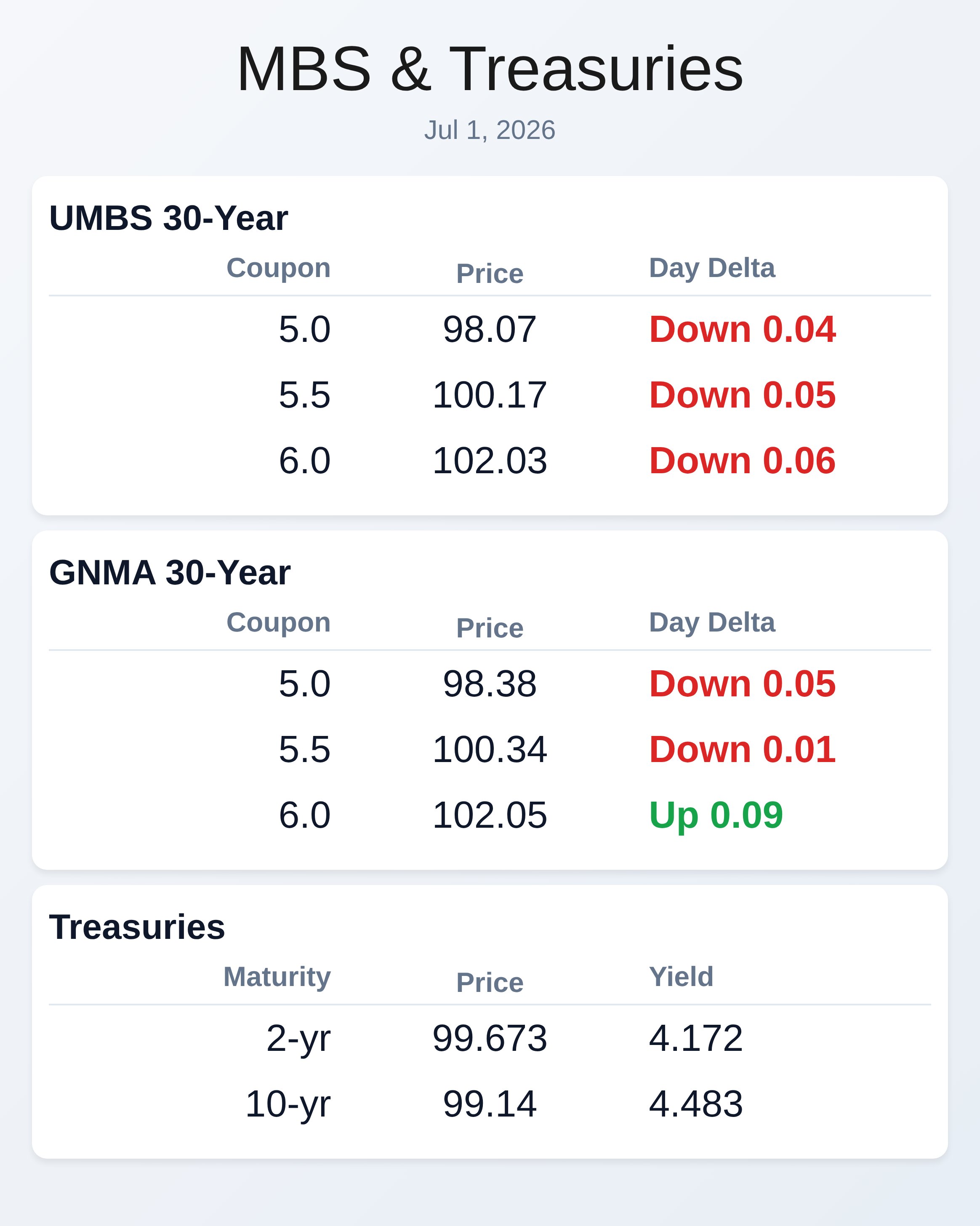

July 1, 2026

RECENT ARTICLES

Give the Gift of Wrong

Upon the recommendation of The Great Tim Ferris, I read a super interesting essay today entitled: Keep your Identity Small. Billionaire investor/philospher Paul Graham great job with this interesting title. Though the copy writing [...]

Most Influential Book on Influence Ever (Tip 14)

This is part of a series of information/stories delivered from the INCREDIBLE book, "Influence: The Psychology of Persuasion" by Robert Cialdini. If you work or live a life where you have to get people [...]

The Economy – Today, Tomorrow, and Down the Road

Combining news items today helps summarize where I think we are going. On Friday, Q1 GDP came in stronger due to net exports and inventories. So basically messing with numbers that don't impact our [...]

Article Archive